Global| Jan 23 2026

Global| Jan 23 2026S&P Flash PMIs Rebound But Emit No Clear Signal

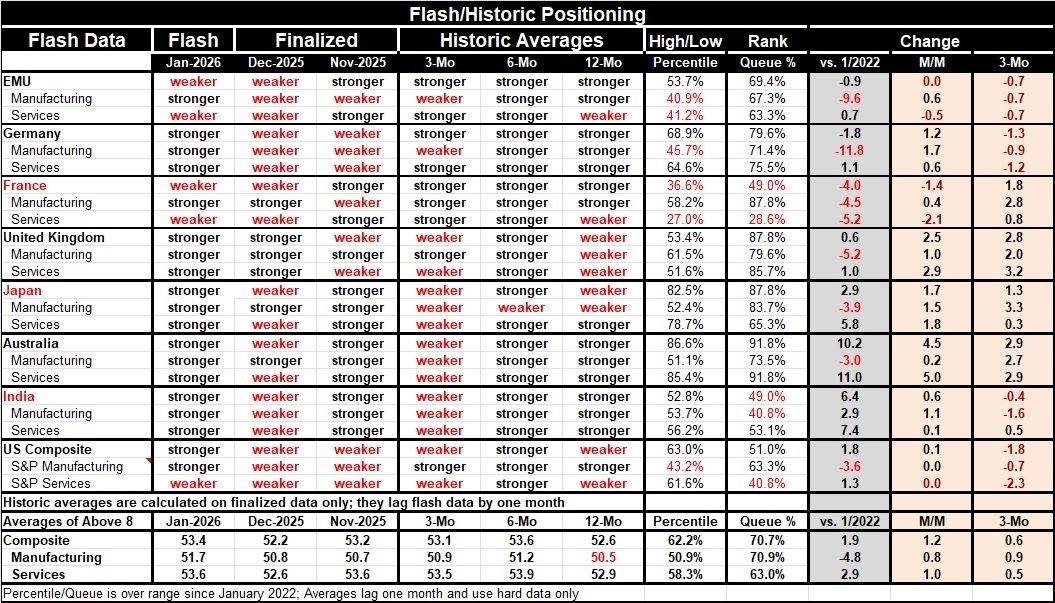

The S&P PMIs for January show flash readings that indicate broadly stronger conditions across the early reporters in this table. Exceptions are the European Monetary Union as a whole with its composite reading weaker and France with its composite reading weaker, but Germany, the United Kingdom, Japan, Australia, India, and the United States all have composite readings that are stronger month-to-month in January. With these eight countries, there are 24 readings in each period, three for each country: a composite, one for manufacturing, and one for services. Among these 24 readings, only five of them were weaker month-to-month in January. Of course, this follows a December when only 6 of the readings were stronger month-to-month.

The sequential readings, that we calculate only off hard data (which means that calculations are done from December backward) are still mixed. Substantially weaker conditions period-to-period are reported comparing three-months to six-months. Over three months, only nine of the 24 readings are stronger whereas over six months only one of the 24 readings is weaker when compared to the 12-month average. Over 12 months, the average is stronger than it was one-year ago in 15 of the 24 readings.

Only the United States and France have service sectors that are below their medians over this period back to 2022. Only France and India have composite readings that are below their respective medians over this period. But by comparison, there are very strong composite readings as well. There is a 91-percentile standing on the composite in Australia, an 87-percentile standing in Japan and the United Kingdom. The German composite has a 79-percentile standing.

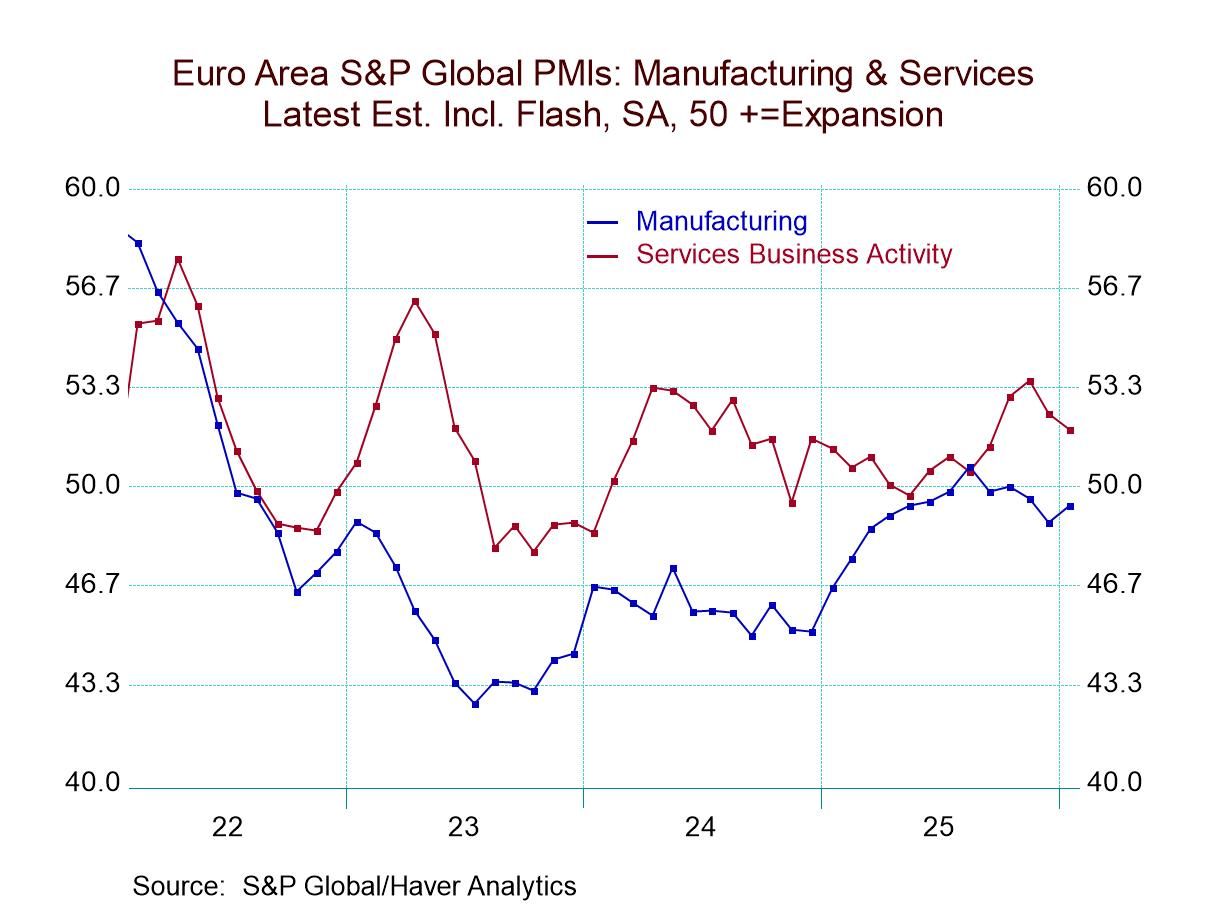

The recent data have been running sporadically hot and cold, making it difficult to make sense out of what's happening. But broadly, it's clear that the PMIs in the European Monetary Union have been working their way higher and this is the general theme.

For the 8 reporters in the table back to January 2022, all of them except India show weaker manufacturing readings in January 2026 than what they showed in January 2022. But January 2022 was, of course, part of the COVID recovery move. Manufacturing in the European Monetary Union slipped from its high point over this period to its low point around mid-2023.

Looking at point-to-point changes over the last three months, we find 3-sector cumulative drops in the United States, the European Monetary Union, and Germany. India has two sectors weakening with a decline in its composite as well as its manufacturing reading. Meanwhile, all the rest of the readings in the table over these three months show improved results. On a broad basis, we have to conclude there's more strength than weakness. However, since the weakness is concentrated and widespread and the largest economic units: the United States, the European Monetary Union, and the German economy, it's better to refer to the last three months as generating mixed economic statistics.

Looking forward, conditions are still hard to sort out. There's this obvious recovery in January after an equally obvious weak spot in December. The two of them cancel one another out in some sense. The average composite reading for all countries in the table shows some improvement in the manufacturing sector but waffling on the services sector. We get the same sort of readings looking at sequential averages; they do more of waffling than any kind of clear trend. On balance, the S&P readings don't give us a lot to go on this month. The survey is a bounce-back after a weak December and that's good news. But that doesn't give us a good handle on the trend yet.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief