Global| Jun 24 2003

Global| Jun 24 2003Consumer Confidence About Flat

by:Tom Moeller

|in:Economy in Brief

Summary

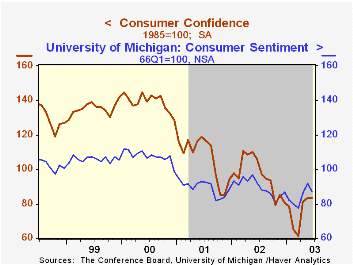

The Conference Boards Index of Consumer Confidence was about flat in June. The index fell 0.1% m/m to 83.5. Consensus expectations were for a decline to 82.5. Since the low of this past March, Confidence has risen 36.0%. That rise is [...]

The Conference Board’s Index of Consumer Confidence was about flat in June. The index fell 0.1% m/m to 83.5. Consensus expectations were for a decline to 82.5.

Since the low of this past March, Confidence has risen 36.0%. That rise is versus a 12.4% gain in the University of Michigan's Consumer Sentiment during the same period.

The slip in confidence in June reflected a 3.6% decline in the present situation index, down for the second consecutive month. The index of expectations rose 1.5% for the third monthly gain this year.

Jobs were viewed as hard to get by 32.0% of survey respondents, down slightly from the record 32.9% in May. Expectations for employment opportunities in six months improved to the highest level in twelve months.

During the last five years there has been a 75% correlation between the level of Consumer Confidence and the y/y change in real consumer spending.

The Conference Board's survey is conducted by a mailed questionnaire to 5,000 households and about 3,500 typically respond.

| Conference Board | June | May | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Consumer Confidence | 83.5 | 83.6 | -21.4% | 96.6 | 106.6 | 139.0 |

by Tom Moeller June 24, 2003

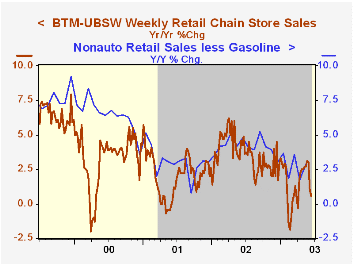

Chain store sales added 0.6% last week to the 0.3% gain of the week prior according to the BTM-UBSW survey.

Sales so far in June are 0.1% above the May average.

During the last five years there has been a 59% correlation between the year-to-year percent change in chain store sales and the change in nonauto retail sales less gasoline.

The BTM leading indicator of chain store sales rose 0.4% in the second week of June and continued the improving trend begun in early May.

The BTM-UBSW retail chain-store sales index is constructed from the sales results reported by seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

| BTM-UBSW (SA, 1977=100) | 6/21/03 | 6/14/03 | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Total Weekly Retail Chain Store Sales | 419.4 | 417.0 | 0.6% | 3.6% | 2.1% | 3.4% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief