Global| Jan 12 2010

Global| Jan 12 2010U.S. Trade Deficit Increases With Economic Recovery

by:Tom Moeller

|in:Economy in Brief

Summary

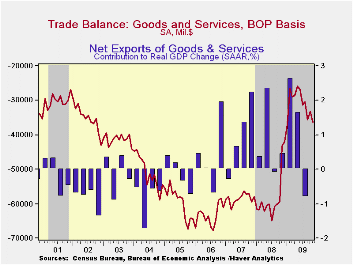

Economic recovery hit the U.S. trade accounts with a double-whammy during November. It generated a 2.6% m/m rise in imports and it increased the international trade deficit to $36.4B which was the highest since January. The rise [...]

Economic

recovery hit the U.S. trade accounts with a double-whammy during

November. It generated a 2.6% m/m rise in imports and it increased the

international trade deficit to $36.4B which was the highest since

January. The rise followed October's deficit of $33.2B which

was revised up slightly from the initial estimate. Export growth lagged

with a 0.9% increase that followed two months of stronger increase. The

latest figure was quite a bit higher than Consensus expectations for a

deficit of $34.5B.

Economic

recovery hit the U.S. trade accounts with a double-whammy during

November. It generated a 2.6% m/m rise in imports and it increased the

international trade deficit to $36.4B which was the highest since

January. The rise followed October's deficit of $33.2B which

was revised up slightly from the initial estimate. Export growth lagged

with a 0.9% increase that followed two months of stronger increase. The

latest figure was quite a bit higher than Consensus expectations for a

deficit of $34.5B.

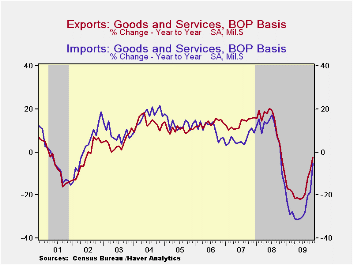

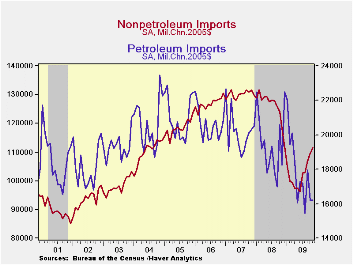

Imports rose 2.6% in part due to a rise in crude

oil prices to $72.54 per barrel which was the highest level since

October of 2008. Overall, however, the gain in petroleum imports was

held back by a 4.6% m/m decline (-8.2% y/y) in the quantity of

energy-related products. U.S. economic recovery continued to be

apparent in a 1.5% increase (-6.3% y/y) in real nonoil imports which

was the fifth increase in six months. Real non-auto capital goods

imports jumped 3.5% (-13.0% y/y) after a 2.8% September rise. Real

nonauto consumer goods imports surged 3.7% and by 12.5% since June.

These are turnarounds from earlier sharp declines. Real automotive

vehicles & parts imports, however, slipped 0.4% (-0.1% y/y) but

they were up by one-half since the spring. Real capital goods imports

also have been strong and rose 3.6% for the fourth increase in five

months. They have risen 14.5% since June. Finally, services imports

rose a modest 0.3% (-4.0% y/y) for the fifth increase in six months.

U.S. travels abroad were discouraged by the lower dollar. Travel

imports slipped 0.9% (-7.1% y/y and passenger fares rose 1.5% (-25.6%

y/y).

These are turnarounds from earlier sharp declines. Real automotive

vehicles & parts imports, however, slipped 0.4% (-0.1% y/y) but

they were up by one-half since the spring. Real capital goods imports

also have been strong and rose 3.6% for the fourth increase in five

months. They have risen 14.5% since June. Finally, services imports

rose a modest 0.3% (-4.0% y/y) for the fifth increase in six months.

U.S. travels abroad were discouraged by the lower dollar. Travel

imports slipped 0.9% (-7.1% y/y and passenger fares rose 1.5% (-25.6%

y/y).

Reflecting the competitive value of the dollar, nominal exports rose 0.9% m/m and by 13.6% from the April low. Adjusted for price inflation, however, the gain is more impressive. Though real merchandise exports slipped 0.6% during November (-4.4% y/y), they have risen 13.9% since April. Offsetting a 5.4% decline (-2.3% y/y) decline in real non-auto consumer goods exports was a 9.0% rise in auto exports (-6.1% y/y) and a 0.4% uptick (-7.6% y/y) uptick in real capital goods exports. Exports of services ticked up 0.2% (-0.8% y/y) following earlier strong monthly gains.

By country, the trade deficit

with mainland China lessened to $20.2B, its least since June, as

exports rose 41.4% y/y and imports fell 2.5%. With Japan, the trade

deficit deteriorated to $5.4B from 5.1B one year earlier as exports

fell 16.3% while imports fell just 4.4%. With the European Union, the

trade deficit deteriorated to $6.4B as exports declined 9.4% y/y and

imports fell a lesser 5.3%.

By country, the trade deficit

with mainland China lessened to $20.2B, its least since June, as

exports rose 41.4% y/y and imports fell 2.5%. With Japan, the trade

deficit deteriorated to $5.4B from 5.1B one year earlier as exports

fell 16.3% while imports fell just 4.4%. With the European Union, the

trade deficit deteriorated to $6.4B as exports declined 9.4% y/y and

imports fell a lesser 5.3%.

The international trade data can be found in Haver's USECON database. Detailed figures are available in the USINT database.

The Determinants of International Flows of U.S. Currency from the Federal Reserve Bank of New York can be found here.

| Foreign Trade | November | October | September | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| U.S. Trade Deficit | $36.4 | $33.2 | $35.7B | $43.2B (11/08) | $695.9 | $701.4 | $760.4 |

| Exports - Goods & Services | 0.9% | 2.7% | 2.8% | -2.3% | 11.2% | 13.2% | 13.3% |

| Imports - Goods & Services | 2.6% | 0.7% | 5.6% | -5.5% | 7.6 | 6.0% | 10.8% |

| Petroleum | 7.3% | -10.6% | 20.7% | 1.0% | 37.0% | 9.4% | 20.1% |

| Nonpetroleum Goods | 2.4% | 3.2% | 4.2% | -6.9% | 1.5% | 4.8% | 9.1% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief