Global| Apr 28 2026

Global| Apr 28 2026EMU PPIs Show Instant Pressure

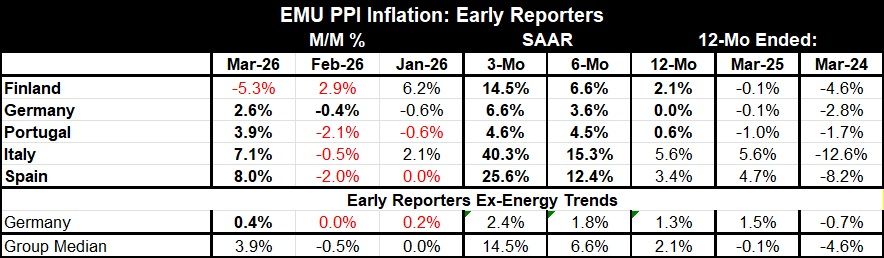

Early PPI reports in the monetary union show collective pressures building over the past year, with newly emergent pressures popping up strongly in March.

The sequence of monthly inflation observations for these five early reporters in March shows that inflation pressure has not been clearly building but did jump up suddenly in March. In February, before the Iran war, the median monthly PPI gain was -0.5%. In March, that jumped to +3.9% (median month-to-month gain). Monthly pressure does not show steady gains anywhere except moderately in Germany. Finland shows deceleration in progress (!) even through—especially through—March, as its PPI in March fell by 5.3%. But the whole Finish pattern is somewhat upside down, with prices up month-to-month by 6.2% in January and 2.9% in February. It is not a trend that is easy to understand.

However, the March monthly gains are strong enough to drive sequential inflation higher from 12-months, to 6-months, to 3-months across all early-reporting countries. Even the German ex-energy index shows acceleration on that profile.

On a year-on-year basis, two of the early reporters have PPI inflation below 2%. Finland has 12-month PPI inflation at 2.1%, but Italy and Spain have inflation much higher, up by 3.4% over 12 months in Spain and by 5.6% in Italy.

The PPI has been very well-behaved in the last few years. Looking at 12-month changes for the year ended in March, the median change for this group in 2025 was -0.1%, compared to -4.6% in 2024.

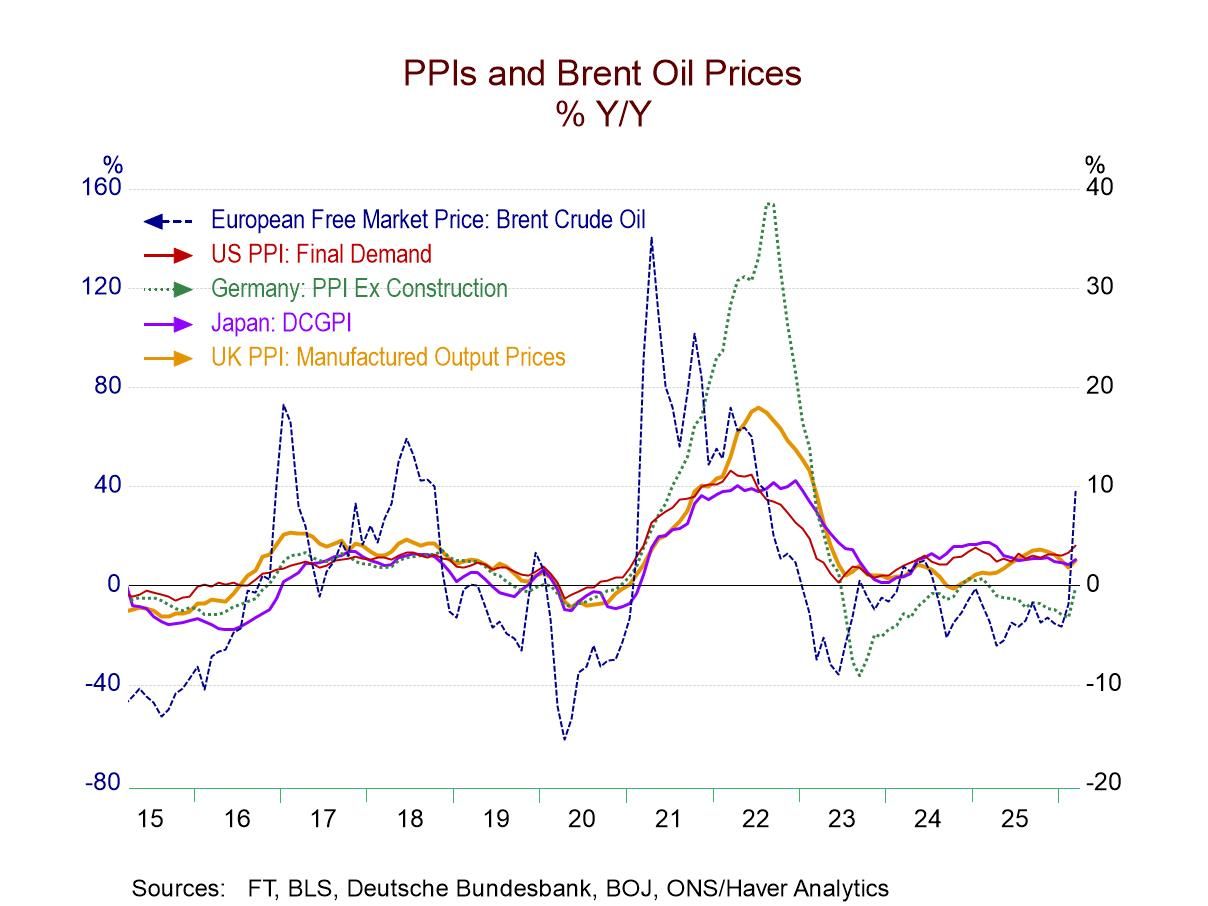

The chart shows the PPI flared sharply in 2021 and 2022, then fell quickly into line in 2023. Clearly, the inflation tune now is being called by oil prices, the same as for that spike prices in 2022 and 2023.

The hope is that the oil price bump up will not be as long-lived, that the war will end soon, with the Strait of Hormuz reopened, and that oil prices—and other inflation pressures—will sink back to prerevision norms relatively quickly. That could happen, but so could other outcomes so markets remain wary. One problem this time is the destruction of oil facilities and the shutting of oil fields that could cause high prices to linger longer.

A new dynamic However, there is now a new dynamic with the UAE leaving OPEC. OPEC has been a vehicle to harness common behavior to control oil prices mostly to keep them higher. While undermining OPEC (UAE pumps about 13% of OPEC capacity) at a time the U.S. oil prowess has risen, this defection will make it much harder for OPEC to control prices. When countries are not bound together, the incentive is for countries to cheat on their production quota. In a cartel arrangement, when many cheat, the output reduction does not hold, and oil prices fall. A cartel arrangement allows for supply control and reduction which raises prices. But once prices are up, each member has an individual incentive to cheat—to sell more than his quota share of oil at the higher price. But that undermines the cartel. So, this move, this exit of UAE from the cartel, will create instability in the OPEC by moving more production outside the OPEC framework, beyond its control. Unless the Saudis are willing to be the ‘swing man’ and cut back their output to keep prices on target—something the Saudis have been increasingly unwilling to do—OPEC will be in less control.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief