Global| Feb 12 2026

Global| Feb 12 2026Charts of the Week: AI-Led Growth Meets Monetary Divergence

by:Andrew Cates

|in:Economy in Brief

Summary

While markets have been unsettled at times by shifting policy expectations, geopolitical noise and questions around valuation, underlying global macroeconomic signals remain broadly supportive. Upgrades to Blue Chip consensus growth forecasts for parts of Asia — led by Taiwan — point to the tangible impact of the AI-driven tech cycle, a theme reinforced by the sharp rebound in semiconductor exports from South Korea (charts 1 and 3). At the same time, revisions to inflation forecasts underline a growing divergence in monetary policy paths, with easing still expected in the US and UK, while tighter stances persist elsewhere (chart 2). Importantly, there is little evidence so far that global supply-chain pressures are re-emerging in a way that would reignite inflation, notwithstanding lingering trade policy tensions (chart 4). Against this backdrop, rising policy uncertainty — particularly in the US — stands out as a potential source of risk, with implications for asset pricing and risk premia (chart 5). Yet the improvement in global sentiment surveys and a continued run of positive economic surprises suggest that markets are responding not just to policy noise, but to a genuinely resilient and improving macroeconomic environment (chart 6).

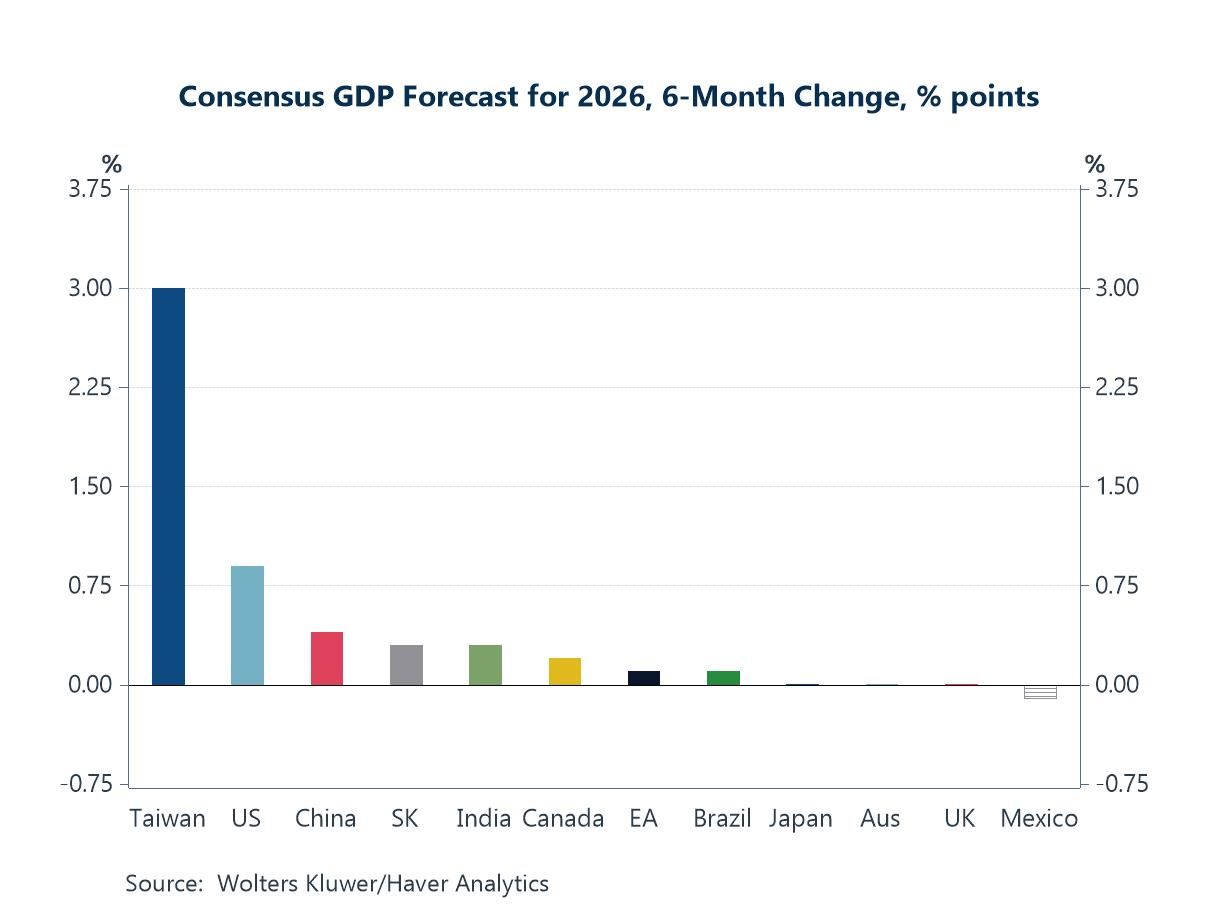

The Blue Chip Growth Consensus The first chart this week highlights a striking feature of recent forecast revisions: the outperformance of Asia, and Taiwan in particular. Over the past six months, Blue Chip panelists have upgraded their 2026 GDP growth forecasts most aggressively for Taiwan, far outpacing revisions elsewhere. This reflects the central role Taiwan plays in the global AI supply chain, especially in advanced semiconductors, where demand linked to data centres, AI accelerators and high-performance computing continues to strengthen. More broadly, positive revisions across parts of Asia suggest that the current AI-driven investment cycle is not just a US story, but one that is increasingly feeding through global tech supply chains, boosting exports, industrial production and capital spending across the region. In contrast, forecast changes elsewhere remain far more muted, underscoring how tightly the near-term growth impulse from AI is concentrated in economies most directly exposed to the semiconductor and hardware build-out.

Chart 1: The Blue Chip Growth Consensus for 2026, 6-month changes

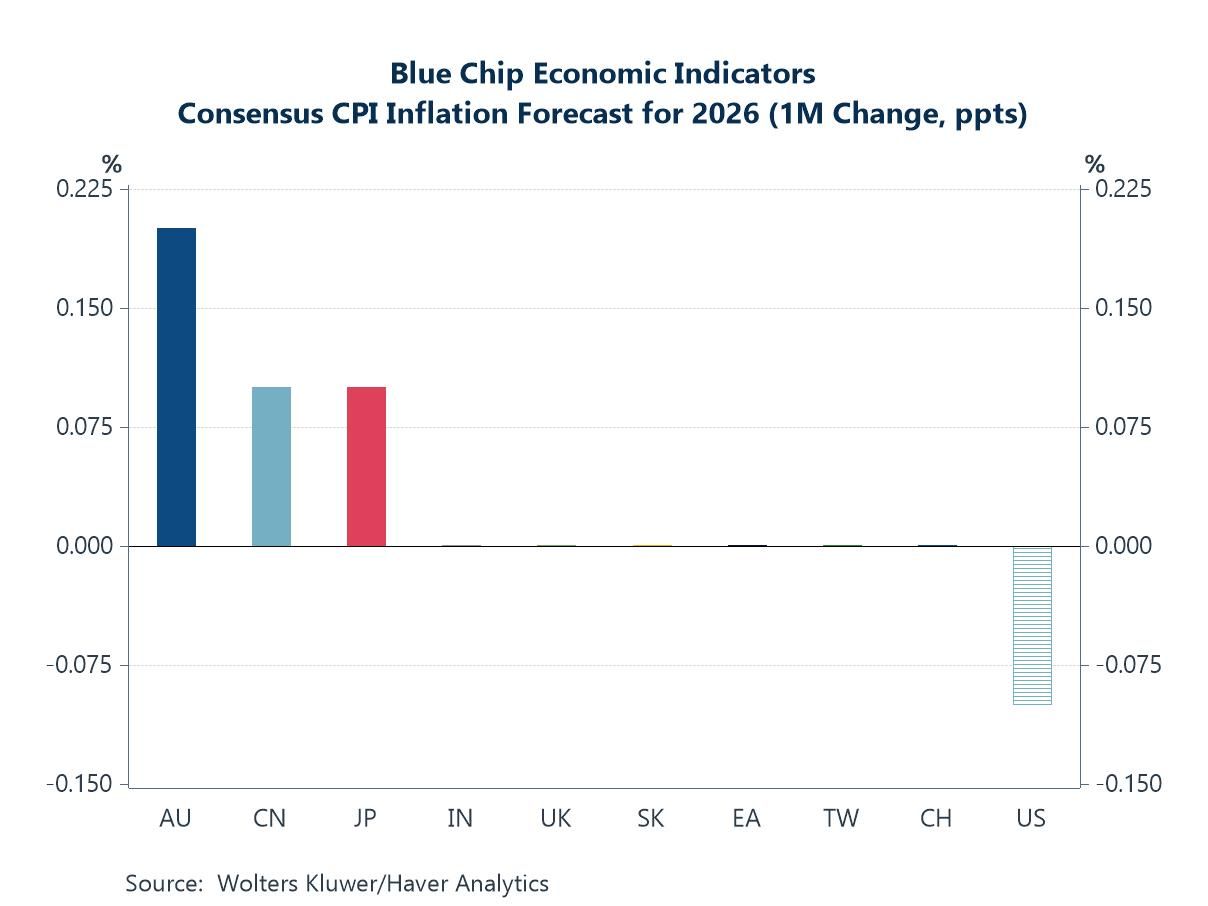

The Blue Chip Inflation Consensus The second chart highlights a growing theme of cross-country divergence, this time through the lens of inflation and monetary policy. Recent changes to Blue Chip CPI forecasts for 2026 show upward revisions in economies such as Japan, Australia and Canada, where inflation pressures are proving more persistent and policy tightening is either already under way or increasingly expected. In contrast, inflation forecasts in the US have been revised lower, consistent with softer recent data and reinforcing expectations of further monetary easing. The result is an increasingly asymmetric global policy backdrop: some central banks are still leaning against residual inflation risks, while others are preparing to shift toward rate cuts. This divergence, moreover, could matter more for global capital flows, exchange rates and financial conditions in the period ahead.

Chart 2: The Blue Chip Inflation Consensus for 2026, 1-month change

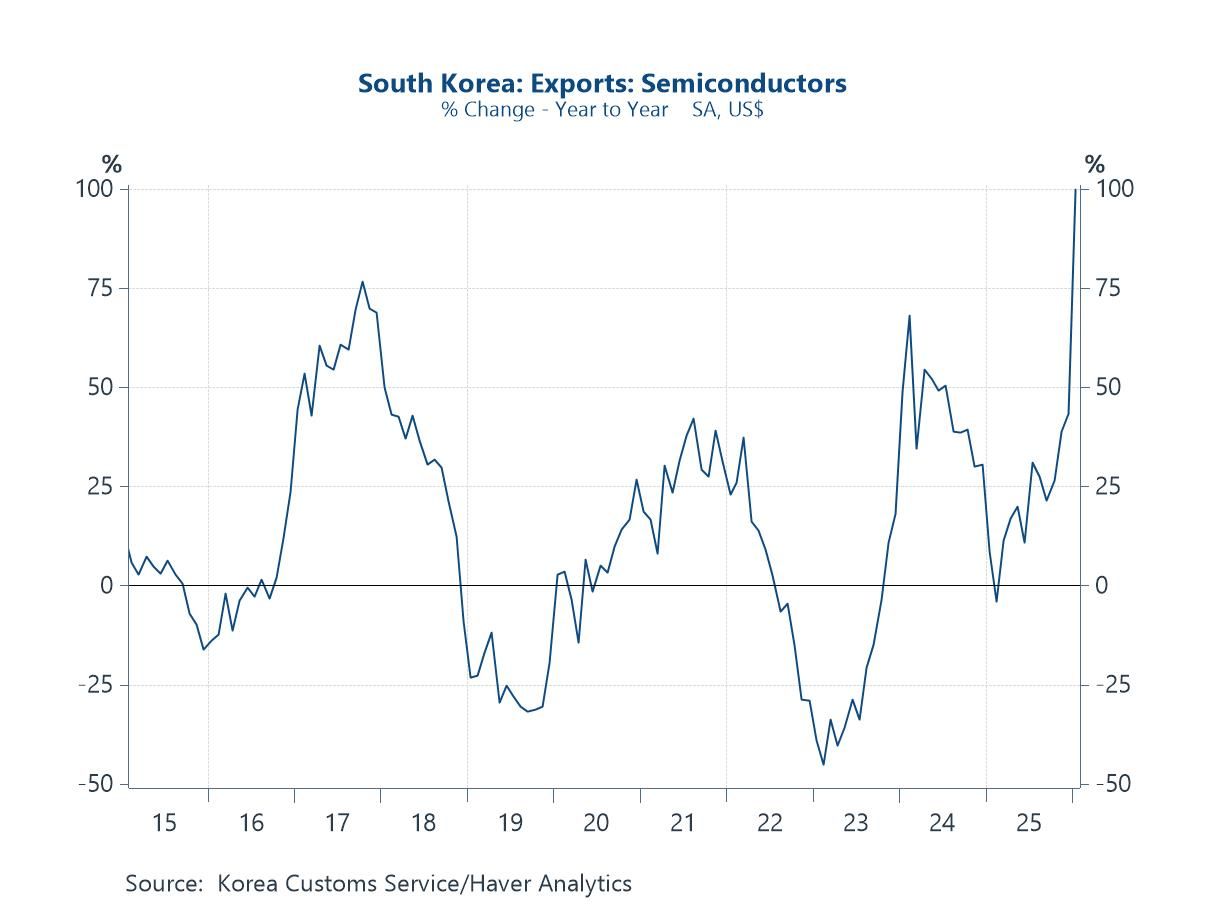

South Korea’s Semiconductor Trade The third chart provides a concrete, high-frequency illustration of the forces underpinning the forecast upgrades seen earlier for Asia. South Korea’s semiconductor exports have surged sharply on a year-on-year basis, marking one of the strongest upswings of the past decade and underscoring the revival of the global tech cycle. This acceleration is closely linked to AI-related demand, particularly for advanced memory chips used in data centres and high-performance computing. Alongside Taiwan, South Korea sits at the core of the AI hardware supply chain, and the strength of semiconductor exports helps explain why growth expectations in parts of Asia have been revised higher so decisively. In this sense, the chart offers a real-economy counterpart to the consensus forecast revisions: the AI boom is not just a financial or expectations story, but one that is already showing up clearly in trade and industrial data across the region.

Chart 3: South Korea’s semiconductor exports

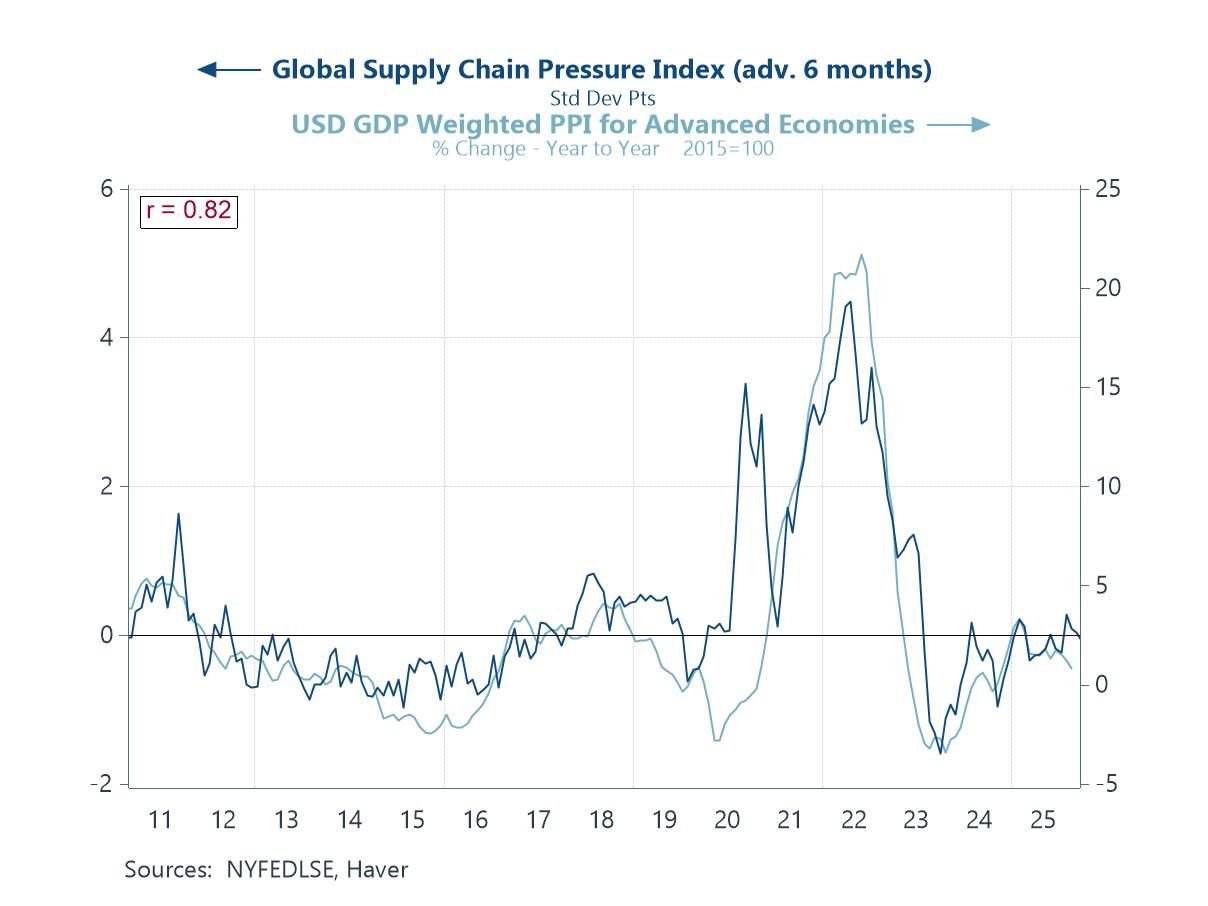

Global Supply Chain Pressures The fourth chart places recent inflation dynamics in a broader supply-chain context and offers little evidence that current US tariff policies are materially exacerbating global bottlenecks. The Global Supply Chain Pressure Index has remained close to historical norms in recent months, a sharp contrast with the extreme dislocations seen during the pandemic period. Consistent with this, producer price inflation across advanced economies has remained muted, reinforcing the tight relationship between supply-chain stress and upstream price pressures. While tariffs may still influence relative prices at the margin and contribute to sector-specific adjustments, the data do not point to a broad-based resurgence in supply-chain pressures of the kind that would generate renewed, systemic inflationary pressure.

Chart 4: Global Supply Chain Pressures versus G10 PPI inflation

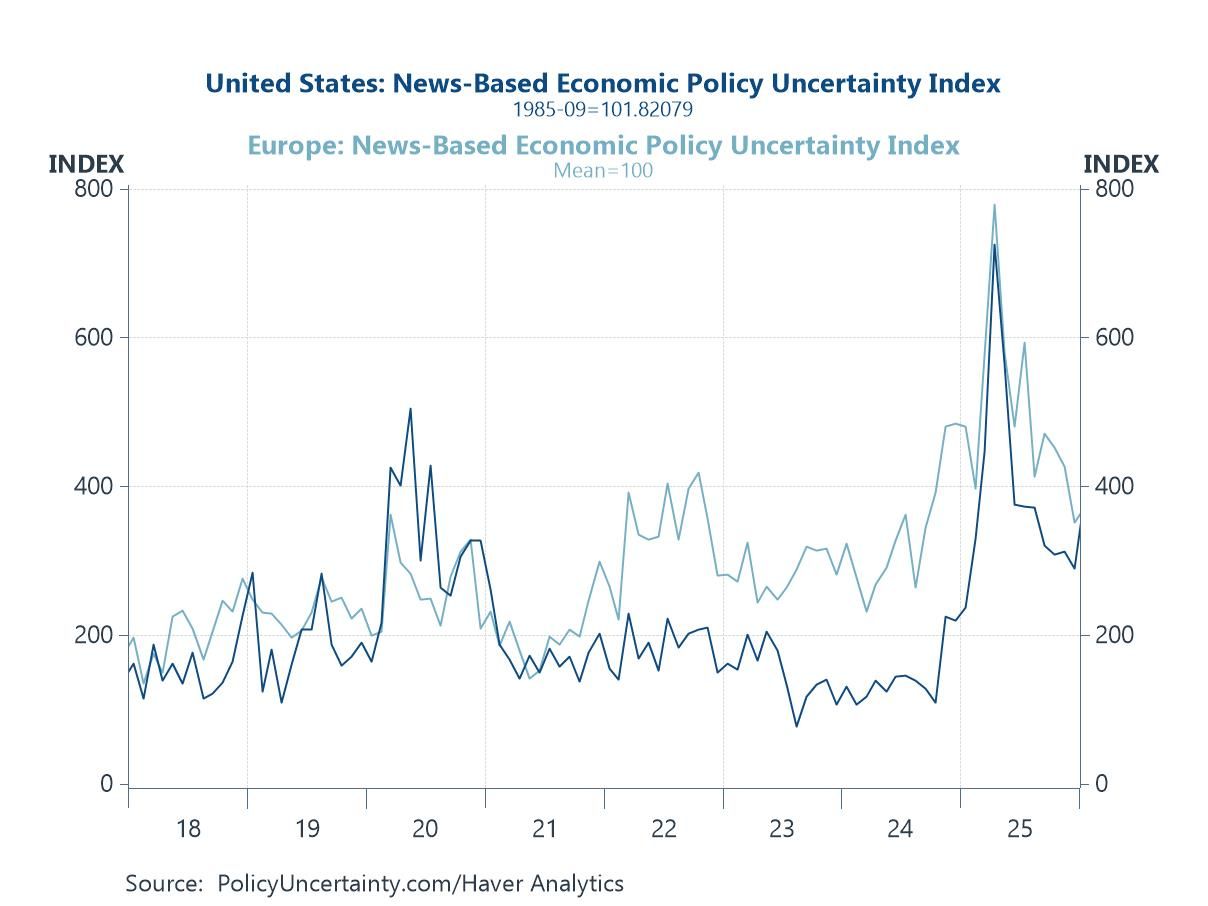

Uncertainty in the US versus Europe The fifth chart highlights a striking shift in the global policy uncertainty landscape. The US news-based economic policy uncertainty index has risen sharply and is now approaching levels more typically associated with Europe — a vivid contrast with the post-GFC and post-pandemic period, when US policy uncertainty was consistently well below European norms. This convergence likely reflects a combination of factors: renewed uncertainty around US trade policy and tariffs, questions over fiscal sustainability and debt dynamics, and growing debate around institutional independence, including the role of the Federal Reserve. At the same time, political polarisation and an increasingly unpredictable policy environment have become more prominent features of the US backdrop. The implications are potentially important for markets. A sustained rise in policy uncertainty would argue for a higher risk premium on US assets, particularly if it begins to influence corporate investment decisions, capital flows or the perceived safe-haven status of US markets.

Chart 5: Uncertainty indexes in the US versus Europe

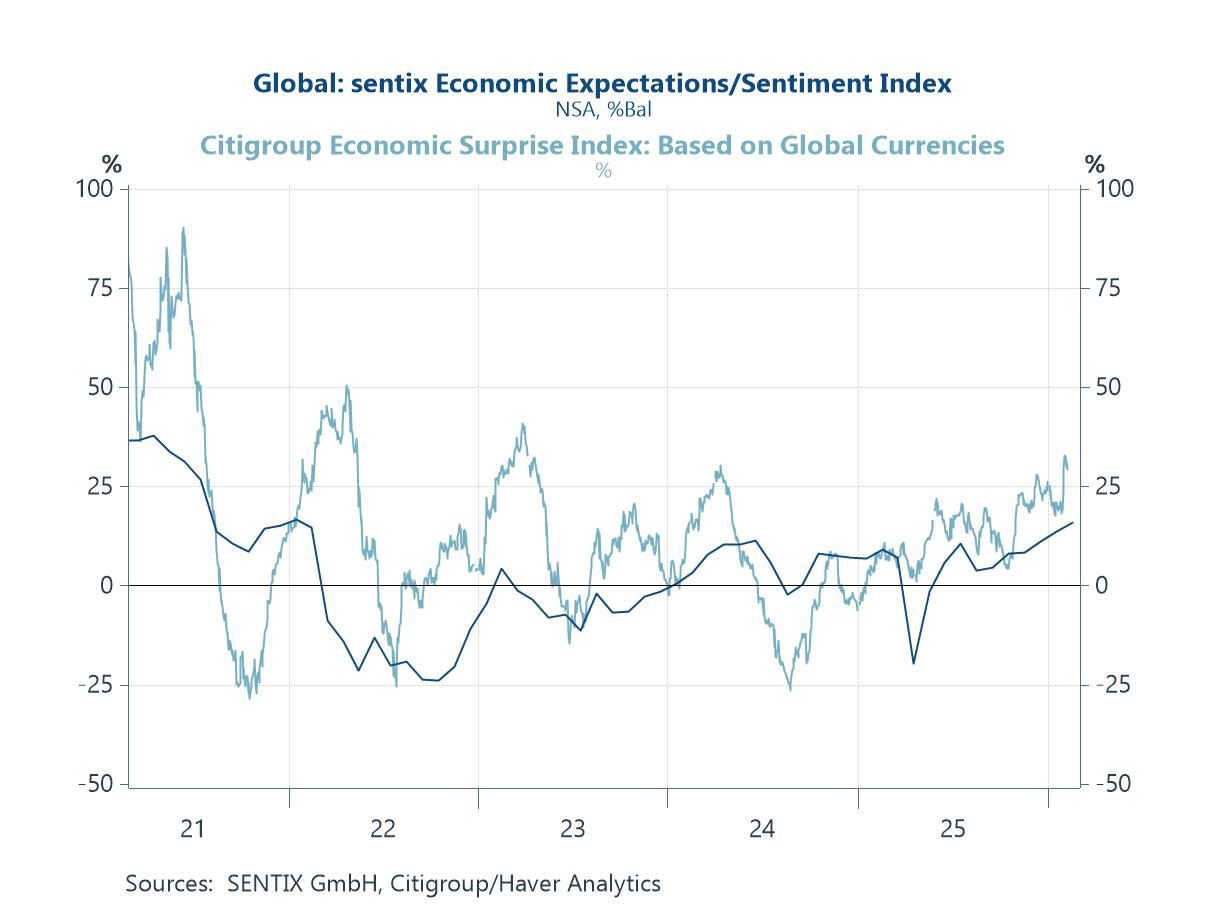

The Global Business Cycle The final chart brings the story together by highlighting a further strengthening in global economic sentiment in February. The Sentix global expectations index moved higher alongside a renewed run of positive economic surprises across a number of major economies, as captured by the Citi Global Economic Surprise Index. This combination points to an environment in which incoming data have consistently exceeded expectations, helping to reinforce investor confidence and support risk appetite. Taken together, the improvement in sentiment and the upside surprise in activity data underscore the constructive macroeconomic backdrop that markets have been responding to in recent months — one characterised by resilient growth, easing inflation pressures and still-supportive financial conditions, even as policy paths and regional dynamics continue to diverge.

Chart 6: The global sentix expectations index versus global growth surprises

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief