Revised Q4 GDP: Downward Adjustment Leaves Modest Growth

Summary

- Consumer spending and business investment in structures accounted for most of the adjustment.

- Although growth was slow, the results were not alarming.

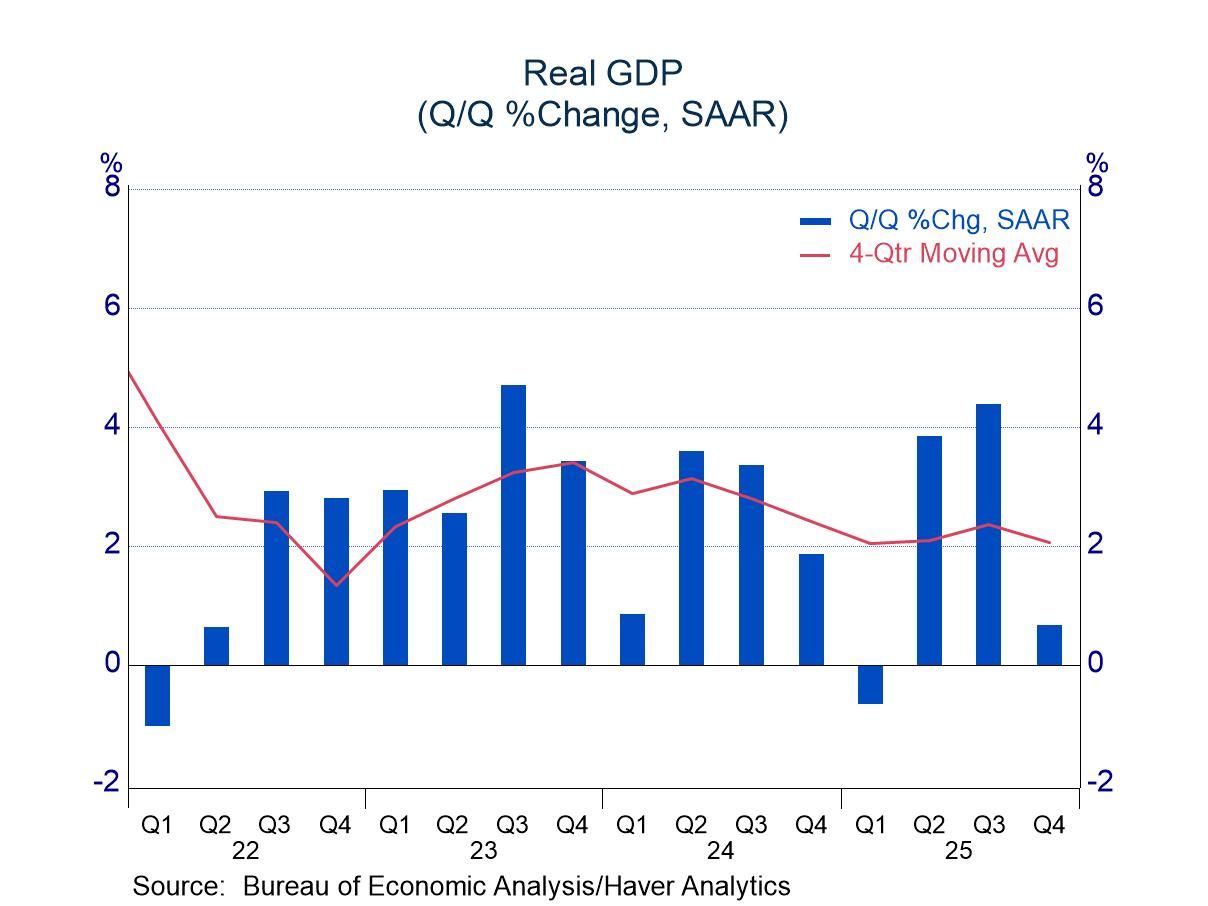

New figures show that real GDP grew 0.7% in the fourth quarter of 2025, revised down from the initial estimate of 1.4%. The pace was among the slowest of the past few years, but the result was not especially troubling, as the government shutdown acted as a notable constraint on economic growth. Federal spending fell 16.7% in Q4, which subtracted 1.2 percentage points from the advance in GDP.

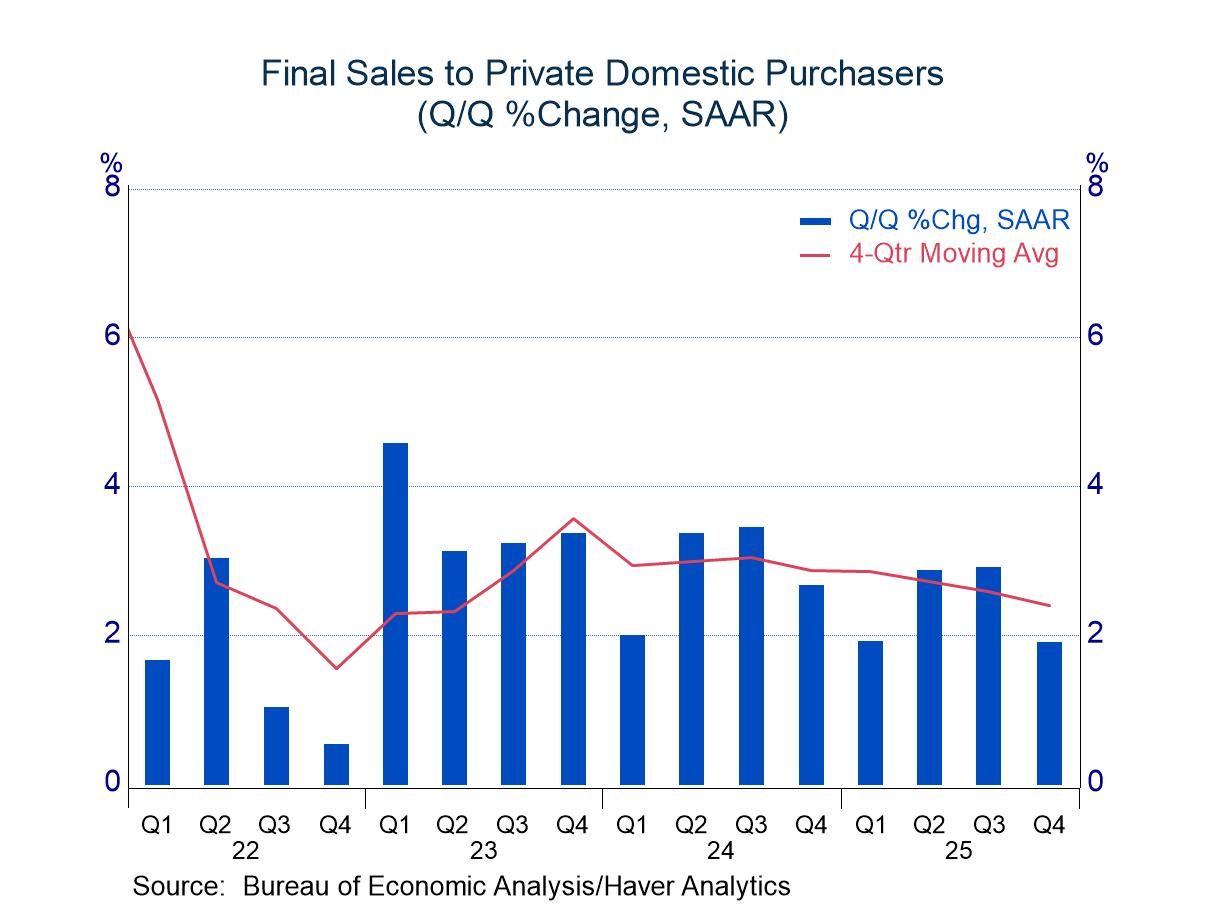

Other sectors performed reasonably well, as shown by an increase of 1.9% in final sales to private domestic purchasers, a pace close to the economy’s potential. (In addition to government spending, final sales to private domestic purchasers excludes the influence of net exports and inventory investment. It is sometimes called private domestic final demand – PDFD.)

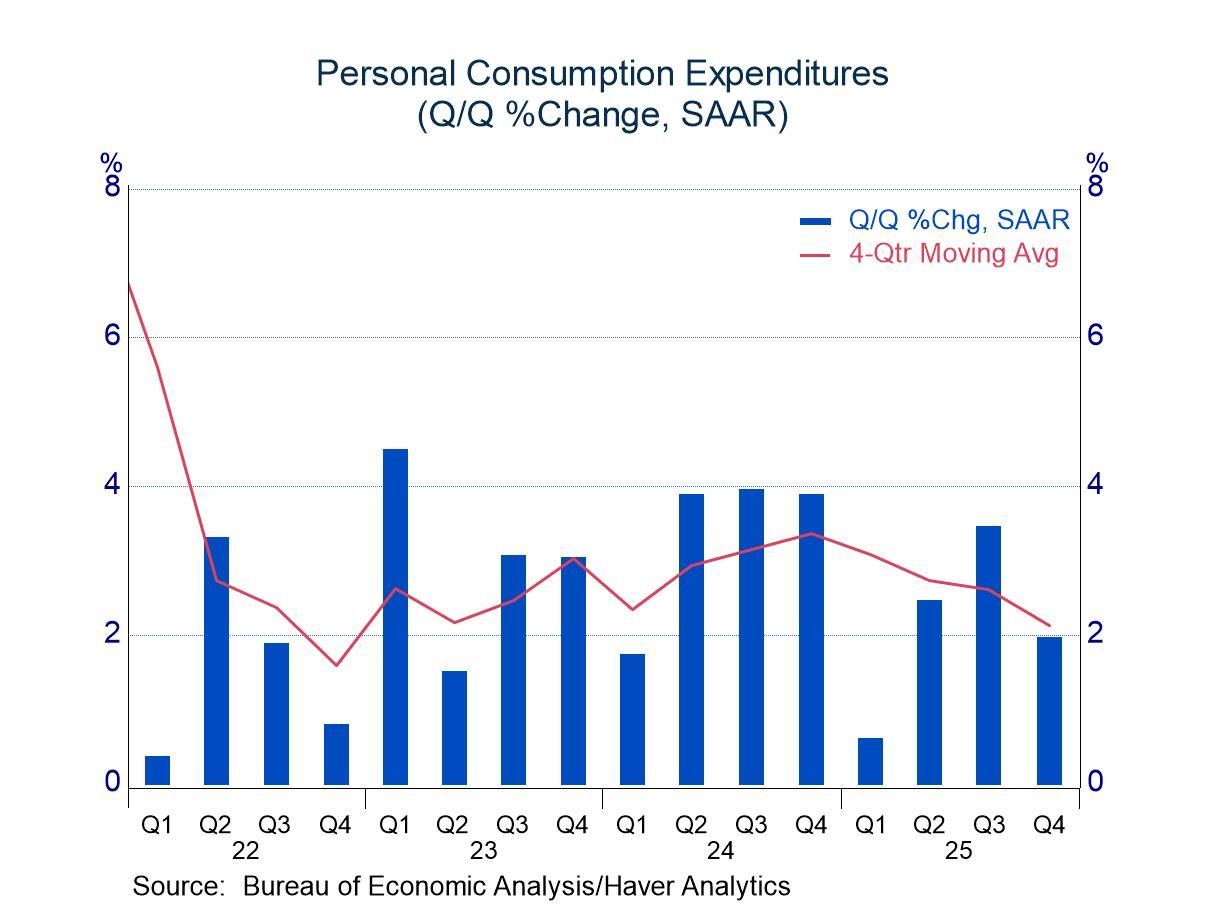

Although the pace of PDFD was respectable, it was the source of most of the downward revision to GDP growth, with the new figure one-half percentage point off the initial estimate of 2.4%. Consumer spending made the largest contribution to the downward revision with growth slowing from 2.4% to a still-respectable 2.0%. Most of the adjustment occurred in the service area, but spending on services remained firm with growth of 2.7%.

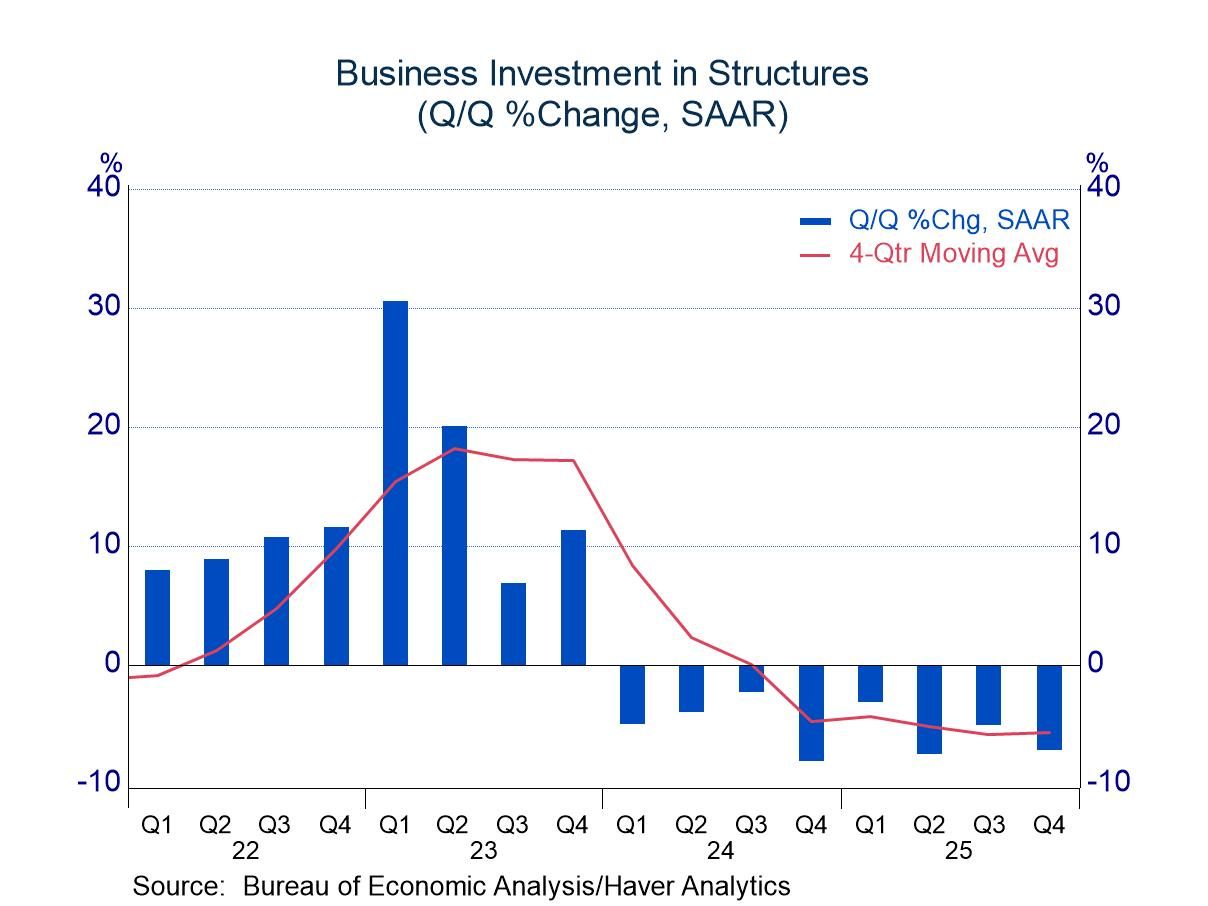

Business investment spending also was lighter than previously believed (2.3% versus 3.7%). The revision, however, was not especially surprising, as most of the adjustment occurred in construction of business structures, which has been notably soft recently. Indeed, investment in structures has now declined for eight consecutive quarters. Business outlays for software also were revised downward (3.8% versus 7.1%), but spending on equipment was a bit firmer than previously estimated (3.9% versus 3.2%).

The GDP data can be found in Haver’s USECON and USNA databases. USNA contains virtually all of the Bureau of Economic Analysis detail in the national accounts. The Action Economics consensus estimates can be found in AS1REPNA.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global