U.S. Housing Market Index Falls for Second Consecutive Month in February

Summary

- HMI continues to weaken in Feb., indicating most builders remain pessimistic about the current and near-term housing outlook.

- Two of three HMI components fall, w/ the steepest m/m decline in potential buyers' traffic (-8.3%).

- Regional weakness continues, w/ the sharpest m/m drop in the West (-11.8%).

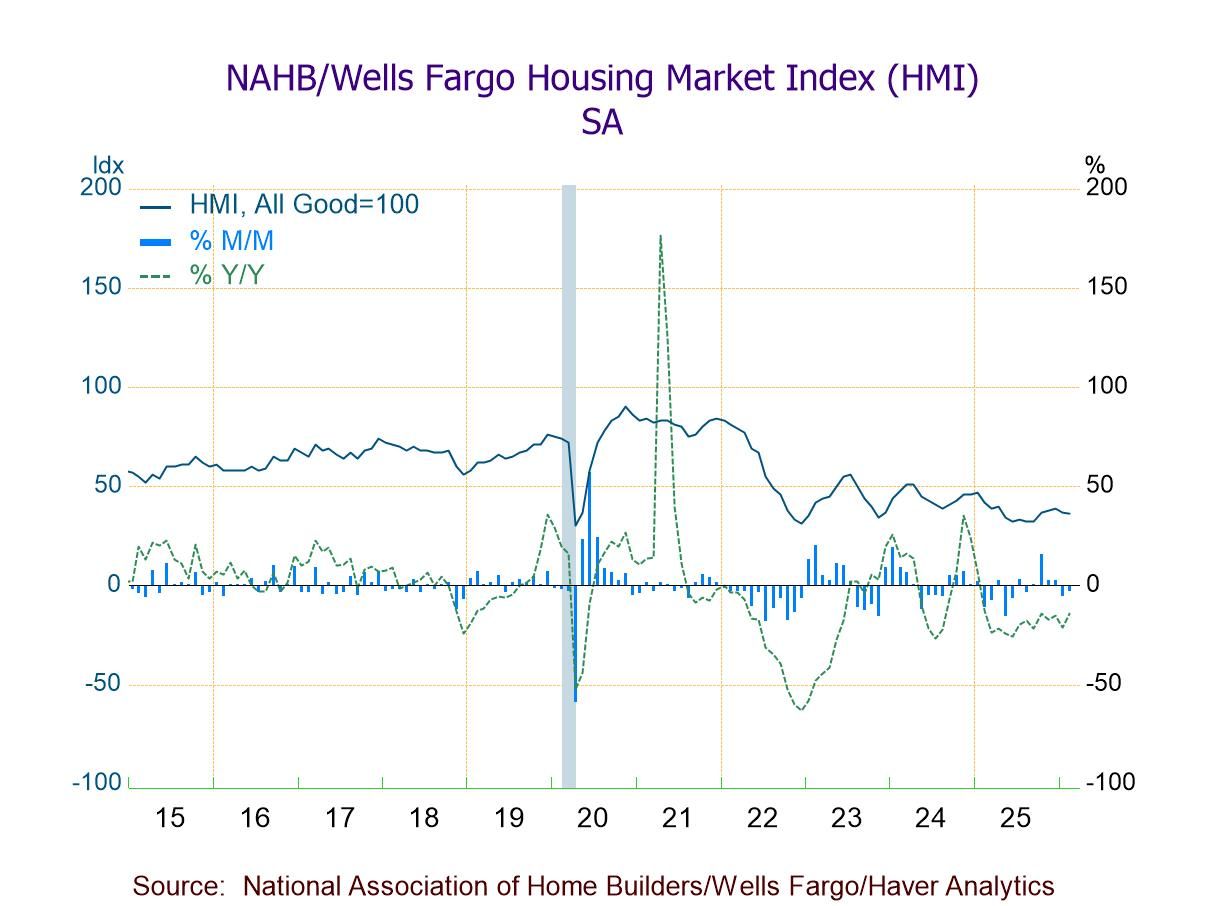

The Housing Market Index (HMI) from the National Association of Home Builders/Wells Fargo fell 2.7% m/m (-14.3% y/y) to a lower-than-expected 36 in February following a 5.1% decline to 37 in January (unrevised) and a 2.6% rise to 39 in December (unrevised). February marked the second successive m/m decline after three straight m/m increases. A reading of 38 had been expected in the INFORMA Global Markets survey. The HMI had been below the breakeven 50 level since May 2024. The February index, lower than 42 in February 2025, was 35.7% below a high of 56 in July 2023 and 60.0% below a record-high 90 in November 2020.

Notably, the average rate on a 30-year fixed rate mortgage fell to 6.09% in the February 12 week, the lowest in three weeks, from 6.11% in the February 5 week, according to Freddie Mac. The rate was below a high of 7.22% in the week of May 2, 2024 and a peak of 7.79% in the week of October 26, 2023.

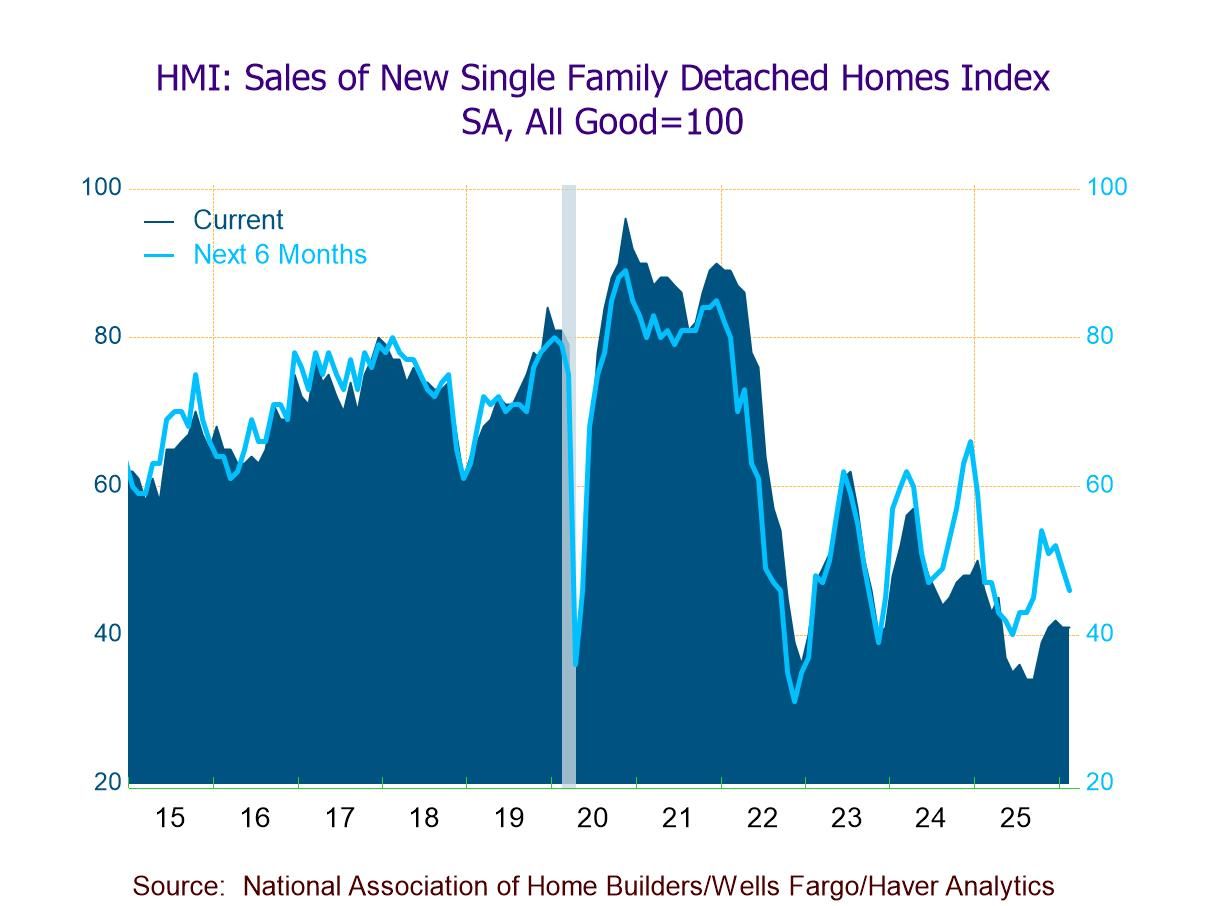

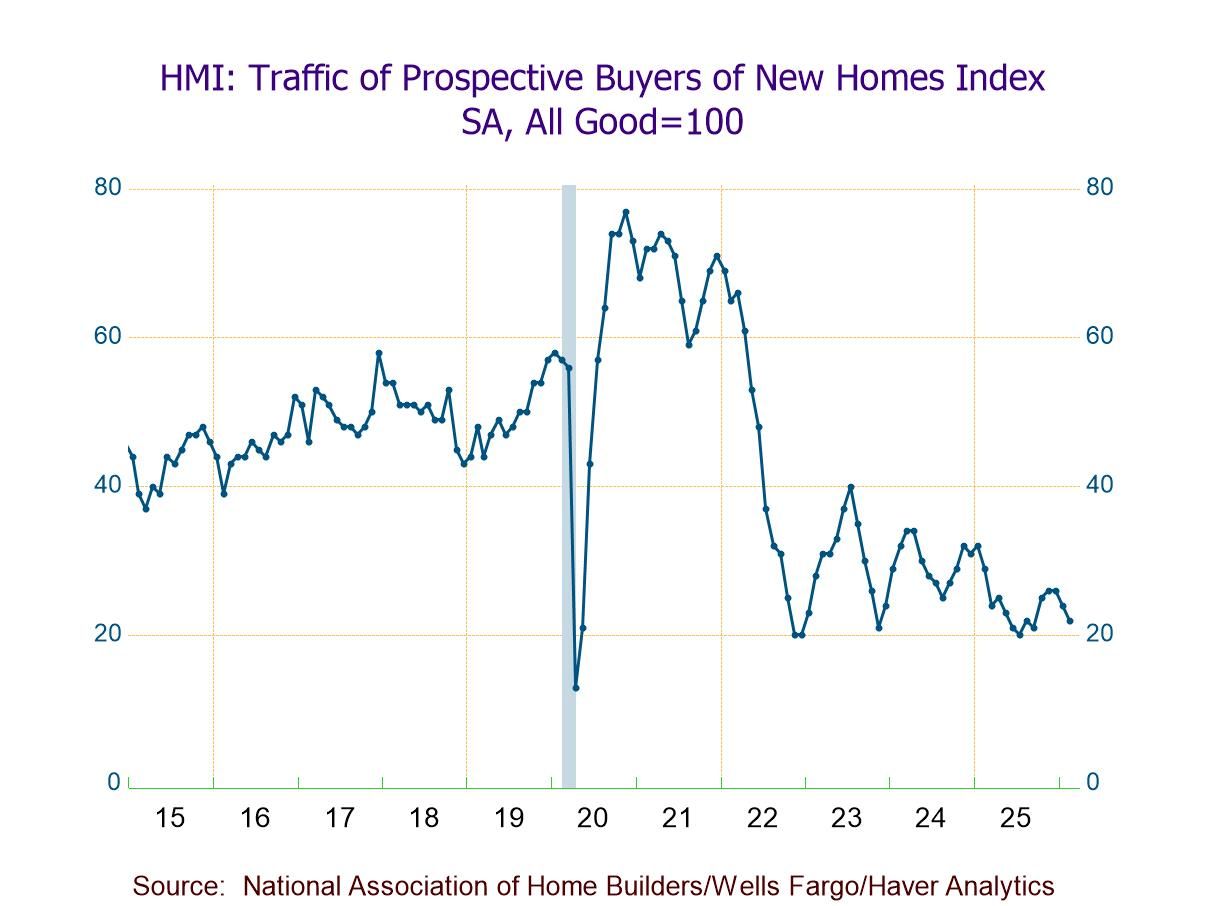

Two of the three HMI components decreased this month. The index of present single-family sales conditions was unchanged m/m at 41 (-10.9% y/y) in February after a 2.4% decline in January. The index was 33.9% below a high of 62 in July 2023 and 57.3% below a record-high 96 in November 2020. The index of expected single-family sales for the next six months fell 6.1% (-2.1% y/y) to 46 in February after a 5.8% decrease to 49 in January, marking the third m/m fall in four months and the lowest level since September 2025. The index was 30.3% below a high of 66 in December 2024 and 48.3% below a peak of 89 in November 2020. The index measuring traffic of prospective buyers slid 8.3% (-24.1% y/y) to a five-month-low 22 in February on top of a 7.7% drop to 24 in January. The index was 45.0% below a high of 40 in July 2023 and 71.4% below a record-high 77 in November 2020.

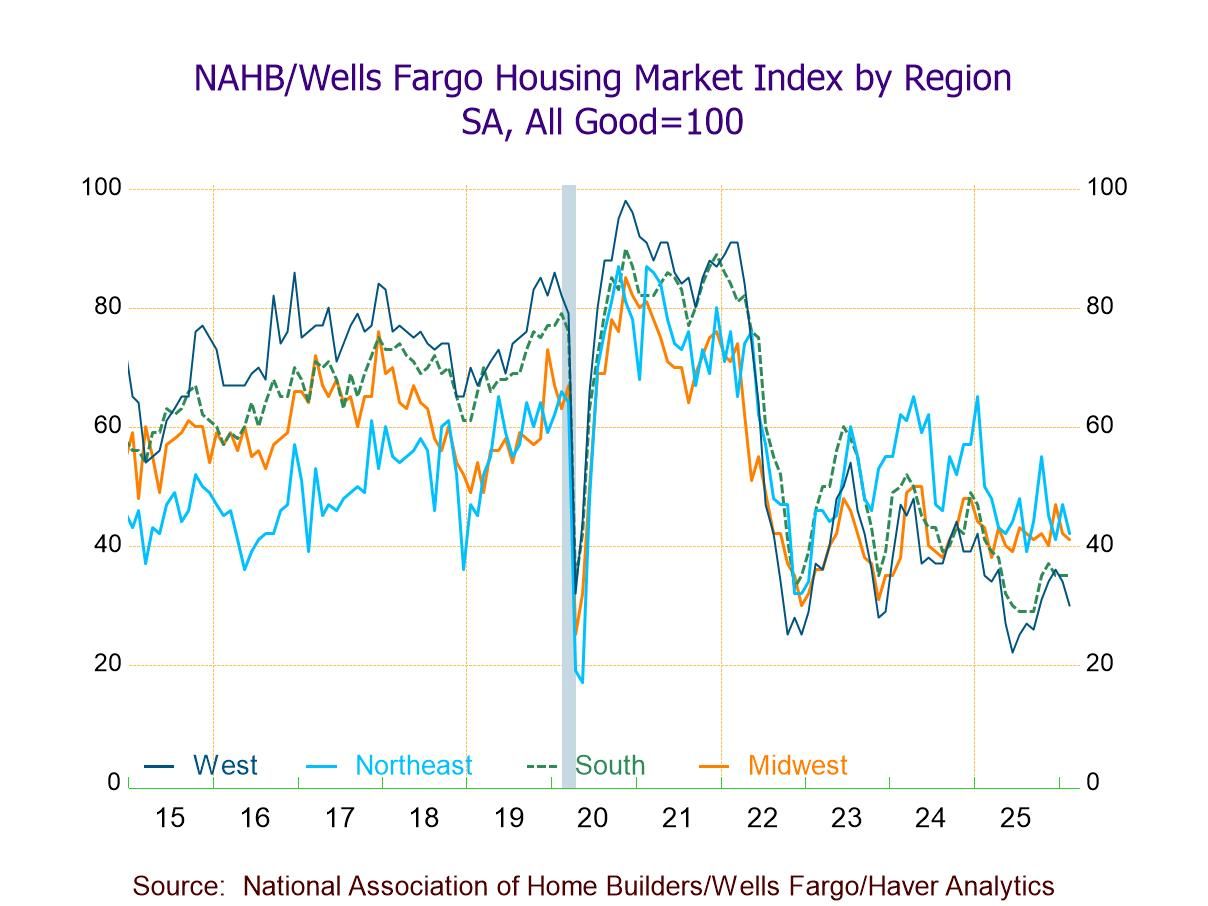

By region, the HMIs mostly fell m/m this month. The index for the West dropped 11.8% (-14.3% y/y) to 30 in February, the lowest level since September 2025, after a 5.6% decline to 34 in January. The index for the Northeast decreased 10.6% (-16.0% y/y) to 42, down for the third time in four months, following a 14.6% January rebound to 47. The index for the Midwest fell 2.4% (-4.7% y/y) to 41 after a 10.6% January fall to 42, registering the third m/m decline in four months and the lowest reading since November. Meanwhile, the index for the South held steady at 35 for three consecutive months (-14.6% y/y).

The NAHB has compiled the Housing Market Index since 1985. It reflects survey questions which ask builders to rate sales and sales expectations as "good," "fair" or "poor" and traffic as "very high," "average" or "very low". The figures are diffusion indexes with values over 50 indicating a predominance of "good"/"very high" readings. In constructing the composite index, the weights assigned to the individual index components are: 0.5920 for single-family detached sales, present time, 0.1358 for single-family detached sales, next six months, and 0.2722 for traffic of prospective buyers. The regional indexes run back to December 2004.

These data are included in Haver's SURVEYS database. The Informa Global Markets survey is in Haver's MMSAMER database.

Winnie Tapasanun

AuthorMore in Author Profile »Winnie Tapasanun has been working for Haver Analytics since 2013. She has 20+ years of working in the financial services industry. As Vice President and Economic Analyst at Globicus International, Inc., a New York-based company specializing in macroeconomics and financial markets, Winnie oversaw the company’s business operations, managed financial and economic data, and wrote daily reports on macroeconomics and financial markets. Prior to working at Globicus, she was Investment Promotion Officer at the New York Office of the Thailand Board of Investment (BOI) where she wrote monthly reports on the U.S. economic outlook, wrote reports on the outlook of key U.S. industries, and assisted investors on doing business and investment in Thailand. Prior to joining the BOI, she was Adjunct Professor teaching International Political Economy/International Relations at the City College of New York. Prior to her teaching experience at the CCNY, Winnie successfully completed internships at the United Nations. Winnie holds an MA Degree from Long Island University, New York. She also did graduate studies at Columbia University in the City of New York and doctoral requirements at the Graduate Center of the City University of New York. Her areas of specialization are international political economy, macroeconomics, financial markets, political economy, international relations, and business development/business strategy. Her regional specialization includes, but not limited to, Southeast Asia and East Asia. Winnie is bilingual in English and Thai with competency in French. She loves to travel (~30 countries) to better understand each country’s unique economy, fascinating culture and people as well as the global economy as a whole.

More Economy in Brief

Global

Global