Asia| Jan 26 2026

Asia| Jan 26 2026Economic Letter from Asia: Forecasts, Chips, and Polls

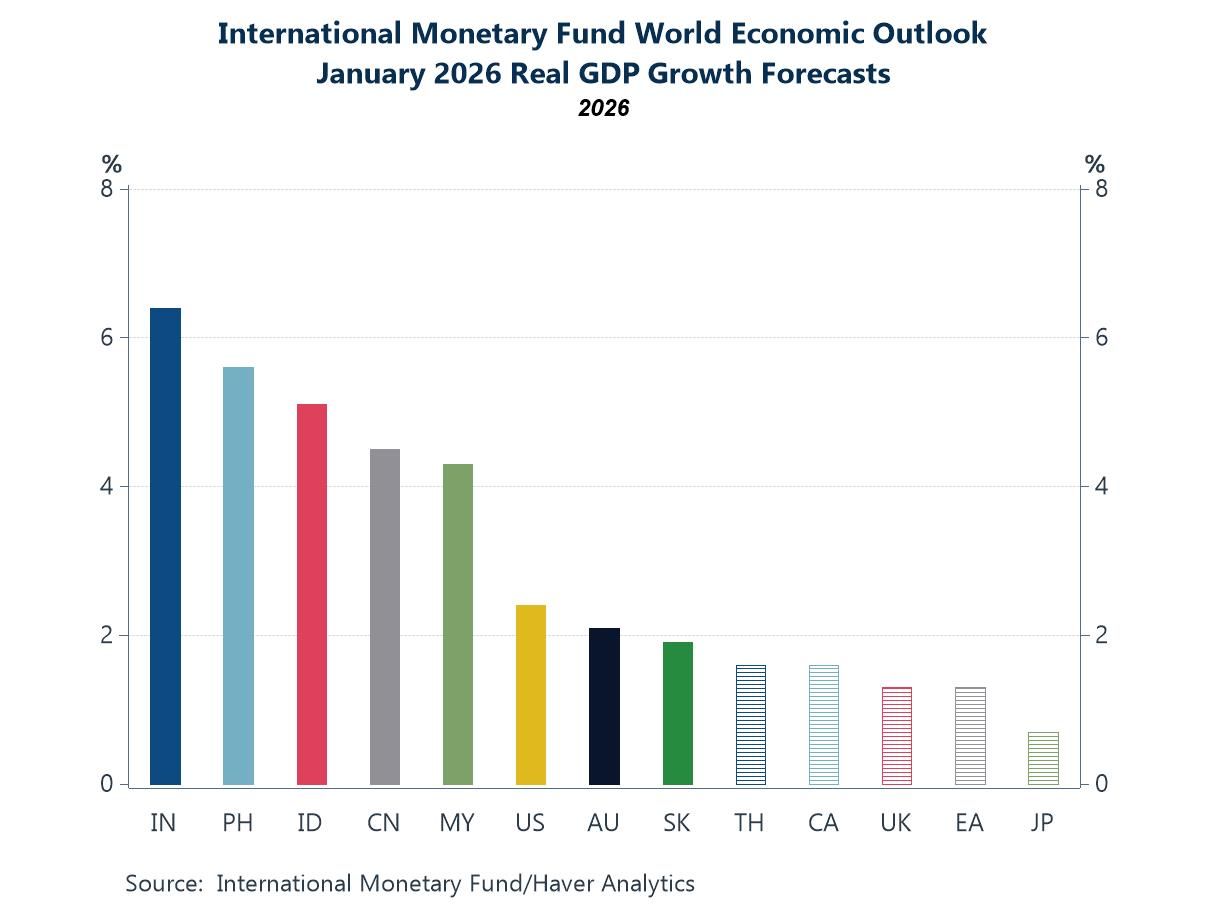

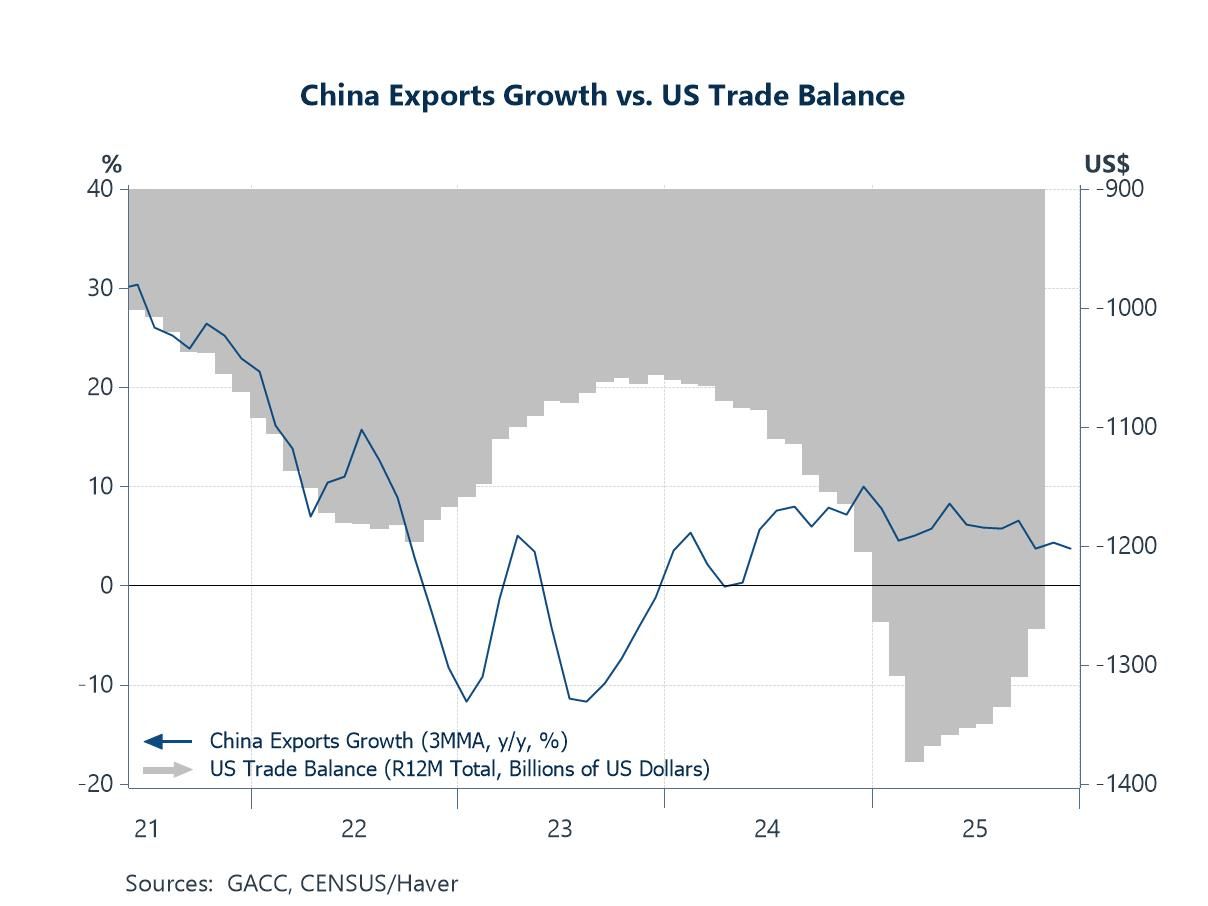

This week, we take stock of key developments across Asia. The IMF’s latest outlook delivered several positive growth revisions, with India once again seen at the forefront of regional expansion, while China is still seen unlikely to reach a 5% growth target this year should it be adopted (chart 1). Between China and the US, a clear divergence in trade strategies persists. China has continued to pivot toward Asia to sustain relatively robust export growth, while the US has turned inward—effectively narrowing its trade deficit in line with President Trump’s objectives (chart 2). Within Asia, trade ties with China have become increasingly two-way, as China’s share as an export destination has risen steadily over the past decades to rival that of the US for many economies (chart 3).

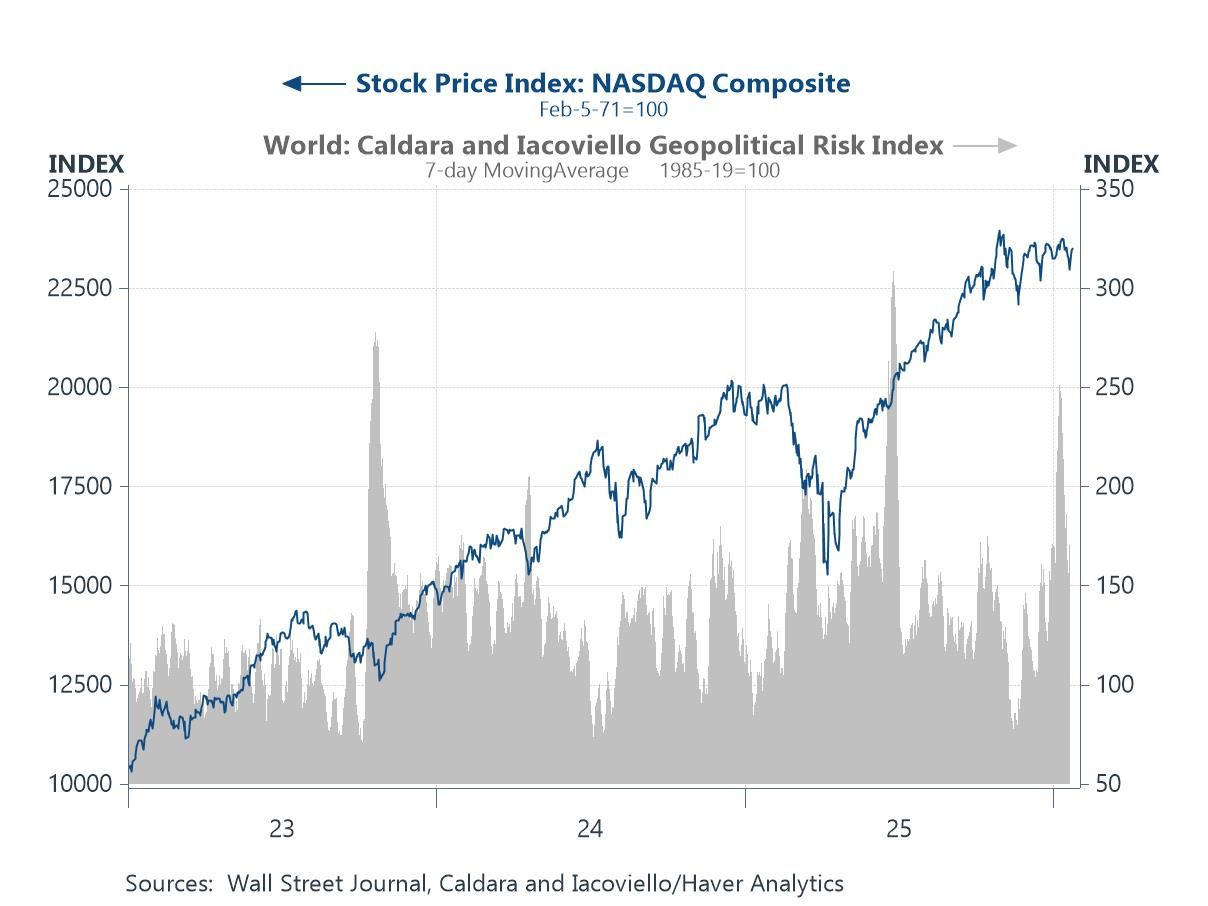

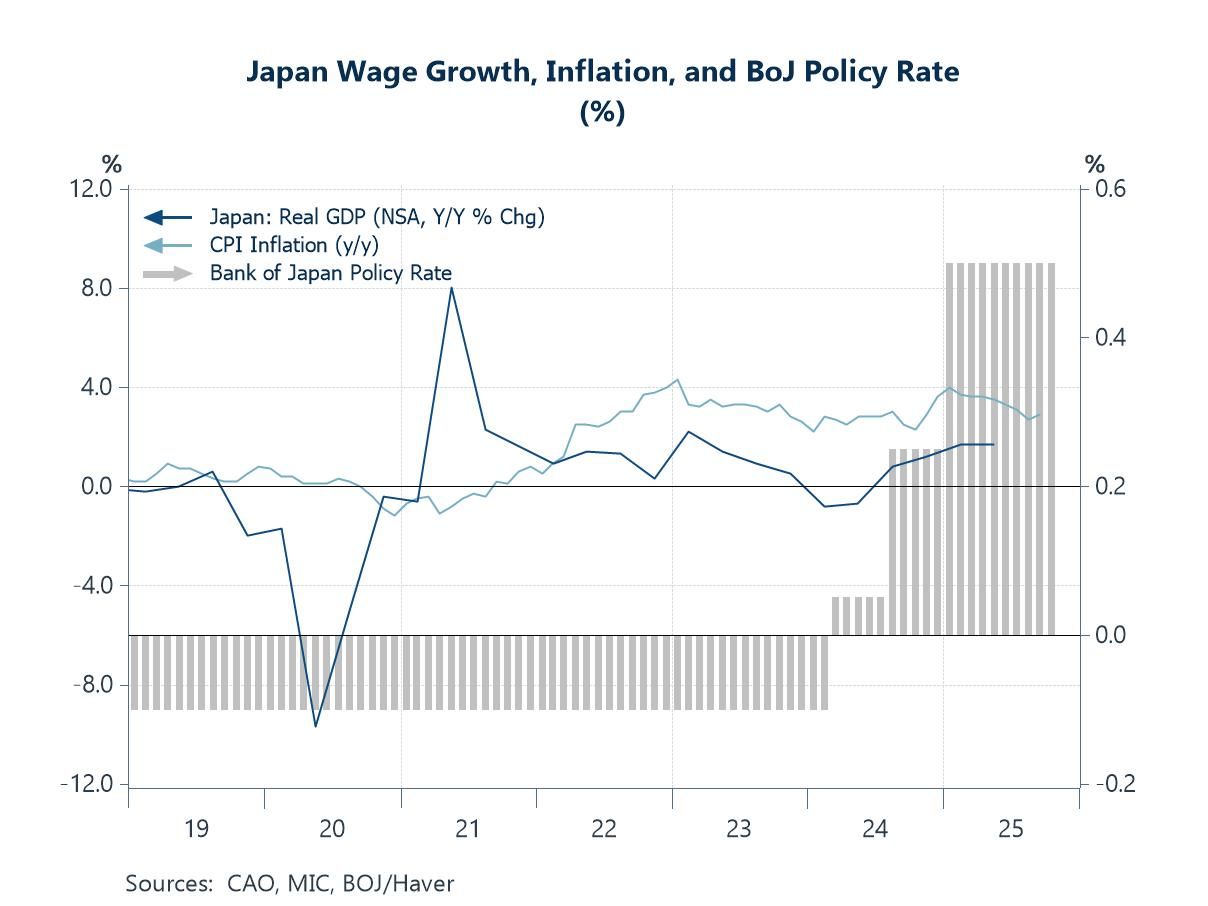

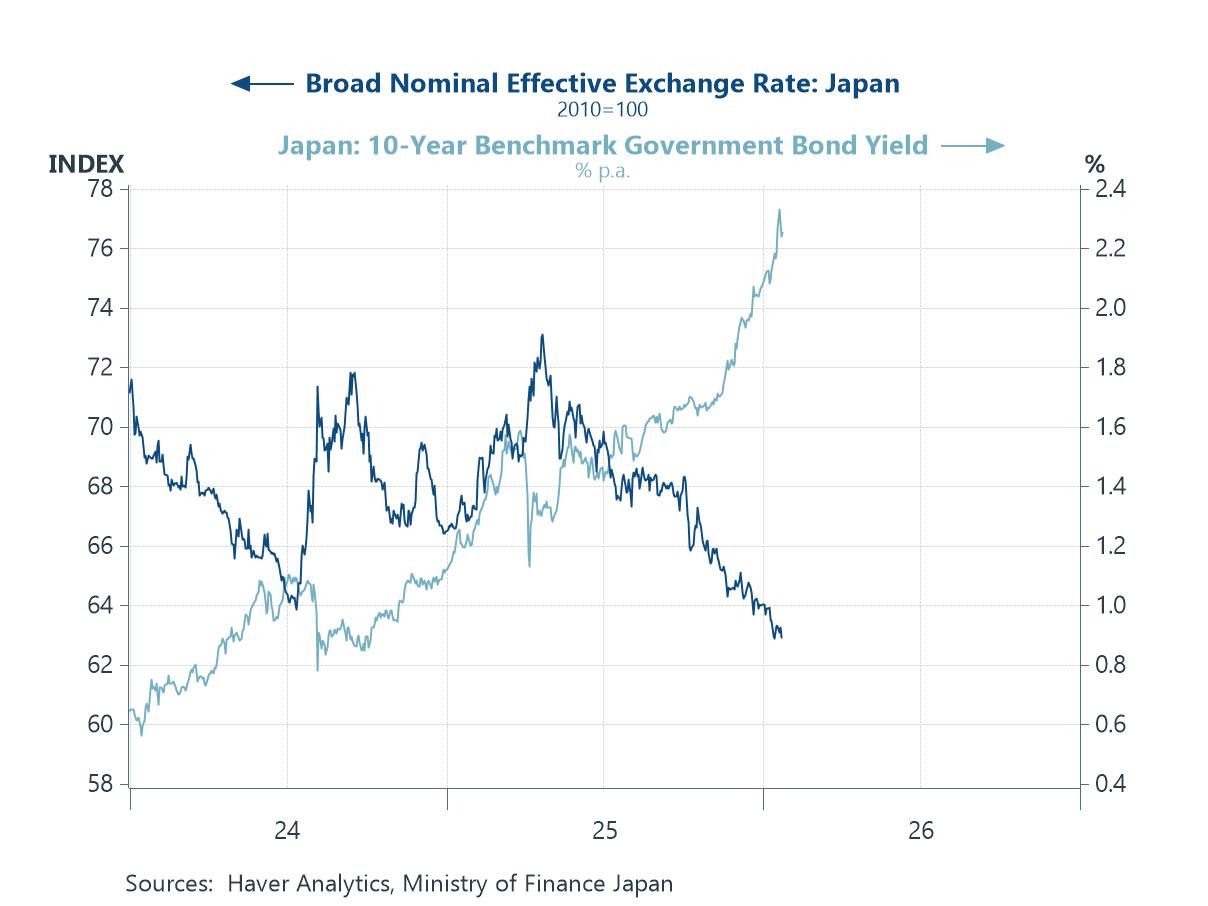

In the AI space, notable developments emerged following reports that Chinese authorities may soon formally allow domestic tech firms to import Nvidia’s H200 chips. The news could provide a boost to US tech equities, although broader geopolitical risks remain a possible resurgent drag on sentiment (chart 4). Turning to Japan, last week’s Bank of Japan (BoJ) meeting left policy rates unchanged, as expected. However, the BoJ’s latest outlook report delivered upgrades to both growth and inflation forecasts—developments that could pave the way for further monetary tightening (chart 5), albeit likely only after near-term uncertainties, most notably upcoming snap elections, have passed. Ahead of the polls, the yen and Japanese government bonds have come under sustained pressure (chart 6), though short sellers may become more cautious given the risk of official intervention.

The IMF’s World Economic Outlook The International Monetary Fund (IMF) unveiled its updated forecasts last week in its World Economic Outlook (WEO) publication. On growth, World GDP growth for 2026 was revised up by 0.2 ppts to 3.3%, driven by a surge in technology investment, including AI. China and India each saw a 0.3 ppt upgrade to their growth forecasts, while Japan and South Korea received more modest 0.1 ppt upgrades. Within Asia, India continues to be seen as the region’s growth leader (chart 1). By contrast, despite the IMF upgrade, China is still not expected to reach 5% growth this year should it re-adopt such a target, though there has been some discussion of a lower target range of 4.5–5%. On the downside, only a handful of economies saw downgrades; in Asia, the Philippines stands out with a 0.1 ppt downward revision to 5.6% for the year.

Chart 1: IMF January 2026 World Economic Outlook

China, the US, and trade Turning to China, and to recap, the economy managed to eke out exactly 5% growth in 2025, supported by exports amid a challenging domestic backdrop. Whether this pace can be sustained this year, however, remains uncertain. Externally, China has nonetheless maintained relatively robust export growth despite tariffs, largely by redirecting exports toward other trading partners, particularly within Asia. On the other side, the US—through its pursuit of “America First” policies such as tariffs—has seen its trade deficit significantly reduced over the past year (chart 2), effectively achieving one of President Trump’s stated objectives. That said, both approaches carry risks: China may face heightened scrutiny over excess capacity, while the US risks further alienating long-standing trade partners.

Chart 2: China exports growth and US trade balance

More on China: the relationship with Asia has become increasingly two-way. China has not only pivoted its exports toward regional partners but has also become a growing export destination for Asian economies. For many major economies in the region, China now accounts for at least 10% of exports, reaching as high as 25% in cases such as Indonesia. In contrast, the US share of exports has declined across several Asian economies. Japan and the Philippines, for example, each had around 30% of exports heading to the US in the early 2000s; today, that share has fallen to roughly 15–20%. As a result, China now rivals the US as an export destination for many economies as inward-looking “America First” policies take hold (chart 3). Importantly, China’s rise as a key export destination has been gradual, unfolding over decades from shares that were previously largely below 5%.

Chart 3: Share of China and the US as export destinations

China and chips There have also been notable developments in the chips space after reports that China may soon allow its tech firms to purchase Nvidia’s H200 AI chips. The news could boost sentiment in US tech equities, although geopolitical risks remain elevated and details are still scarce (chart 4). Still, authorities appear keen to support the domestic chip industry: companies are reportedly being encouraged to buy a set number of domestic chips as a condition for approval to import H200s. The H200 is an older generation of Nvidia chips that the US previously approved for export, albeit with a 25% tariff on units destined for China. Importantly, the latest reports run counter to earlier concerns that H200 shipments had been effectively banned, after Chinese customs reportedly stopped some shipments.

Chart 4: US tech equities and world geopolitical risk

The Bank of Japan Moving to Japan, the Bank of Japan (BoJ) released its first interest rate decision of the year last week and, as expected, kept its policy rate unchanged at 0.75% (chart 5). The meeting nonetheless offered notable takeaways. The BoJ’s latest outlook report included modest upgrades to real GDP forecasts for fiscal years 2025 and 2026. It also revised up core CPI forecasts, likely reflecting expectations of both already passed and maybe even anticipated additional fiscal support under new Prime Minister Takaichi. The twin upgrades suggest the path to further monetary tightening may be clearer over the coming quarters, once interim uncertainties ease. That said, Japan still faces several near-term risks, including upcoming elections, which we discuss in the next section.

Chart 5: Japan’s economy and its policy rate

Japan’s snap elections Previous rumours that Prime Minister Takaichi might call snap elections in early February materialised last Friday, when the Lower House was dissolved to make way for polls on February 8. While the move may capitalise on her strong approval ratings, it remains a political gamble and introduces an interim period of political flux and policy uncertainty. In the lead-up to and following the announcement, the yen weakened significantly and Japanese yields surged, prompting authorities to publicly warn against excessive volatility. Yen short sellers have also become more cautious, given the risk that further sharp moves could trigger market intervention. External factors have since helped the yen recover somewhat: renewed US government shutdown fears have weighed on the US dollar, supporting the yen in recent days (chart 6).

Chart 6: The Japanese yen and yields

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief