Global| May 04 2004

Global| May 04 2004FOMC Left Rates Unchanged, Language Altered

by:Tom Moeller

|in:Economy in Brief

Summary

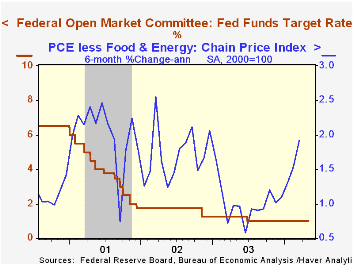

As expected, the Federal Reserve left the target rate for federal funds unchanged at 1.00%. The discount rate also was left unchanged at 2.00%. The decision was unanimous. The press release which accompanied the Fed's action indicated [...]

As expected, the Federal Reserve left the target rate for federal funds unchanged at 1.00%. The discount rate also was left unchanged at 2.00%.

The decision was unanimous.

The press release which accompanied the Fed's action indicated that "output is continuing to expand at a solid rate and hiring appears to have picked up."

Regarding inflation and future policy action the Fed acknowledged that inflation had "moved somewhat higher" and that future "policy accommodation can be removed at a pace that is likely to be measured."

Here is the complete text of the Fed's latest press release.

"How Do Data Revisions Affect the Evaluation and Conduct of Monetary Policy?" from the Federal Reserve Bank of Kansas City can be found here.

Chain Store Sales Jumped Last Weekby Tom Moeller May 4, 2004

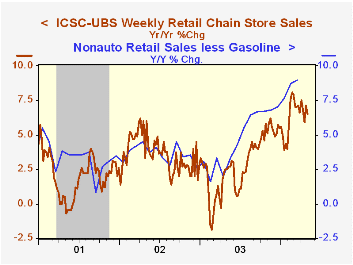

Chain store sales jumped 1.5% higher last week following a 0.5% slip the prior period, according to the International Council of Shopping Centers (ICSC)-UBS survey.

For the full month, sales in April rose 0.4% following a 0.1% dip during March.

During the last ten years there has been a 59% correlation between y/y change in chain store sales and the change in nonauto retail sales less gasoline.

The ICSC-UBS retail chain-store sales index is constructed using the same-store sales reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

| ICSC-UBS (SA, 1977=100) | 05/01/04 | 04/24/04 | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Total Weekly Retail Chain Store Sales | 444.7 | 438.3 | 6.5% | 2.9% | 3.6% | 2.1% |

by Tom Moeller May 4, 2004

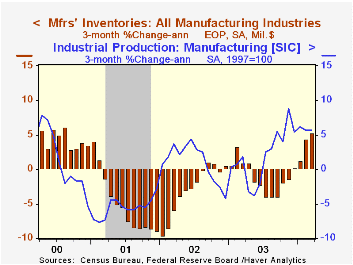

Factory orders surged 4.3% m/m in March, nearly twice the Consensus expectation for a 2.3% rise. The gain was driven by a 5.0% increase in durable goods orders which was revised up from the advance report of a 3.4% rise.

Strength was quite apparent in the capital good sector. The advance report of a 2.1% rise in nondefense capital goods orders was revised and doubled. Excluding aircraft & parts the rise in advance orders was nearly doubled to 4.5% (12.4% y/y). Much of the upward revision stemmed from orders for computers & electronic products which were revised to show a 2.5% (16.3% y/y) gain versus the advance report of a 0.2% uptick.

Non-durable goods orders (which equal shipments) jumped 3.5% (6.2% y/y) and recouped a 1.8% February decline. Higher petroleum shipments led the March gain but shipments of apparel, paper and chemicals also were quite strong.

Factory inventories rose 0.3% in March and the February increase was revised up. The swing to inventory accumulation from decumulation has been scattered across industries, although the furniture and automobile industries still lag.

Factory shipments jumped 3.8%. Excluding the transportation sector shipments rose 4.2% (9.1% y/y).

| Factory Survey (NAICS) | Mar | Feb | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Inventories | 0.3% | 0.6% | -0.2% | -1.3% | -1.8% | -6.1% |

| New Orders | 4.3% | 1.1% | 7.0% | 3.7% | -1.9% | -6.7% |

| Shipments | 3.8% | -0.1% | 9.2% | 2.6% | -2.0% | -5.4% |

| Unfilled Orders | 1.2% | 0.9% | 5.0% | 4.2% | -6.1% | -5.9% |

by Tom Moeller May 4, 2004

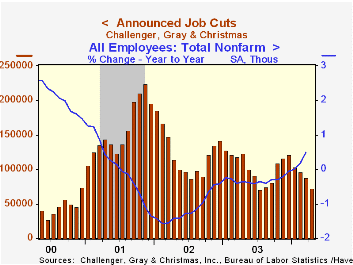

Challenger, Gray & Christmas reported that announced job cuts rose 6.1% to 72,184 in April following m/m declines of 11.9% and 34.3% during the prior two periods.

The three month moving average of job cut announcements fell to 72,489 (-41.2% y/y). During the last ten years there has been an 83% (inverse) correlation between the three month average level of announced job cuts and the y/y percent change payroll employment.

The m/m increase in layoffs was scattered across industries but notable in the automotive, computer & chemical industries.

Job cut announcements differ from layoffs. Many are achieved through attrition, early retirement or just never occur.

| Challenger, Gray & Christmas | April | March | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Announced Job Cuts | 72,184 | 68,034 | -50.7% | 1,236,426 | 1,431,052 | 1,956,876 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief