Consumer Price Index: Slow, but Steady, Deceleration

Summary

- The year-over-year change in the headline index moved to the bottom of its recent range.

- The annual change in the core index moved to a new low for the current cycle.

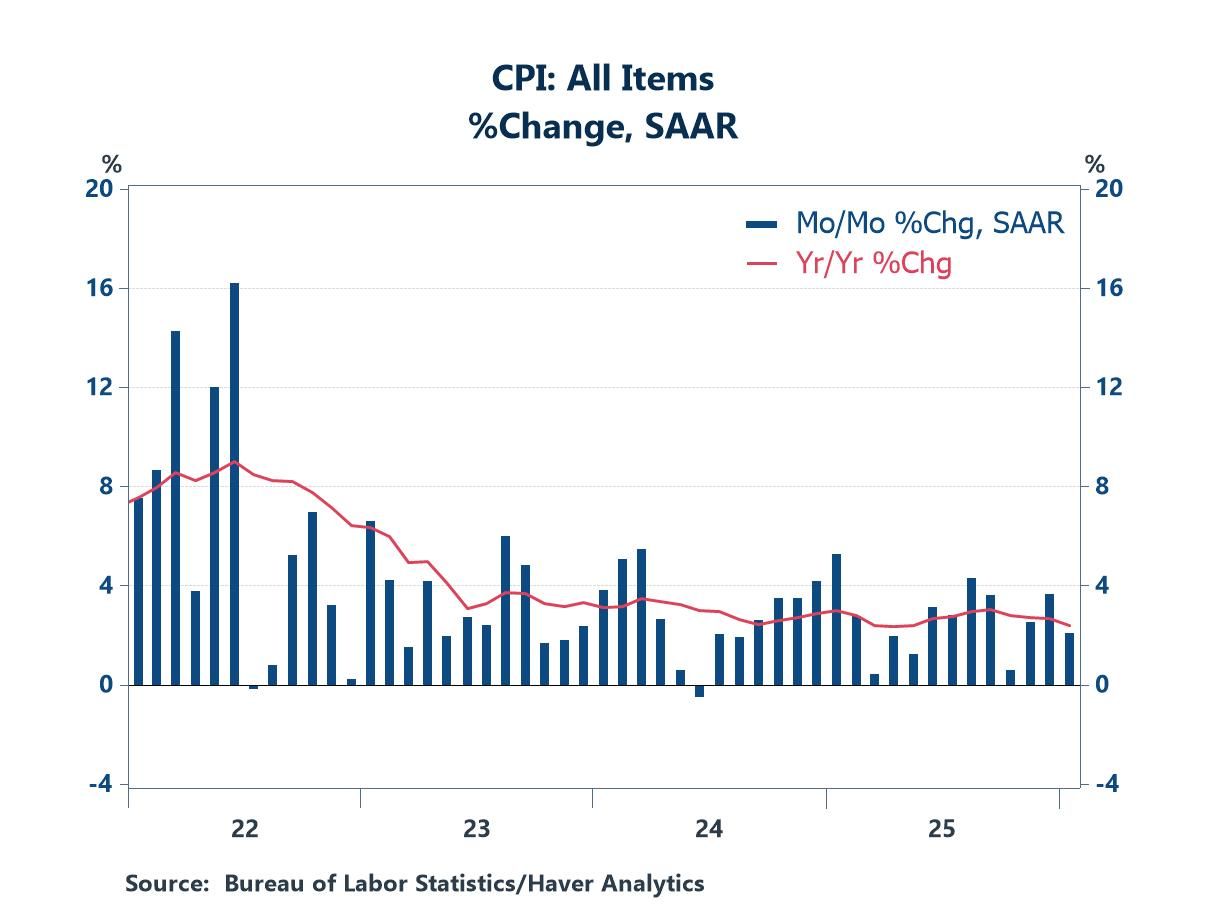

The consumer price index rose 0.2% in January, slower than the expected increase of 0.3% (and it rounded up to reach the published advance – 0.17% when calculated with more precision; annual rate of 2.04%). The latest monthly increase left the year-over-year at 2.4%, down from a recent high of 3.0% in September and bested by only one other recent reading: 2.3% in April of last year.

A drop of 1.5% in energy prices helped to contain the headline index. The drop was led by sharp retreats in the prices of both fuel oil and gasoline (off 5.7% and 3.2%, respectively). Energy prices have jumped around from month-to-month, but they have stayed within a narrow range in the past two years. Food prices rose 0.2% in January after a surge of 0.7% in the prior month. The food category experienced severe pressure during the inflation burst in 2022 (peak of 11.4%). Pressure settled in 2024, with annual food inflation easing to a low of 2.0% in August of that year. However, prices picked up again in 2025, with the year-over-year increase moving to 3.2% in August and staying close to that pace in subsequent months. The year-over-year increase in January totaled 2.9%.

The core component (ex food and energy) rose 0.3% in January, one of the sharpest advances of the past year or so. However, the increase was not especially troubling, as it was influenced by a jump of 6.5% in airfares, which added nearly a full tenth percentage point to the core component (0.08%). Airfares often move erratically, and the ups and downs in the past few years have left little net change. Discounting, most likely, will unfold in coming months. Even with the jump in airfares, the year-over-year increase in core prices moved to a new low for the current period of deceleration (2.5%). Core inflation appeared to be picking up in the spring and summer of last year (a recent peak of 3.1% in August), but pressure has eased since then.

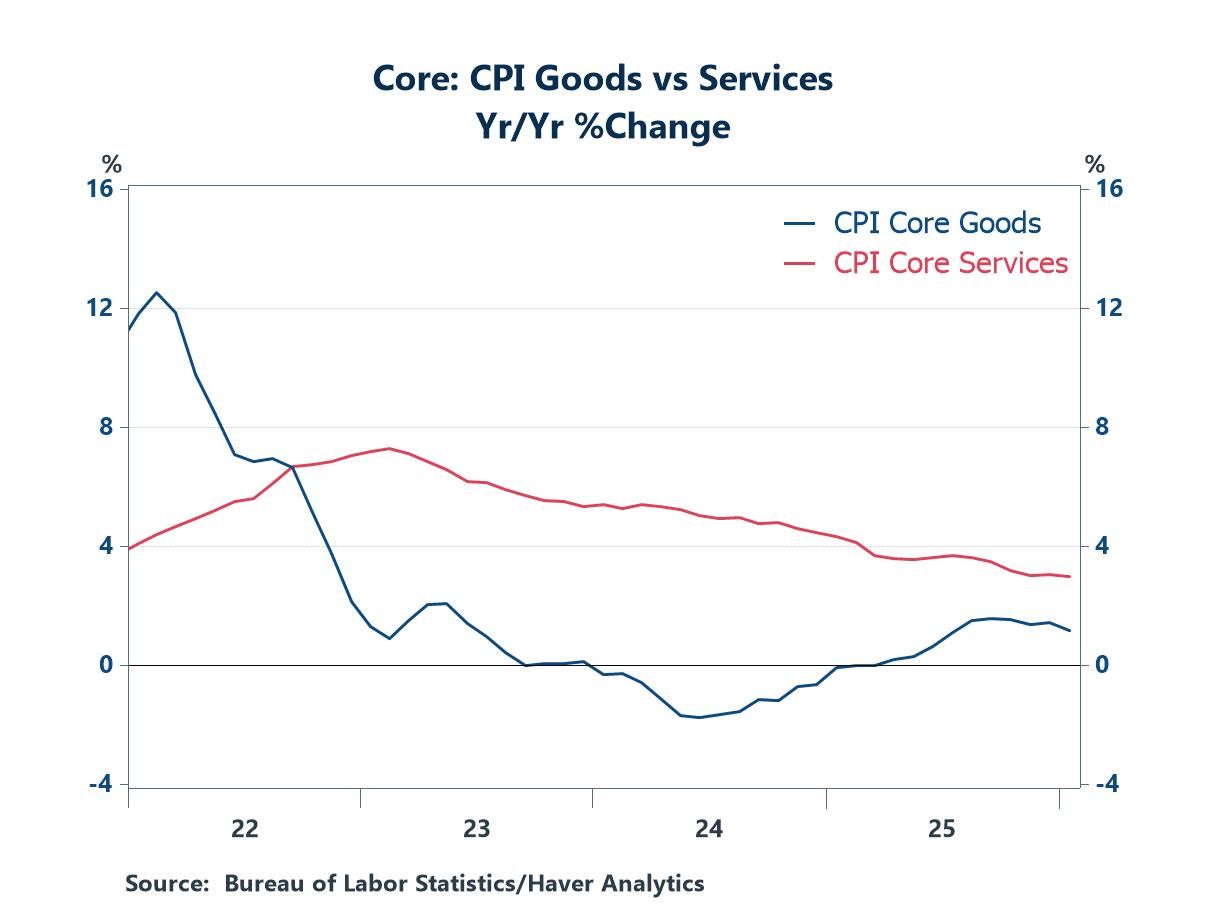

The source of the waxing and waning in core prices lies primarily in the goods component of the CPI. Goods prices were declining noticeably in the first half of 2024 (deflation!), but, they began to shift direction in the second half of 2024 and moved to price increases in 2025. The upward trend seems to have peaked at 1.5% in September and October, with the year-over-year change easing to 1.1 percent in January. Service prices have been decelerating over the past few years, but the rate of decline began to slow last year, and the latest months have shown no further improvement, stuck at 3.0% in the past three months.

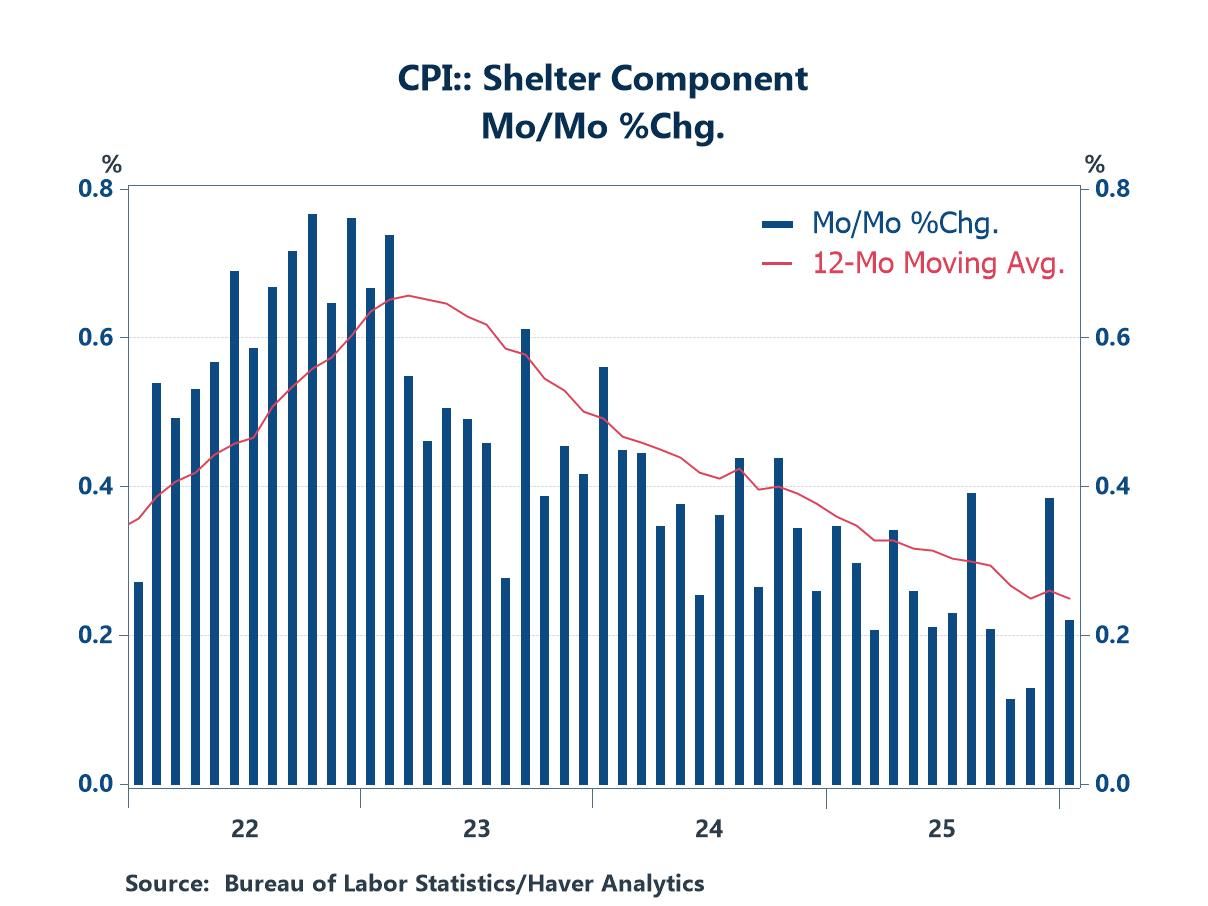

Within the core component, the movement of housing costs is notable. Rental rates rose 0.2% in January, a marked shift from the experience in 2022 and 2023, when increases in excess of 0.6% were common. This component jumps around from month-to-month, but the downtrend is unmistakable. After peaking at 8.2% in 2022, the latest year-over-increase totaled 3.0% in January.

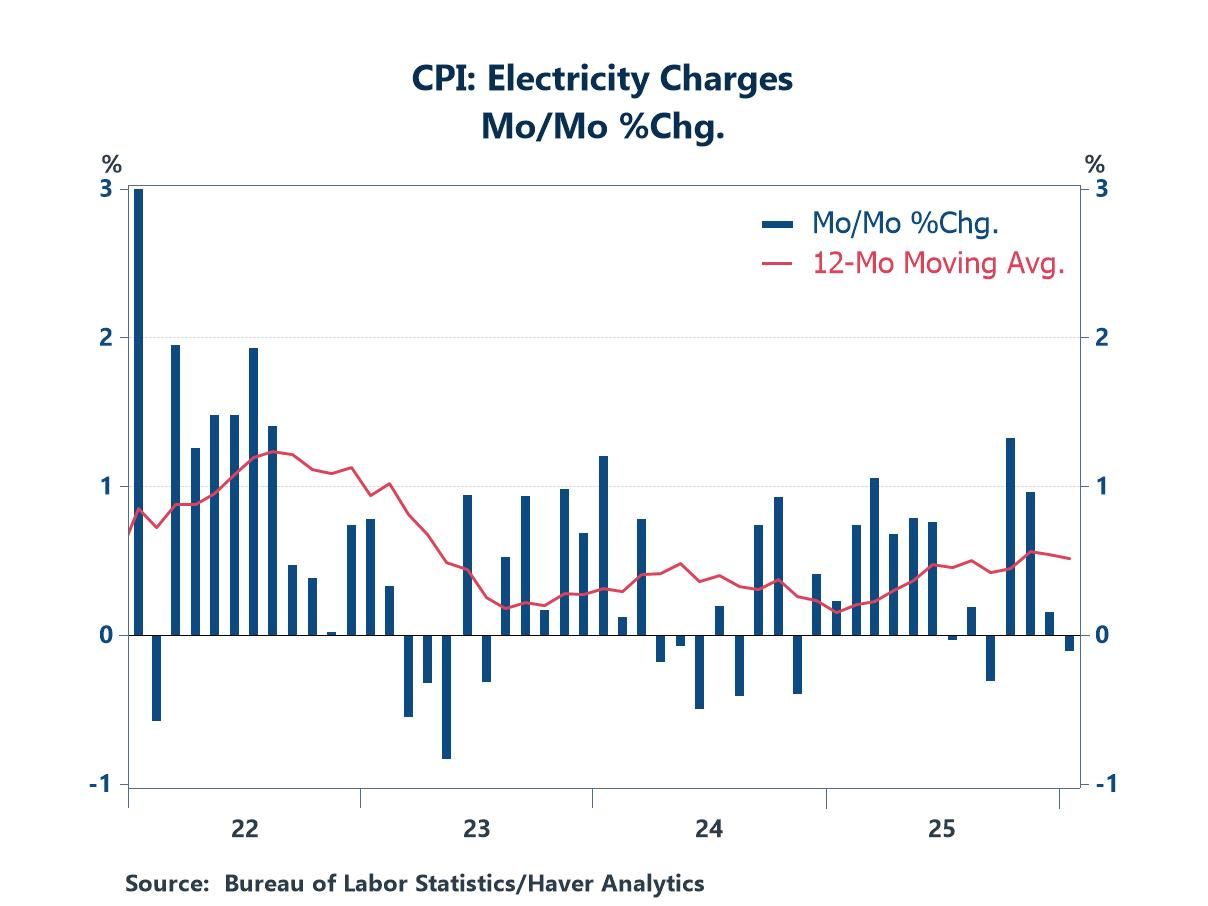

The cost of electricity is now gathering the attention of the public and politicians because of the pressure being exerted by the infrastructure requirements of artificial-intelligence. Costs were tame in January (down 0.1%), but increases have largely been the norm in the past year or so. The year-over-year increase totaled 6.3% in January, down from 7.0% in November but still a challenge for many households. Many observers are expecting more upward pressure down the road. Some observers perhaps recall (and fear) the experience in 2022, when electricity inflation touched 15.8%.

The Consumer Price figures can be found in Haver's USECON database. The expectations figure is contained in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Asia

Asia