IP in EMU Weakens in December; Sector Trends Show Slow or Erratic Improvements

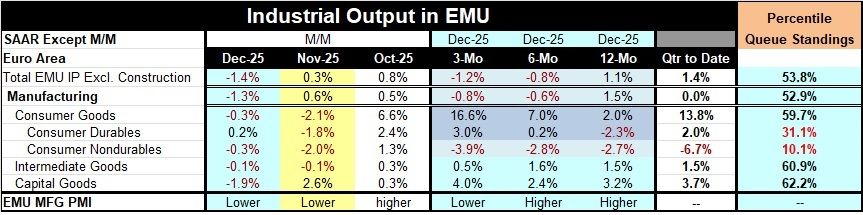

Industrial output in the European monetary union fell by 1.4% in December. Manufacturing output fell by 1.3%. Output of consumer goods fell by 0.3%, output of intermediate goods fell by 0.1%, and output of capital goods fell by 1.9% in December. The subsector, consumer durables, showed an increase in output of 0.2% in December. Headline and manufacturing output in December reversed the increases seen in October and November. However, consumer goods, consumer nondurables, and intermediate goods saw two consecutive months of output declines for November and December.

Turning to sequential trends, overall industrial output rises by 1.1% over 12 months, falls at a 0.8% annual rate over six months, and then falls at a 1.2% annual rate over three months showing a tendency for deceleration. Manufacturing shows the same pattern of eroding growth rates for the one-year and shorter horizons.

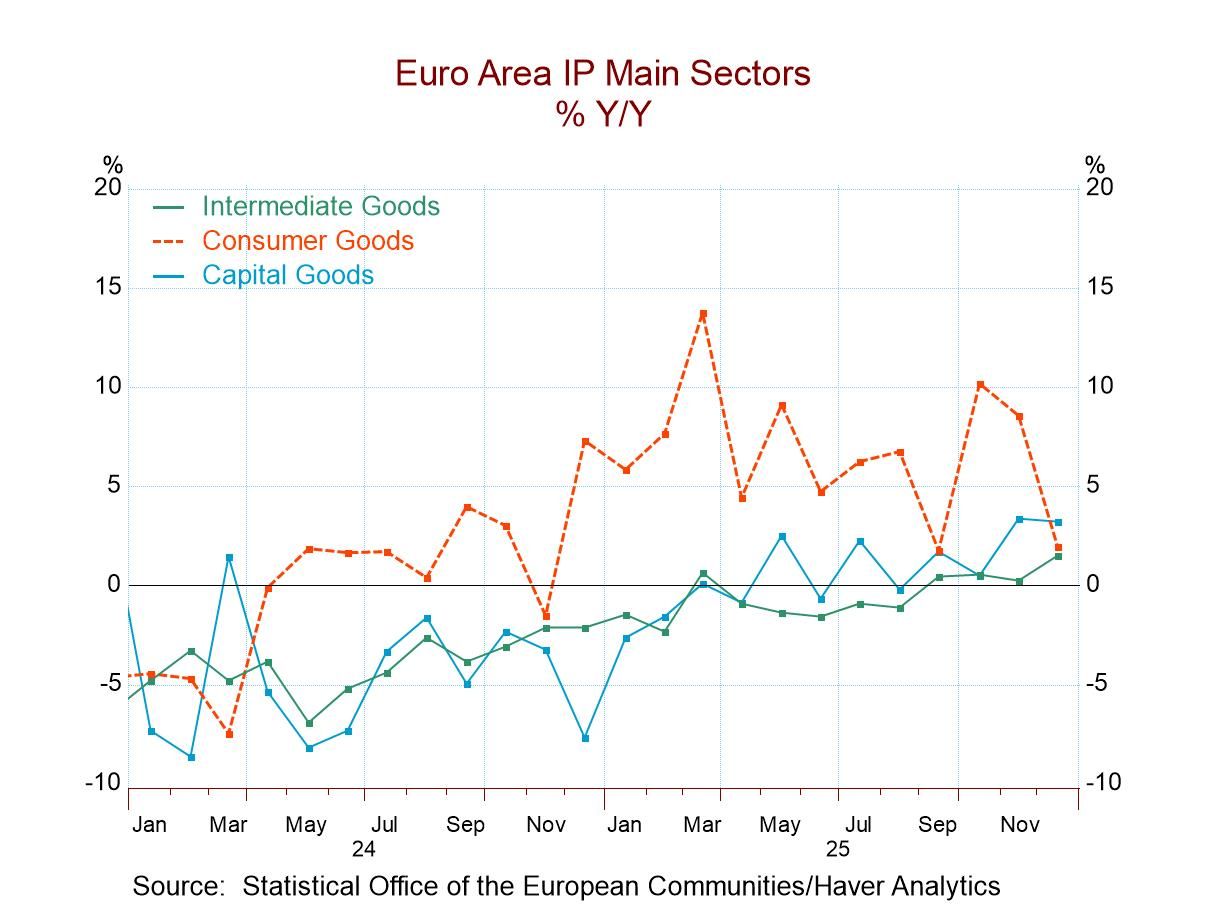

Sector stories However, for consumer goods, manufacturing output is accelerating steadily from a growth rate of 2% over 12 months, to a 7% pace over six months, and to a 16.6% annual rate over three months; the inclusion of ‘semi-durables’ in this category total makes it stronger than the two detailed subcategories of durable and nondurable goods. Consumer durables output transitions from falling 2.3% over 12 months to growing at a 3% pace over three months. Consumer nondurables output shows persistent declines, with slightly more intense over shorter periods, echoing the deceleration phenomenon. Intermediate goods and capital goods do not show clear sequential trends, but both categories show increases in output over all three horizons.

Cross currents These cross currents among sectors make it hard to characterize what's happening with output trends in the European Monetary Union. The country detail shows a good deal of turbulence, with a number of countries showing decelerating output trends and others showing accelerating output trends. It's fair to say that manufacturing in the EMU continues in the grip of cross currents. While the short-term data in the table that look at growth rates from 12-months to 6-months to 3-months show more weakening than strengthening, the trends in the graph across recent 12-month growth rates seem to show a little more solidifying and expanding behavior – albeit with confusing volatility as well.

Quarter-to-date (concluded Q4) In the quarter to date, all of the sectors and subsectors show output rising except for the aggregate for manufacturing that is flat, and consumer nondurables that show a decline at 6.7% at an annual rate. In the quarter to date, overall output is growing at a 1.4% annual rate, while consumer goods output is expanding at a 13.8% annual rate, immediate goods output is expanding at 1.5% annual rate, and capital goods output is expanding at a 3.7% annual rate. Those sector numbers look exceptionally healthy.

Ranking the trends The far-right hand column analyzes the 12-month growth rates comparing them to historic growth rates since 2006. Most of the growth rate rankings over this span are moderate, with standings above their respective 50th percentiles, placing them above their historic medians. However, consumer durable goods and nondurable goods are exceptions, with rankings in their 31st percentile and 10th percentile, respectively. Consumer nondurables output is particularly weak in comparison with historical trends. On the other hand, intermediate goods and capital goods output have rankings in their 60th percentile, and for all consumer goods output, the ranking is near its 60th percentile. Looking only at manufacturing, the ranking slips to its 52.9 percentile; for the headline series which excludes construction, the ranking is at its 53.8 percentile.

Summing up On balance, it's the consumer sector that is holding back the advancements of output, and this is not surprising with such weak conditions in Europe for consumer confidence. However, in another respect, it's somewhat surprising because unemployment rates remain historically low in the European Monetary Union - and for Europe generally - and typically jobs are one of the more important ingredients in consumer confidence. Some of this disconnect could be because of the war on Europe's doorstep, and some of it may also be concern about the current rough spot the NATO is experiencing and that's reflected in the relations between Europe and the United States. Globally, growth is beginning to look a little bit more solid, but industrial production in the EMU continues to be touch-and-go, in part, because its largest economy, Germany, continues to struggle.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global