January Employment Report: The Labor Market Has a Pulse

Summary

• The increase in employment in January was firm, although narrowly based. • The unemployment rate dipped for the second consecutive month, led by strong employment as measured by the household survey. • The benchmark revision included with this report showed that job growth in much of 2024 and early 2025 was softer than previously believed.

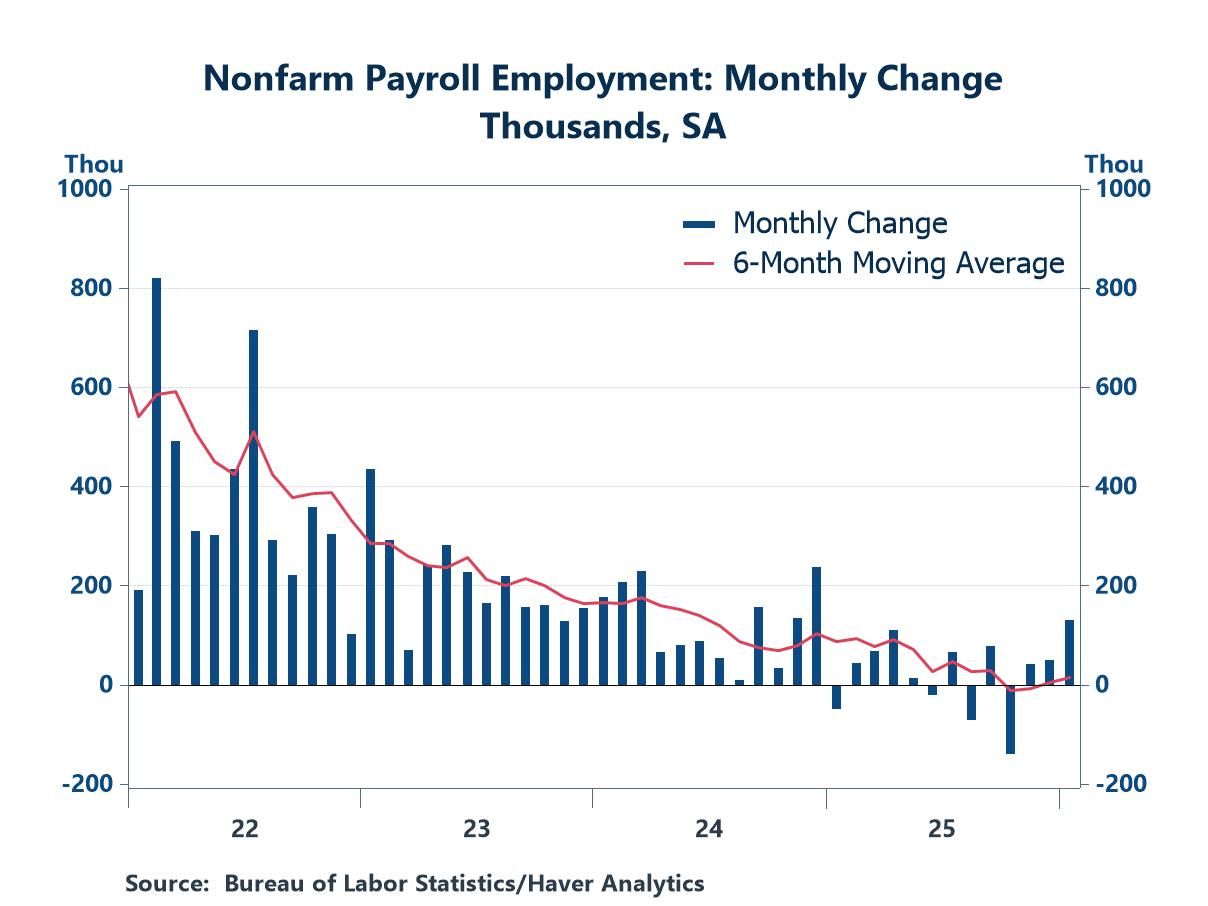

Nonfarm payroll employment rose 130,000 in January, notably better than the expected increase of approximately 50,000 and far better than the average monthly gain of 15,000 in 2025. Some observers might not be impressed because the increase was concentrated in the health-care and social-services category (124,000), which is not especially sensitive to the business cycle. In addition, the increase in this category was unusually sharp, suggesting the possibility of random volatility. The increase was the largest since the summer of 2020, when pandemic-related noise was driving activity.

To be sure, the employment gain outside of health-care and social-services was modest, but the report carried some bright spots nonetheless. The construction sector, which is highly sensitive to business conditions, rose sharply for the second time in the past three months (net gain of 65,000). Similarly, employment in business services, another area sensitive to the business cycle, rose for the third consecutive month, a marked shift from declines in nine of the prior ten months. The manufacturing sector added 5,000 jobs, a moderate change but a welcome break from 13 consecutive declines before January.

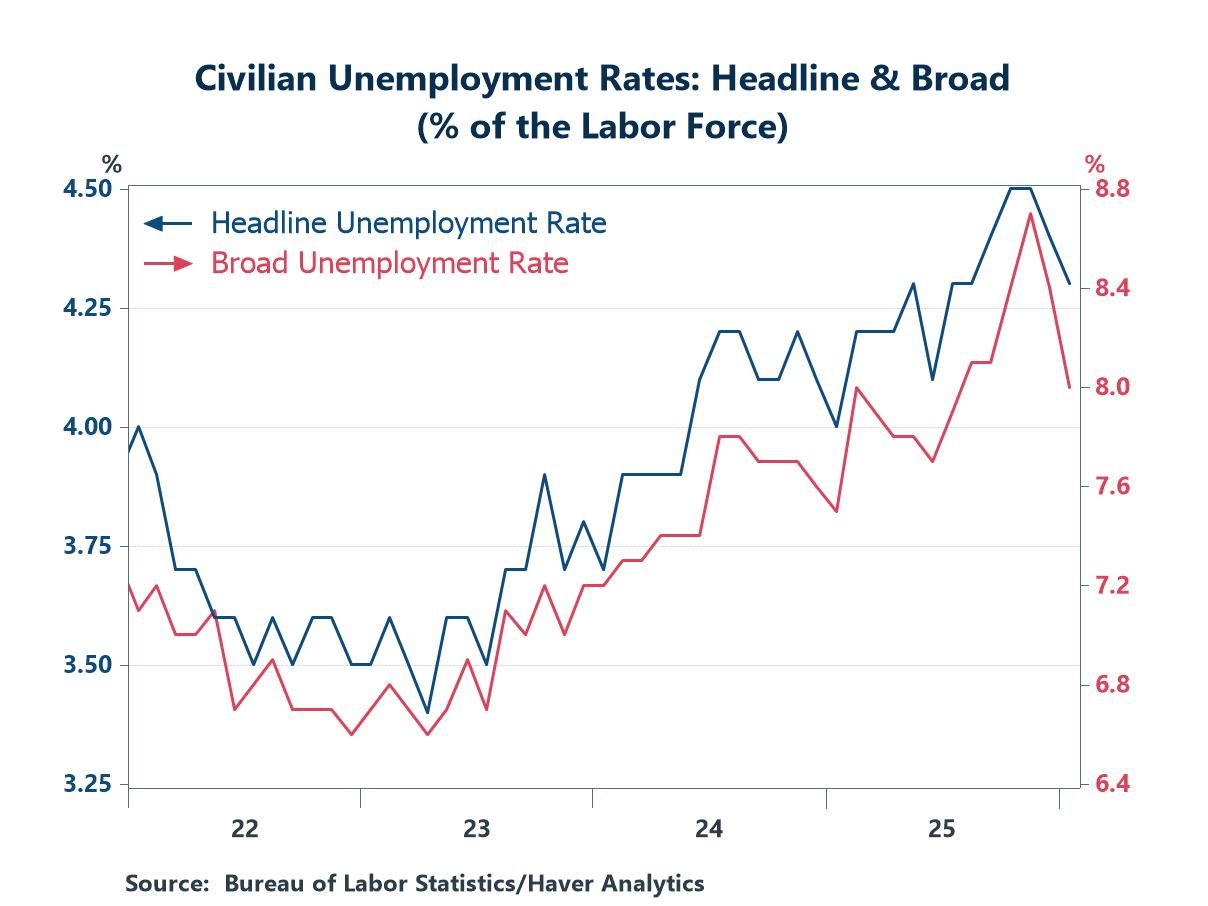

Results from the household survey also were favorable, with the unemployment dipping 0.1 percentage point for the second consecutive month. Also, it was a “strong” decline, with the drop reflecting a surge in employment as measured by the household survey (528,000) that exceeded a sharp increase in the size of the labor force (387,000). The broad unemployment rate (the so-calledU-6 measure) showed even sharper improvement (off 0.4 percentage point to 8.0%). Both of the two items added to the headline measure in the broad rate contribute to the decline. The number of individuals working part time for economic reasons fell 8.5% and the number of individuals marginally attached to the labor force fell 4.9%.

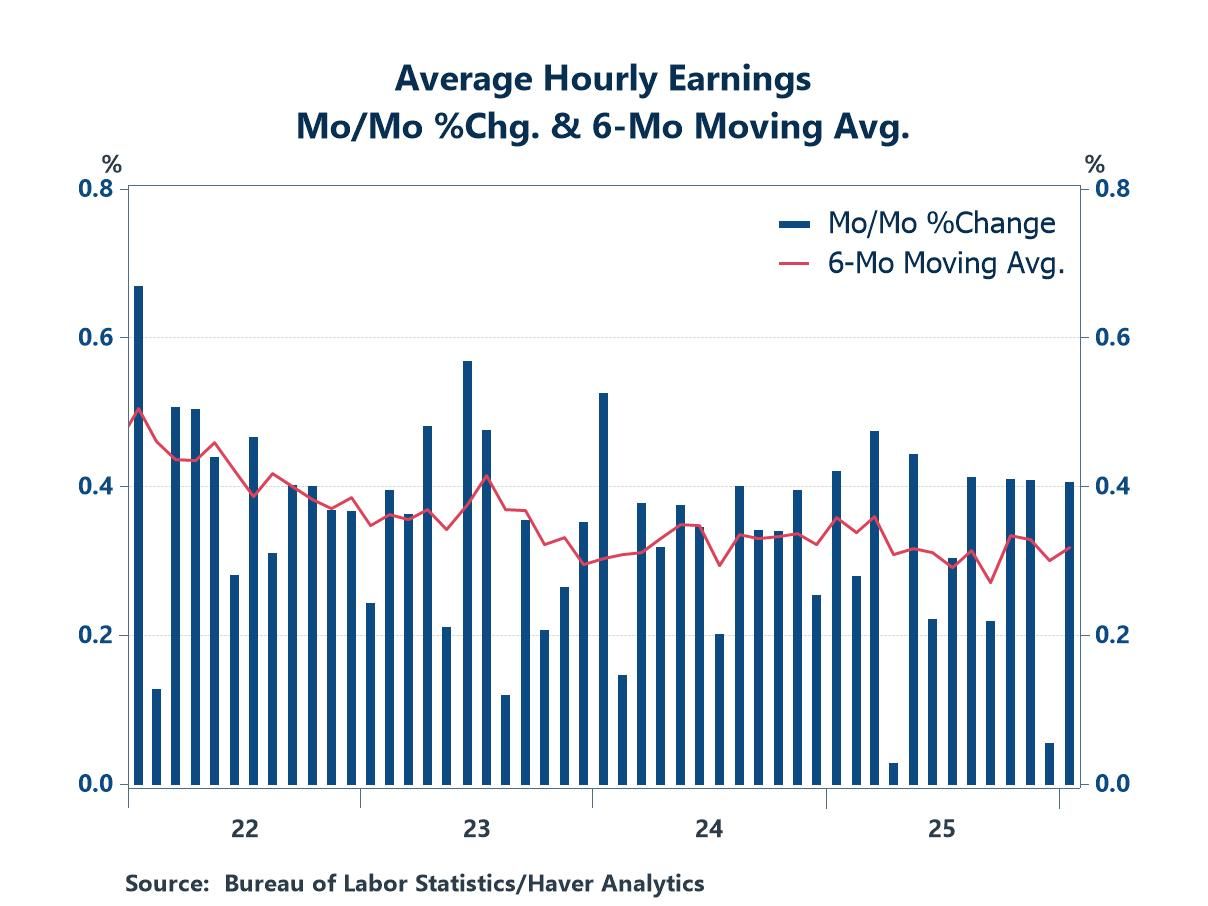

An increase of 0.4% in average hourly earnings could be viewed as a bright spot. The monthly change was in the upper end of the range from the past year or two, which left little change in the year-over-year increase (3.7%). The steady advance at a rate in excess of inflation shows that demand for workers has not evaporated.

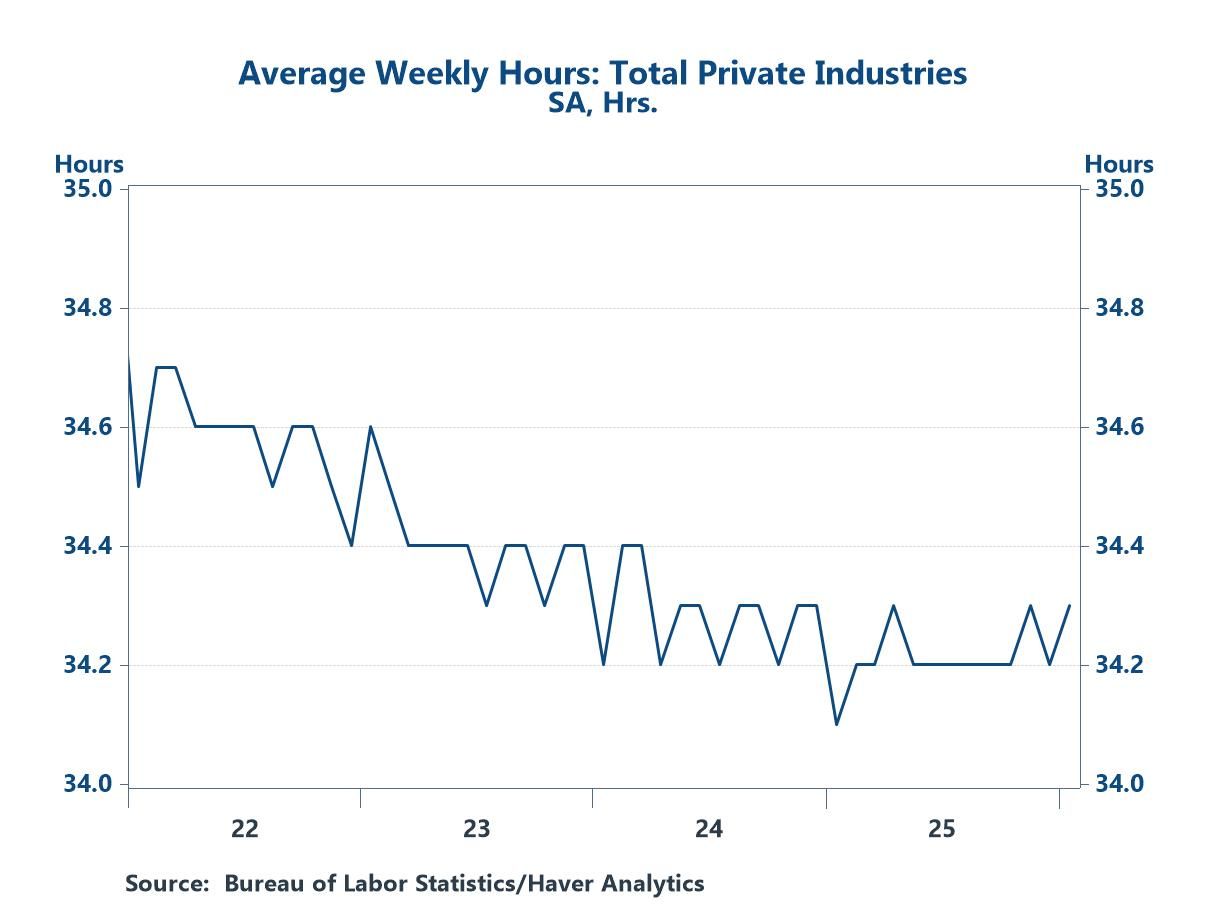

The length of the average workweek often receives scant attention in reviews of the labor market, but it can be an important variable. Businesses can alter the pace of activity by adjusting hours worked rather than changing payrolls, and thus, shifts in the workweek can signal changes in the tempo of the economy. Fortunately, the workweek has been steady recently, rising 0.1 hour in January and moving to the upper end of the tight range that has been in place for the past year or two.

While we judged the report to be favorable overall, it also contained some soft elements, as several industries posted slow job growth in January: transportation and warehousing (-11,000), information (-12,000), financial activity (-22,000), and the federal government (-34,000).

The annual benchmark adjustment also involved troublesome news. The universe job count taken as of March every year showed that total employment in March 2005 was 862,000 lower than previously believed (not seasonally adjusted). That revision left average monthly job growth from April 2004 to March 2005 (the period between the two benchmark months) at 76,000, down substantially from the average of 147,000 in the monthly reports (seasonally adjusted). Results from April to December 2025 also were nudged lower (monthly job growth of 13,000 rather than 28,000). The adjustments after the latest benchmark date reflected a recalibration of models used in the estimation process and the normal monthly adjustments in the prior two months of the latest survey. Revisions to seasonal factors back to 2021 also influenced all results.

The employment and earnings data are collected from surveys taken each month during the week containing the 12th day of the month. The labor market data are contained in Haver's USECON database. Detailed figures are in the EMPL and LABOR databases. The expectations figures are in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Asia

Asia