Asia| Feb 02 2026

Asia| Feb 02 2026Economic Letter from Asia: The AI Resource Race

This week, we examine Artificial Intelligence through an Asian lens, focusing on how the region fits into the broader AI value chain. While the US clearly dominates at the frontier—spanning cutting-edge AI model capabilities, chip design, and data centres—it remains heavily reliant on more foundational segments of the value chain.

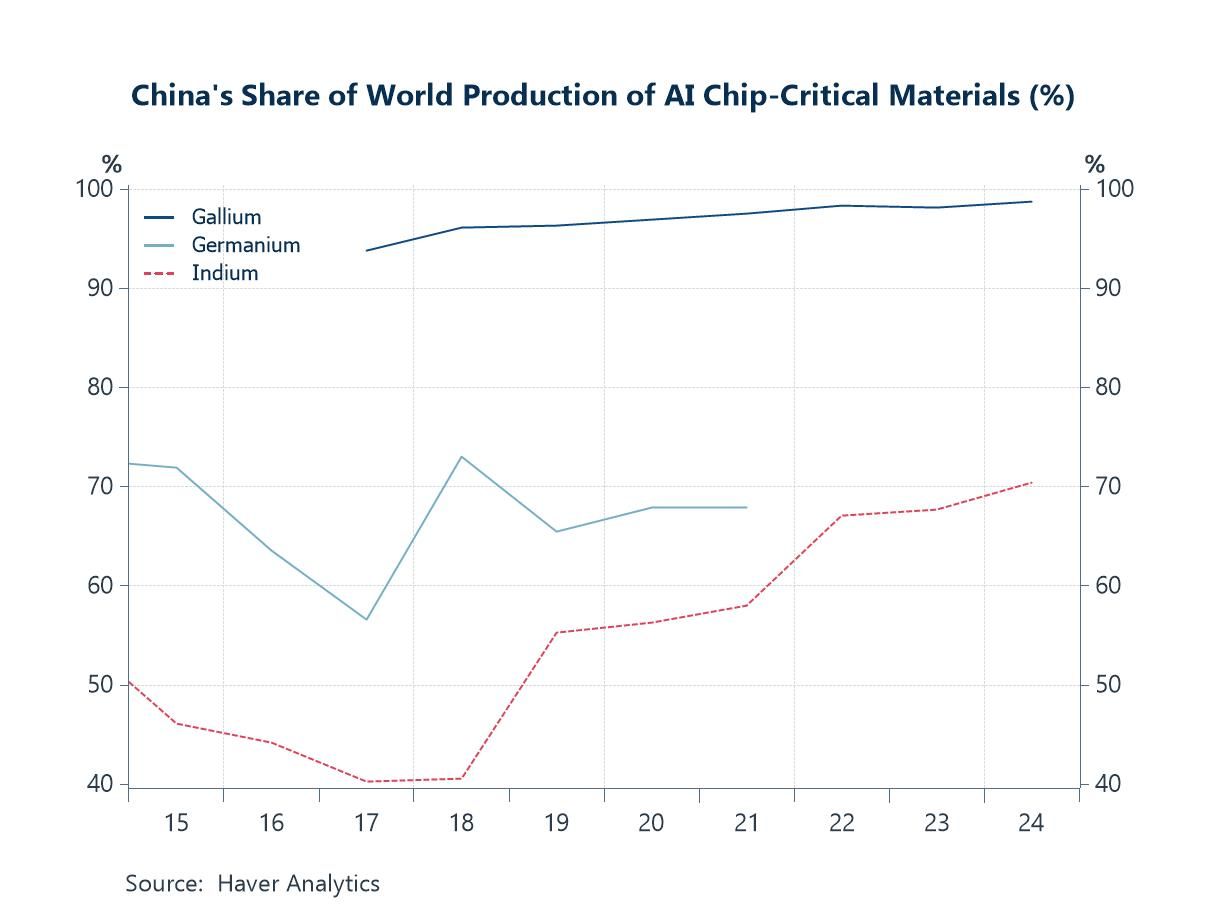

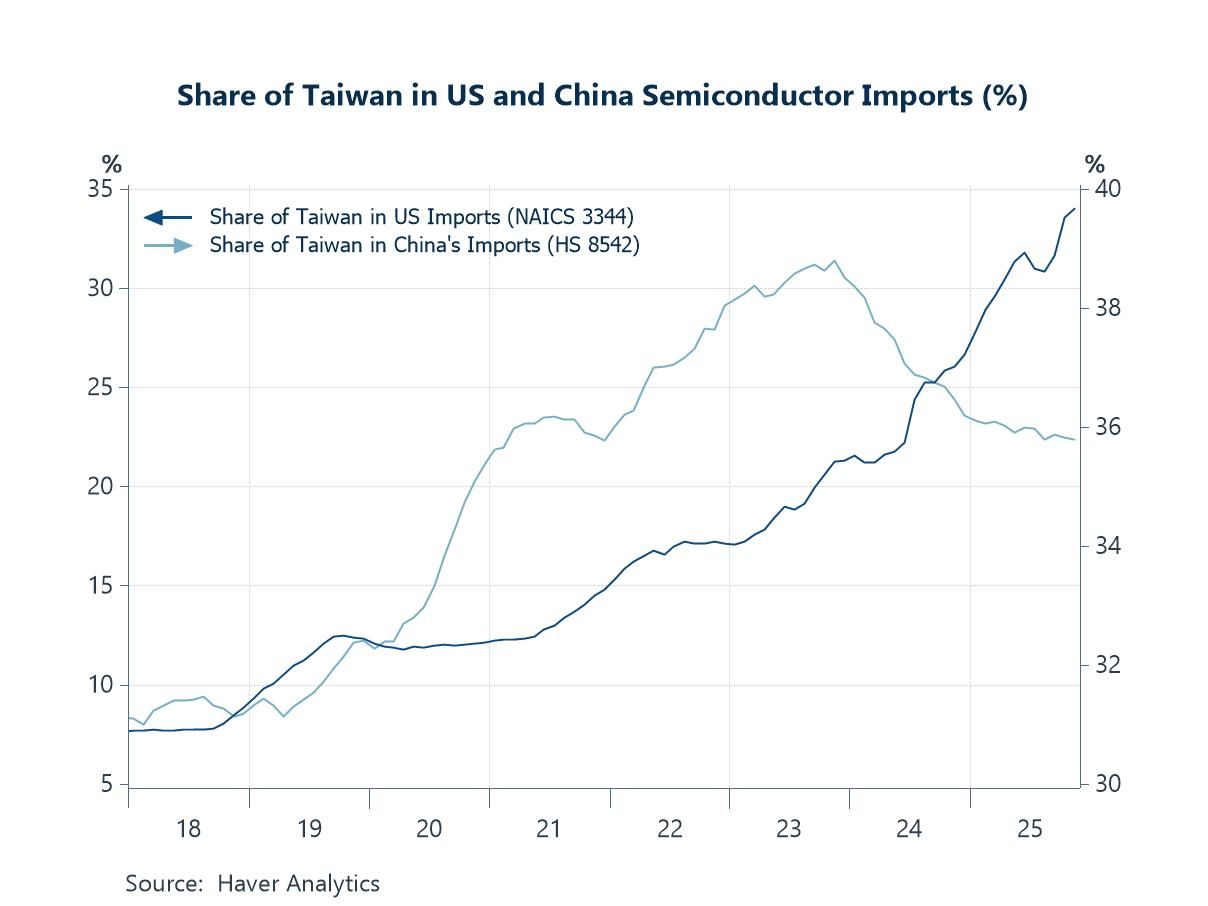

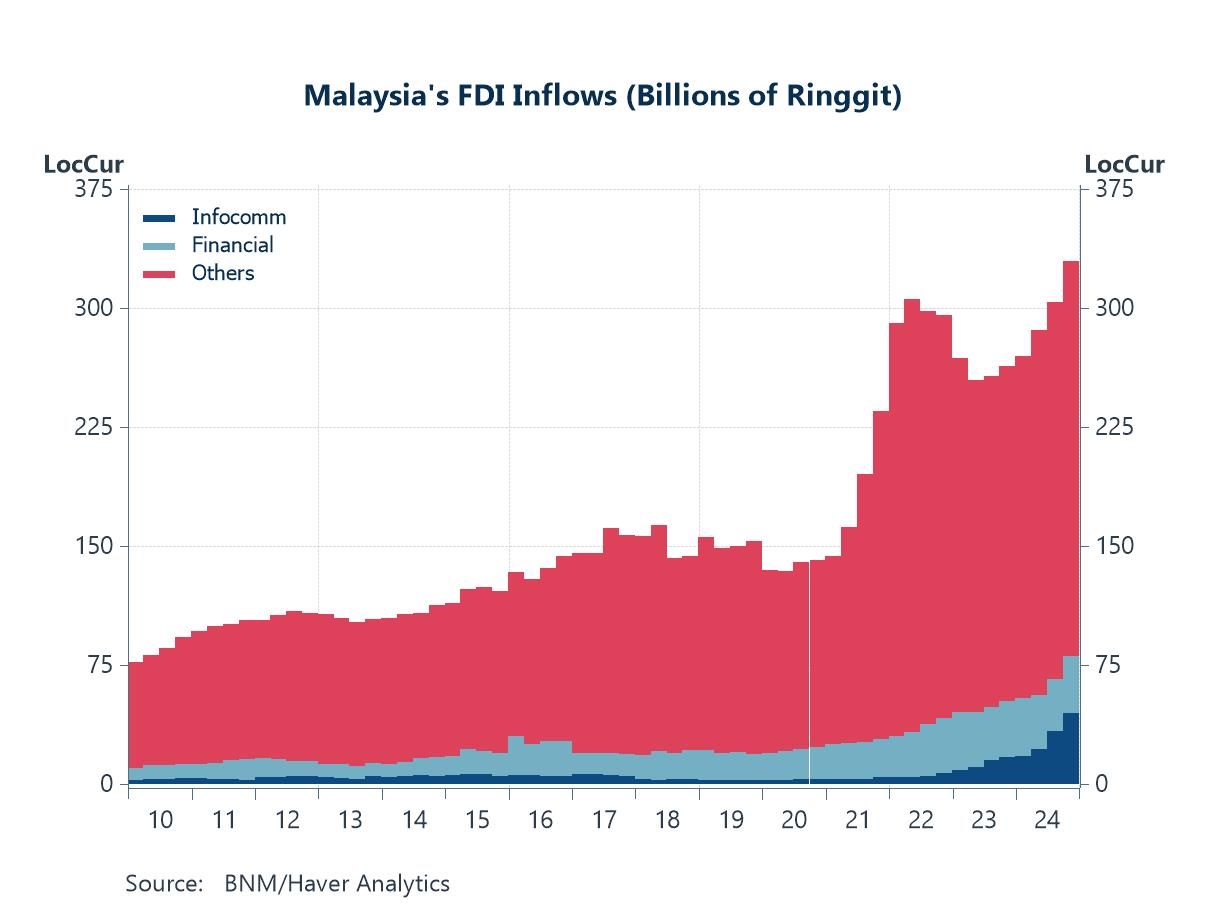

We begin with first principles, looking at the raw material inputs required to produce AI chips, where China continues to hold a dominant position (chart 1). We then turn to the chips themselves, highlighting Taiwan’s well-known leadership in advanced semiconductor manufacturing and its critical role for both the US and China (chart 2). That said, recent efforts by both the US and China to reduce external dependence are beginning to show up in the data (chart 3), and could reshape this landscape in the years ahead. Next, while the US still leads in data centre capacity—the infrastructure essential for training and deploying AI models—several Asian economies, notably Malaysia, are seeking to capture a larger share of this rapidly expanding segment. These efforts have been met with strong interest from global technology firms, translating into sizable foreign direct investment inflows (chart 4).

Underpinning the entire AI ecosystem, however, are rapidly rising electricity requirements. China is now the world’s largest consumer of electricity, while other aspiring AI players, including India, will also need to confront the growing energy demands that come with deeper participation in the AI space (chart 5). At the same time, economies that have made significant shifts toward certain renewable energy sources must contend with higher electricity prices. This may create pressure to slow—or in some cases reconsider—the pace of the green transition in order to remain competitive in the intensifying race for AI-related resources (chart 6).

AI chip material production We begin with the most critical raw inputs required to produce AI chips. Beyond silicon—the foundational material on which chips are built—China commands substantial market share and dominance in the production of other key chipmaking materials, notably gallium and germanium. China accounts for a near-total share of global gallium production and roughly 68% of germanium output (chart 1), levels that effectively give it the ability to steer these markets. China has demonstrated this leverage before, most recently through temporary export restrictions on critical minerals enacted last year amid tit-for-tat measures between the US and China. Those controls were eventually paused following a subsequent US–China trade agreement. Even so, the episode served as a stark reminder of China’s strong negotiating position in the semiconductor supply chain—despite the US retaining leadership in the sophistication and advancement of AI models.

Chart 1: China’s share of world production of critical AI chip materials

AI chip production Next, we revisit the production of AI chips themselves. This area has featured prominently in financial market discussions and, by extension, has driven sharp swings in tech-sector equity valuations in recent years. As is now widely understood, Taiwan remains by far the world’s leading producer of AI chips, serving as the primary import source for the two largest importers of these products: the US and China. While firms such as Nvidia lead in advanced chip design, it is typically Taiwanese manufacturers—most notably TSMC—that translate these designs into physical chips, turning blueprints into deployable products. To date, the depth of manufacturing expertise and production capability among major Taiwanese producers remains unrivalled, leaving the global AI chip industry heavily dependent on these firms for actual fabrication.

Chart 2: Share of Taiwan in US and China semiconductor imports

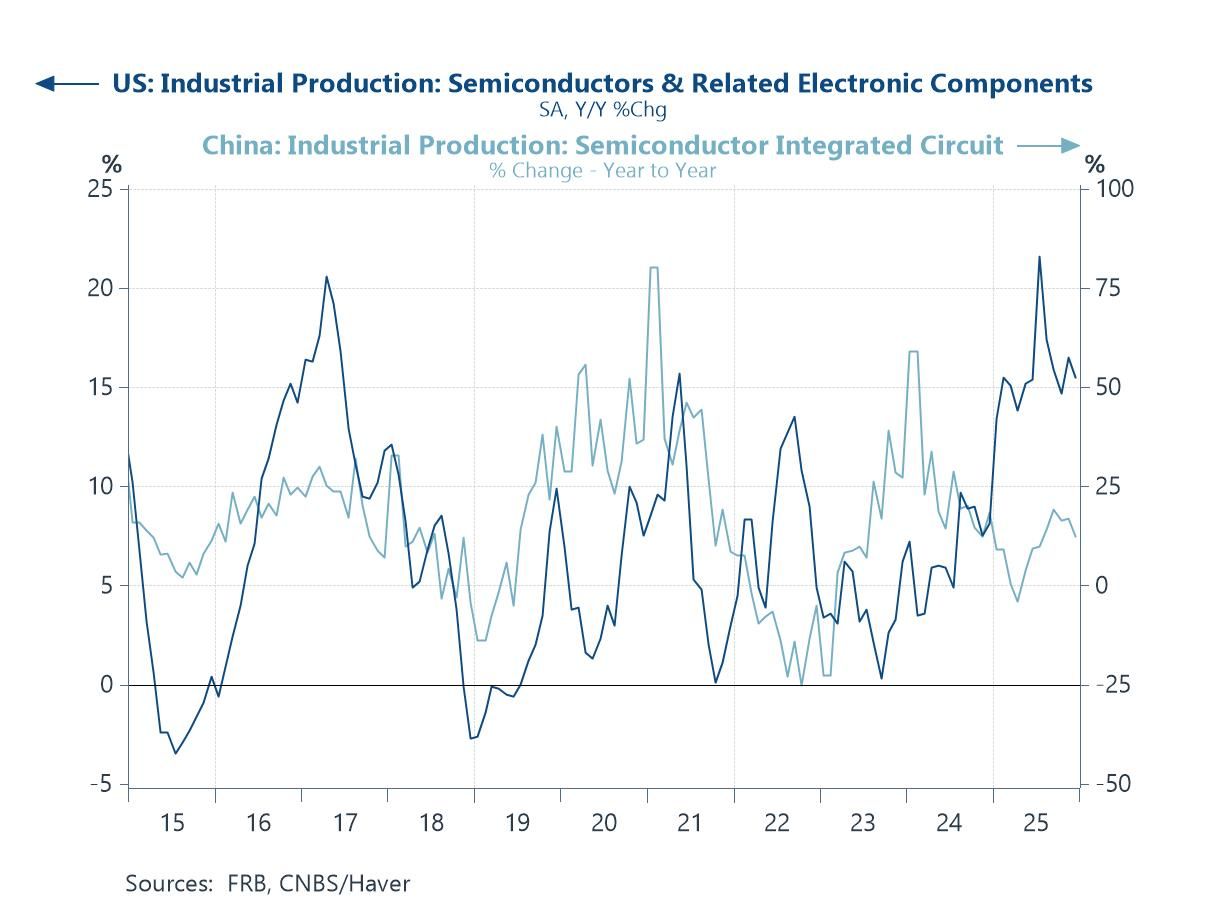

That said, recent major commitments by TSMC to expand manufacturing capacity in the US state of Arizona mark an important shift. These moves, which also culminated in a US–Taiwan trade deal, could gradually onshore more AI chip production to the US and reduce the heavy geographic concentration in Taiwan. That process, however, is likely to take several years to fully materialise. For China, earlier US efforts to restrict access to externally supplied AI chips—particularly at the high end—have also accelerated Beijing’s push toward greater self-reliance. Some middle ground has emerged more recently, with US approval for the sale of Nvidia’s older-generation H200 chips to China. These chips were reportedly approved conditionally by Chinese authorities for purchase by firms such as Alibaba, Tencent, ByteDance, and DeepSeek. Even so, the race to expand domestic capability and production—across not just the most advanced chips, but semiconductors more broadly—is now firmly under way in both the US and China, as shown in chart 3.

Chart 3: US and China semiconductor production

Data centres We next turn to a key component of the infrastructure underpinning AI models and systems: data centres. While the US and China host the bulk of global data centre capacity, several other Asian economies are positioning themselves to capture rising demand for this infrastructure as part of their broader growth strategies. Malaysia, for instance, has increasingly emerged as a viable destination for data centres, with major technology firms such as Google, Microsoft, and Amazon already having announced sizeable investments. More recently, India has also sought to claim a share of this rapidly expanding space, with the government rolling out generous incentives—including a tax holiday of up to two decades for foreign companies operating data centres in the country. That said, the construction and operation of data centres require substantial technical expertise and, at a more fundamental level, large and reliable energy supplies—a topic we turn to in the next section.

Chart 4: Malaysia FDI inflows by sector

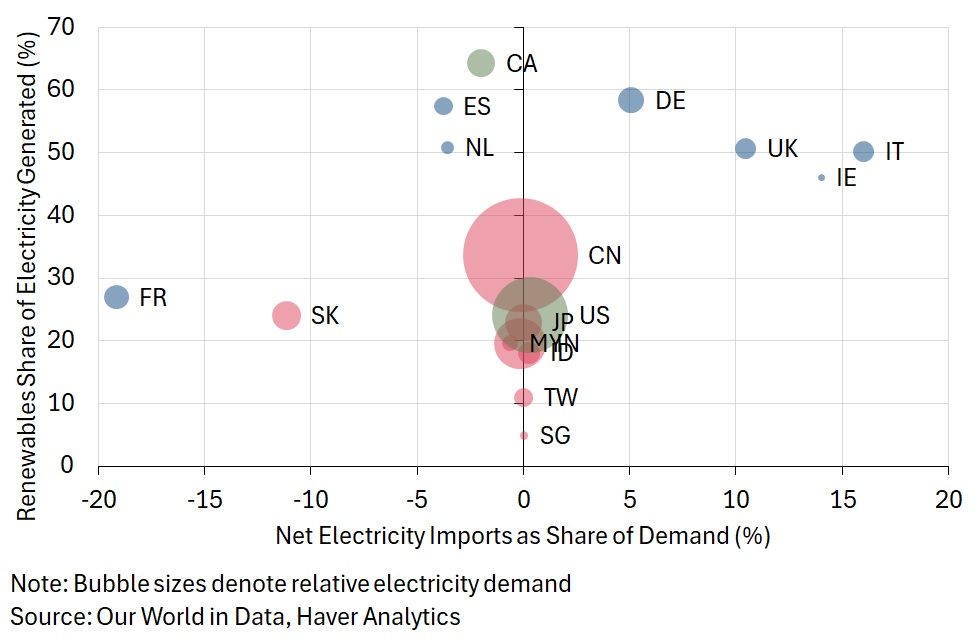

Energy Finally, we turn to the resource underpinning it all: energy. The immense electricity requirements associated with training and deploying AI models in data centres have become increasingly apparent. As a result, economies seeking to expand data centre capacity or capitalise on this wave of demand, such as Malaysia and India, must ensure that electricity supply grows commensurately. At present, China stands out as the world’s largest consumer of electricity. Based on 2024 data, it demanded more than 10,000 TWh over the year—exceeding the combined consumption of the next several major users, including the US, India, Russia, and Japan. As chart 5 illustrates, many developed economies, particularly in Europe, are also net importers of electricity, suggesting constraints in domestic generation capacity. However, even economies that are not net electricity importers may not be fully insulated from external energy dependencies, as they often rely on imported primary energy inputs—such as crude oil or gas—to generate electricity.

Chart 5: Electricity demand, renewables share, and import reliance

Additionally, many developed economies have, over the past decades, increased the share of renewable energy in their overall energy mix. While this shift is socially responsible, particularly in terms of reducing carbon footprints, it has also tended to coincide with higher electricity prices. This reflects the fact that many renewable energy sources have yet to reach efficiency levels that make them fully cost-competitive with fossil fuels. At the same time, geopolitical flashpoints, notably the Russia–Ukraine war, have underscored the risks of inadequate energy security. Repeated disruptions stemming from other tensions, including US trade actions, have further pushed past ambitions for a rapid green transition out of the spotlight Compounding these challenges, the immense energy demands associated with AI, together with the continued availability of relatively cheap fossil fuels, create a strong temptation for some countries to slow the pace of their energy transition—or, in some cases, risk reversing earlier progress. This challenge is also faced by Asian economies seeking to capture a larger share of the AI value chain.

Chart 6: Renewables energy share vs. electricity prices

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief