Global| Feb 02 2026

Global| Feb 02 2026S&P MFG PMIs Power Ahead; PMIs Improve; U.S. ISM blasts a hole through MFG Pessimism

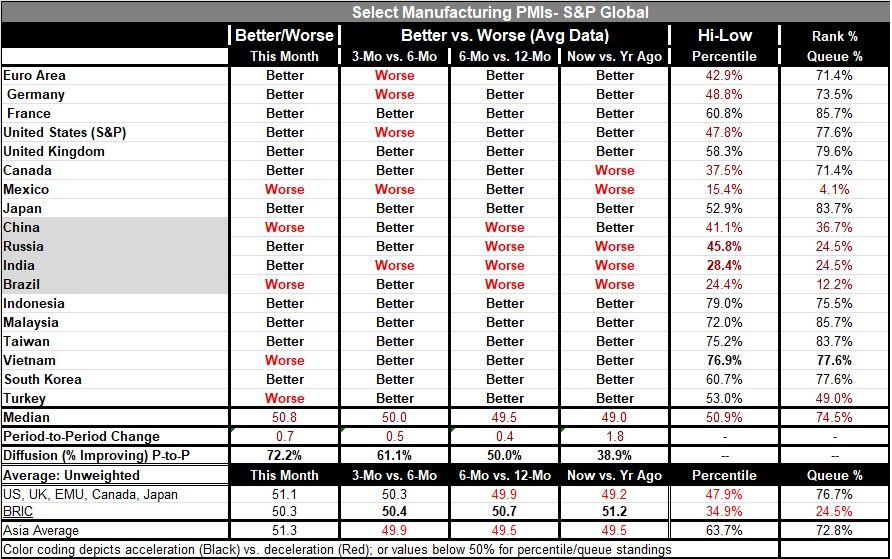

An unexpectedly happy New Year in manufacturing land It's a new year - and a fine new year it is, baby! S&P manufacturing PMIs are showing consistent and broad improvement on a monthly and sequential basis. In January, of the 18 early reporting countries only 5 showed worsening conditions. The median reading for the month moved to 50.8 in January from 50.1 in December and 49.0 in November. It's a slow-motion slog, but on the other hand, it is a steady up creep from November. The PMI's median is up by 1.8 points since November, which may be small potatoes, but it's still significant progress.

Over three months the median reading rises to 50.0, compared to a reading of 49.5 on average over six months and a reading of 49.0 on average over 12 months. These sequential readings are also showing slow but clear stepwise improvement.

Breadth In terms of breadth, in January 72.2% of the reporters showed month-to-month improvement, compared to 44% showing month-to-month improvement in December and 50% showing improvement in November. Yes, the recent performance has shown improvement versus deterioration, and in the two prior months, diffusion has been pretty close to a 50-50 proposition. Then, in January, the upside exploded to a 72.2 percentile reading. Sequential data show that over 12 months 38.9% of the reporters showed improvement compared to a year earlier; over six months 50% of the reporters showed improvement compared to performance over 12 months. Over three months there was improvement of 61.1% of the reporters compared to their six-month metrics.

Unexpected strength These are steady and consistent improving readings, with some explosive improvement in the most recent three-month or one-month periods. This report is really something that was quite unexpected since the trend has been flat, sitting in this position of minor contractive lethargy for quite some time.

Most reporters log readings that imply growth The percentile ranking data show that only six of the 18 countries—one third of reporters—have percentile readings below the 50th percentile, based on data going back to January 2022. 12 of the 18 reporters have percentile standings in the 70th percentile or higher, and 4 of 18 are in the 80th percentile range.

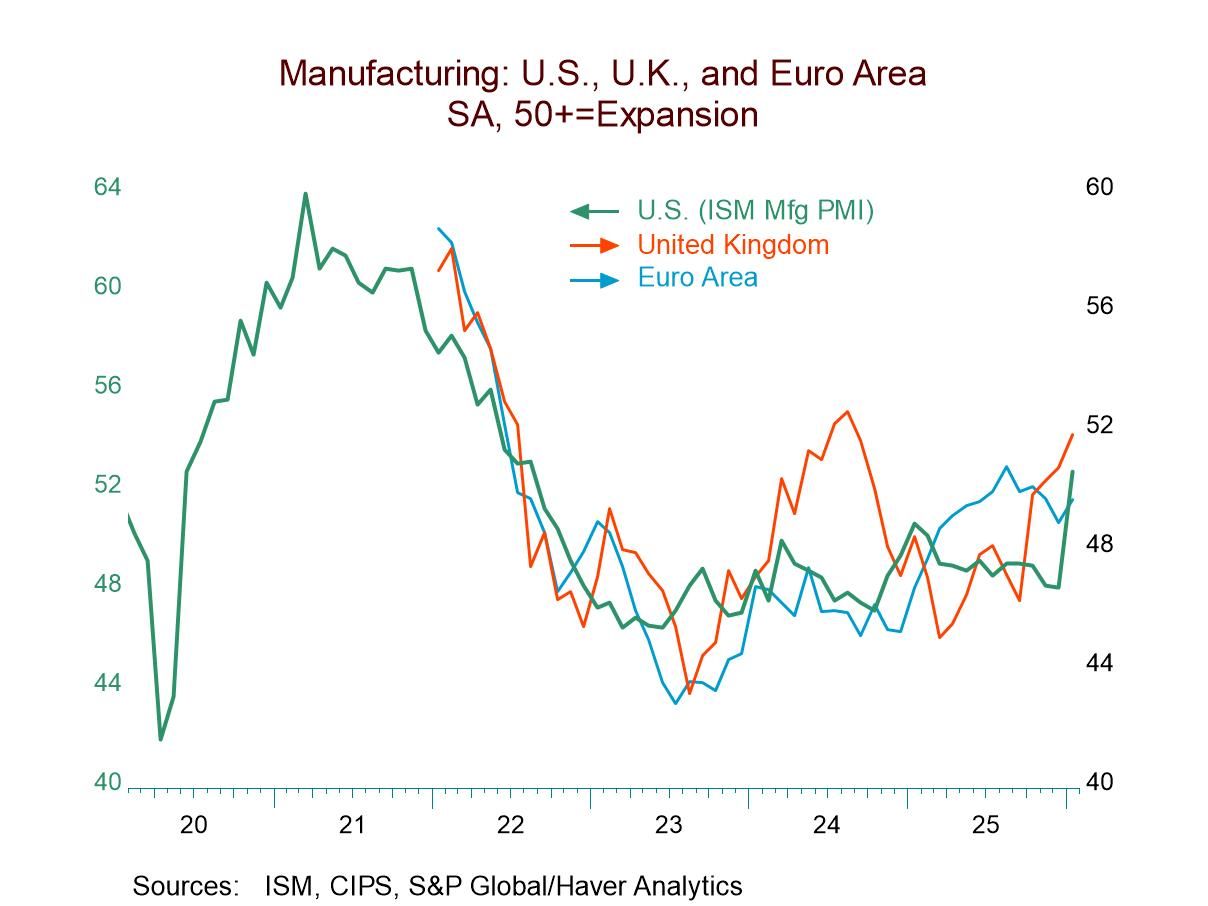

Strong showing in the U.S. a growth leader The breadth of this improvement is quite impressive. The table chronicles the S&P manufacturing PMIs. The chart plots these data for three regions but substitutes the U.S. ISM manufacturing reading freshly released today along-side the S&P readings. The U.S. ISM in January has simply exploded to the upside. That report’s headline snapped up to 52.6 in January from 47.9 in December; it was the strongest reading since the middle of 2022. The order diffusion reading jumped to 57.1, a month-to-month jump of nearly 10 points; the production diffusion rating rose by 5 points monthly; the prices-paid reading continued to snake higher; export and import ratings both rose relatively sharply. If the U.S. is a bellwether for how the rest of the world is going to perform, that bell is ringing loudly in January. The U.S. ISM standing evaluated on data back to 1996 gives an ISM queue standing at its 48.9 percentile – closing in on absolute normal.

Some U.S. detail… The U.S. weakness in imports would probably have something to do with tariffs. There also may be some negative spillovers that would affect exports, but exports would also depend more directly on activity overseas, which the PMI data from S&P suggests has begun to pick up. Employment, which showed an improvement on the month, is still lagging with a 31-percentile standing. However, the rest of the manufacturing readings are really quite solid, quite strong. And in terms of levels instead of rankings, all of the U.S. PMI readings are above their 50% mark in the ISM survey except for inventories and employment. Employment has a 48.1 percentile standing - not a terrible result, especially for a sector whose employment share has been dropping chronically for decades.

Has the worm turned for the US economy? U.S. economy has been through some difficult spots. Economists have focused on various Trump policies and how they've raised the level of uncertainty which is bad for economic activity. However, despite this assessment, the U.S. economy has continued to perform well during this period. And it has been very strong as the end of the year drew to a close. This is even in the face of what became a government shutdown (and, in fact, another, perhaps smaller, shutdown may loom as Democrats seek to bring pressure to bear on ICE through their ability to influence the budget process). Month-to-month all the U.S. manufacturing ISM components strengthened. That included the inflation reading (or prices paid) at a 54-percentile standing, above their median but not an extreme reading. This is a much more brilliant report than had been expected for the U.S., and of course, in the context of much better report on the global economy from the S&P indexes.

Ahead… The Fed seems to want to argue that the effect of tariffs is now mostly water under the bridge. And if that's true, we should also expect the deleterious effect of tariffs on U.S. exports and activity to have reached a peak and to be in a more diminishing mode looking ahead. There are also arguments about how much U.S. productivity is going to stay in place on the contribution of artificial intelligence. And for the moment, those trends both look good, solid, and strong. If the U.S. is going to grow like this, the outlook for global manufacturing is really quite excellent. This is a wonderful surprise for the new year. Hey, it's a new year, baby. Time to drop the pessimism?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief