Global| Jan 22 2026

Global| Jan 22 2026Charts of the Week: Seeing Green

by:Andrew Cates

|in:Economy in Brief

Summary

This week’s data and market moves have been framed by an abrupt escalation in geopolitical tensions surrounding Greenland, which has served as a catalyst for broader financial unease rather than a standalone shock. The episode has sharpened investor focus on US policy predictability, amplifying concerns already evident in the charts on EU–US trade exposure, where tariff threats risk feeding directly into confidence effects and capital flows. At the same time, recent turbulence in Japanese government bonds appears to have been an underappreciated driver of the sell-off in US Treasuries, highlighting how global capital reallocation—rather than geopolitics alone—has contributed to higher US yields. These forces intersect with growing questions around the durability of US monetary credibility, as inflation expectations have shown signs of decoupling from traditional oil-price anchors, raising the sensitivity of markets to any perceived constraints on the Federal Reserve. Beyond the US, UK data delivered a modest upside surprise in headline inflation, with persistent services and wage pressures reinforcing a cautious policy backdrop for the Bank of England. In China, meanwhile, Q4 GDP growth of 4.5% y/y kept full-year expansion aligned with the government’s target, but continued weakness in the property sector remains a significant drag on investment and household confidence. Taken together, the week’s developments point to a global outlook increasingly shaped by geopolitical risk, capital-flow dynamics and domestic structural constraints, rather than by straightforward cyclical momentum alone.

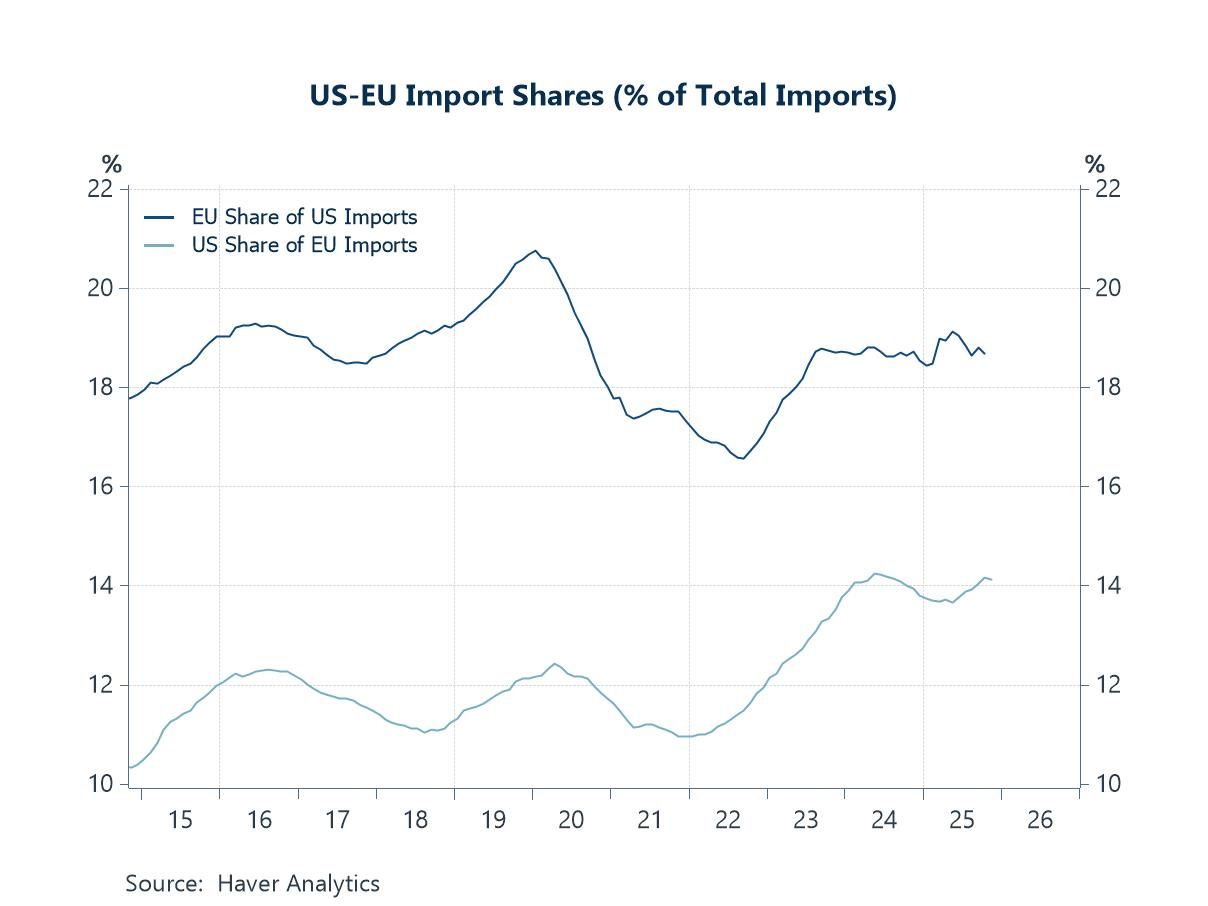

US trade with Europe Geopolitical tensions surrounding Greenland have abruptly sharpened investor sensitivity to US trade and foreign-policy risk. What might once have been dismissed as rhetorical brinkmanship has taken on greater macro-financial relevance as Donald Trump has coupled renewed interest in Greenland’s strategic importance with explicit threats of higher tariffs on European imports. The first chart below highlights that the US is materially more exposed to EU goods than the EU is to US trade, making any escalation asymmetrically more costly for the US economy. Beyond the direct inflationary impact of higher tariffs, the more immediate risk lies in confidence effects and capital flows: early signs of capital reallocation away from US assets over the past 24 hours suggest that markets could be beginning to price a broader erosion of policy predictability. In this environment, tariffs risk functioning less as a targeted trade tool and more as a systemic confidence shock—tightening financial conditions, unsettling the dollar’s safe-haven status and increasing downside risks to US growth via weaker investment and higher risk premia.

Chart 1: US-EU import shares

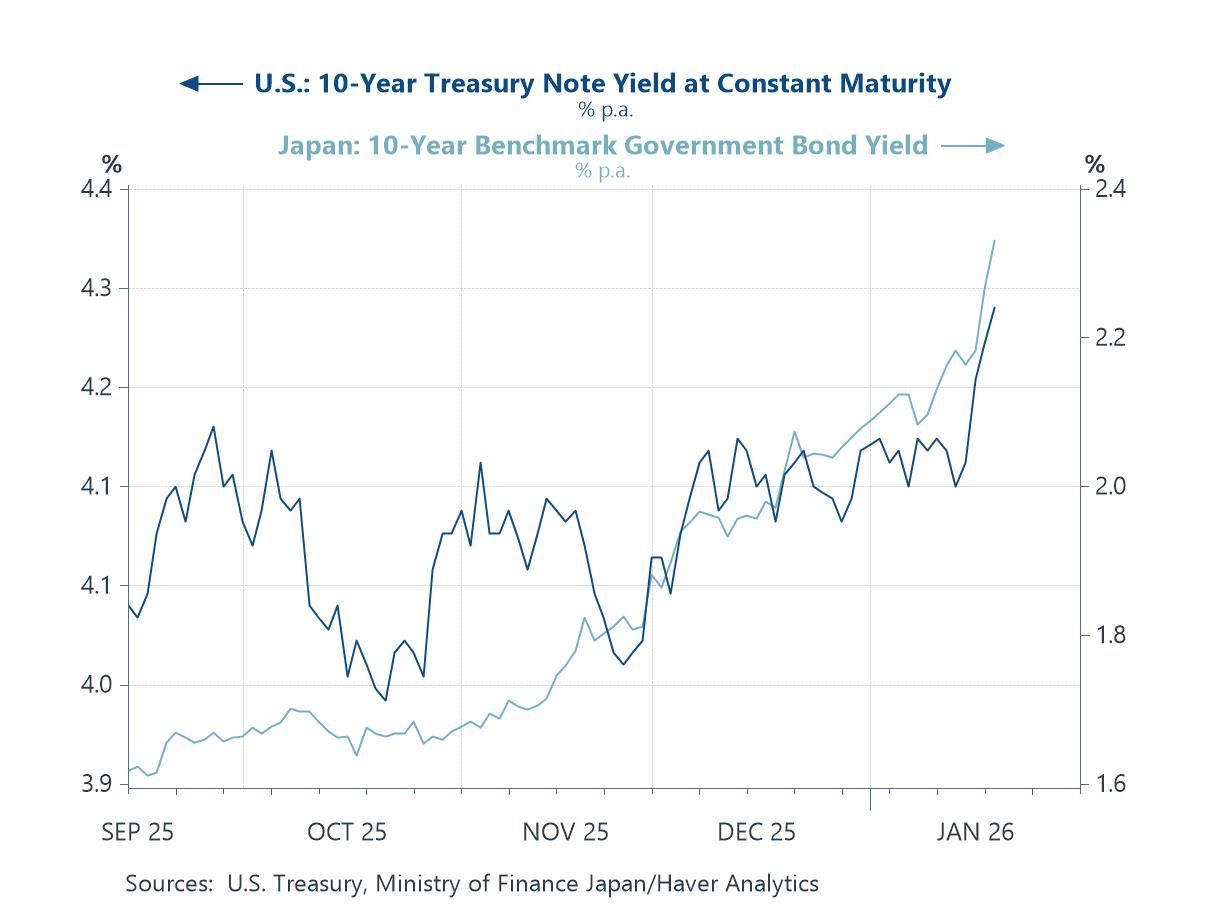

Japan’s JGB yields That said, recent capital outflows from US assets may owe as much to developments in Japan as to geopolitical and trade-related shocks. While tariff threats and policy unpredictability have clearly unsettled sentiment, an underappreciated driver of the sell-off in US Treasuries has been the sharp repricing in the Japanese government bond market. Renewed domestic political uncertainty and intensifying concerns over Japan’s debt dynamics have triggered a rapid rise in JGB yields, prompting portfolio rebalancing by Japanese investors and reducing the relative appeal of US duration. Given Japan’s role as one of the largest foreign holders of US Treasuries, yield gyrations at home can translate quickly into capital repatriation, hedging adjustments and reduced demand for US bonds. In this sense, recent moves in US yields may reflect less a direct reaction to geopolitical risk and more a globally transmitted capital-flow shock—originating in Japan but felt most acutely in US financial markets.

Chart 2: 10-year government bond yields in the US and Japan

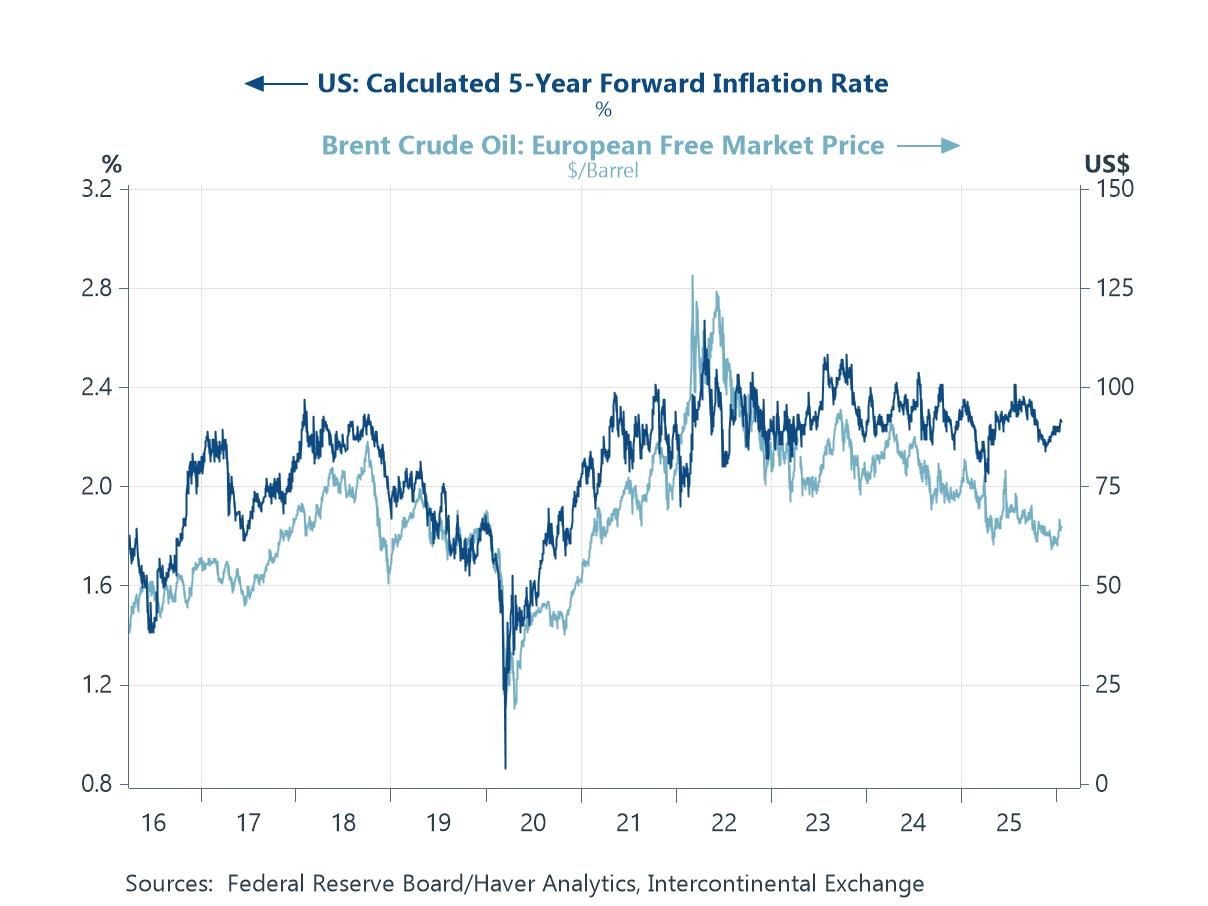

Inflation expectations and oil prices Capital-flow dynamics may have also begun to spill over into how markets are pricing US inflation risk and monetary credibility. Historically, medium-term US inflation expectations have remained closely anchored to global energy prices, as illustrated by the strong co-movement between the 5-year forward inflation rate and Brent crude prices. More recently, however, that relationship has begun to fray: inflation expectations have proven notably resilient even as oil prices have softened, suggesting that markets are increasingly pricing political and policy risk rather than cost-push fundamentals alone. Renewed tariff threats under President Trump, combined with heightened geopolitical tensions involving Greenland and transatlantic relations, risk reinforcing concerns that future inflation outcomes could be shaped as much by political intervention as by macroeconomic conditions. Any perception that the Federal Reserve may face constraints on its operational independence would compound this shift—loosening inflation anchors, raising term premia and increasing the sensitivity of capital flows to US policy credibility.

Chart 3: US market-based 5-year ahead inflation expectations versus oil prices

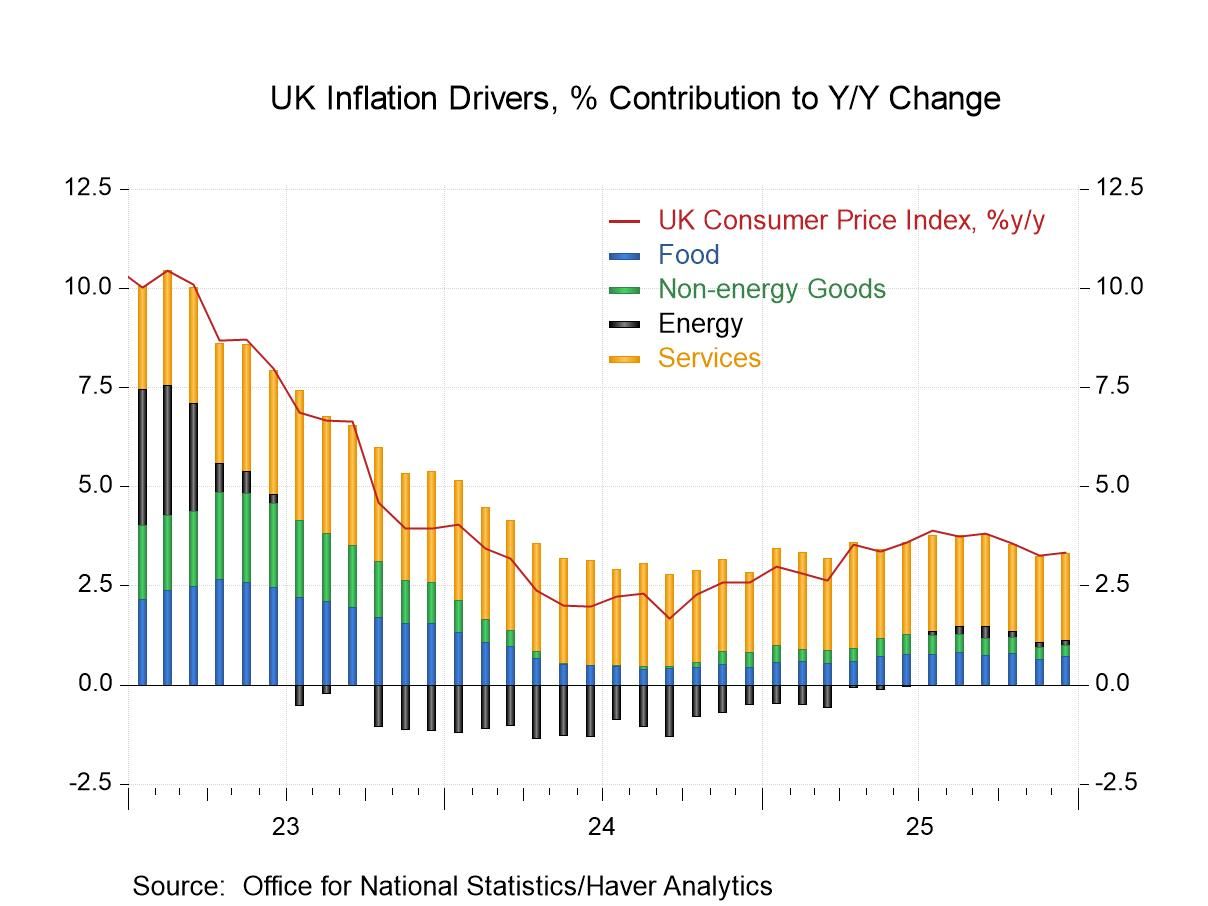

UK inflation UK inflation data released this week show a small upside surprise in headline CPI at year-end. Headline CPI inflation specifically rose from 3.2% y/y in November to 3.4% in December, a little more than expected. The chart below shows that the pickup was driven by persistent underlying pressures—most notably in services. While a negative drag from energy prices has largely faded, services inflation continues to account for a disproportionate share of overall price growth, probably reflecting ongoing wage pressures and limited slack in parts of the domestic economy.

Chart 4: UK inflation drivers

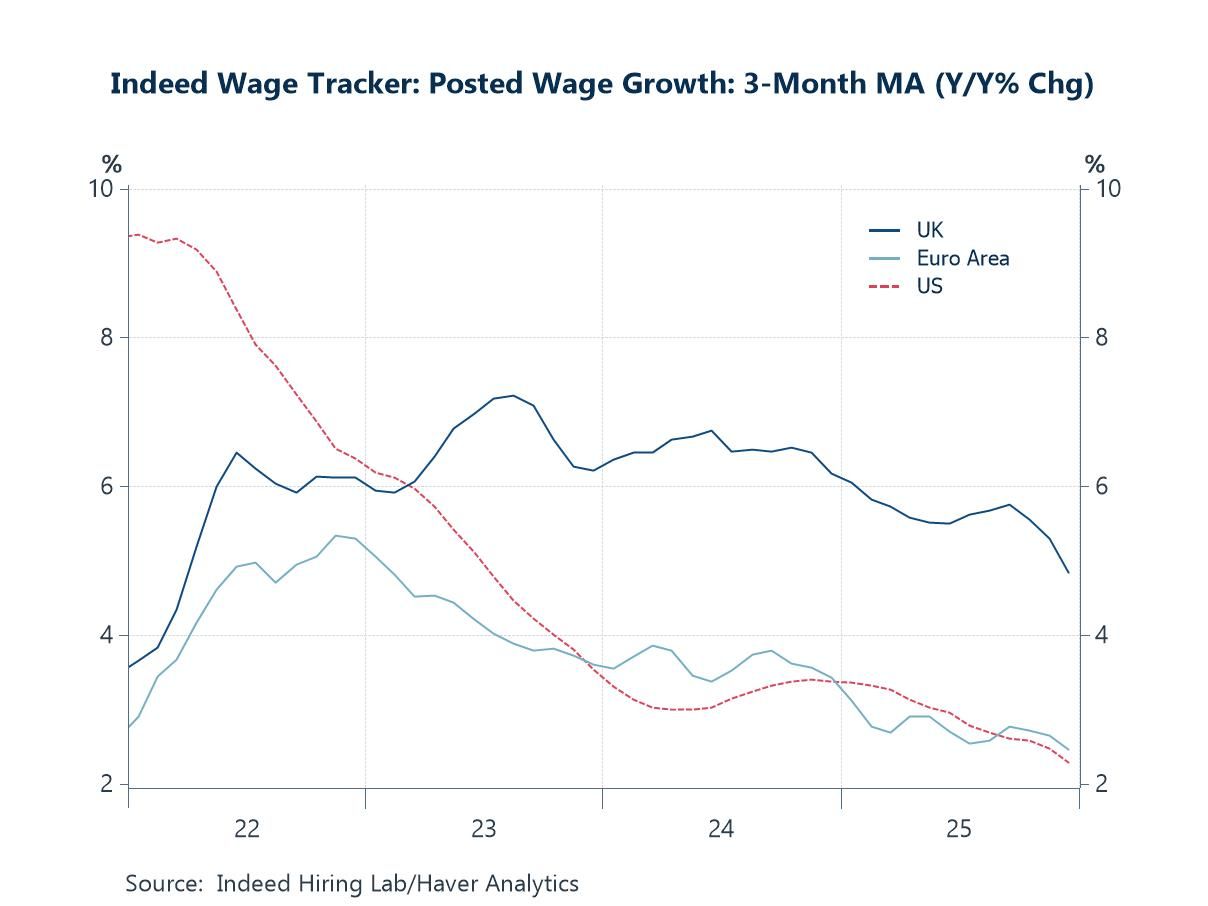

Wage growth in the US and Europe Labour-market data from the Indeed Hiring Lab reinforce the picture of persistent services-side pressure in the UK inflation mix. As the chart shows, UK posted wage growth remains elevated relative to both the euro area and the US, even though momentum has eased from its 2023 peak. At around the mid-5% range on a three-month moving average basis, UK wage growth is still running at a pace that is difficult to reconcile with a rapid return of services inflation to target. By contrast, posted wage growth in the euro area has slowed more decisively, while the US has seen a sharper deceleration from earlier extremes.

Chart 5: Indeed Wage Tracker: Posted wage growth in the US, euro area and the UK

China’s property market Finally, the Q4 GDP figures released in China this week sit uneasily alongside continued weakness in its domestic property sector, which remains a key drag on both investment and consumption. While Q4 growth of 4.5% y/y brought full-year GDP broadly in line with the authorities’ 5% target, the chart highlights how property-market adjustment is still running deep beneath the surface. Prices of existing homes across China’s 70 cities remain in year-on-year decline, while real estate investment continues to contract sharply, underscoring the scale and persistence of the sector’s retrenchment. This helps explain why fixed asset investment has softened further and why household demand remains subdued, despite more resilient industrial output.

Chart 6: China’s house price inflation versus residential investment growth

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief