Asia| Mar 16 2026

Asia| Mar 16 2026Economic Letter from Asia: Strait Squeeze

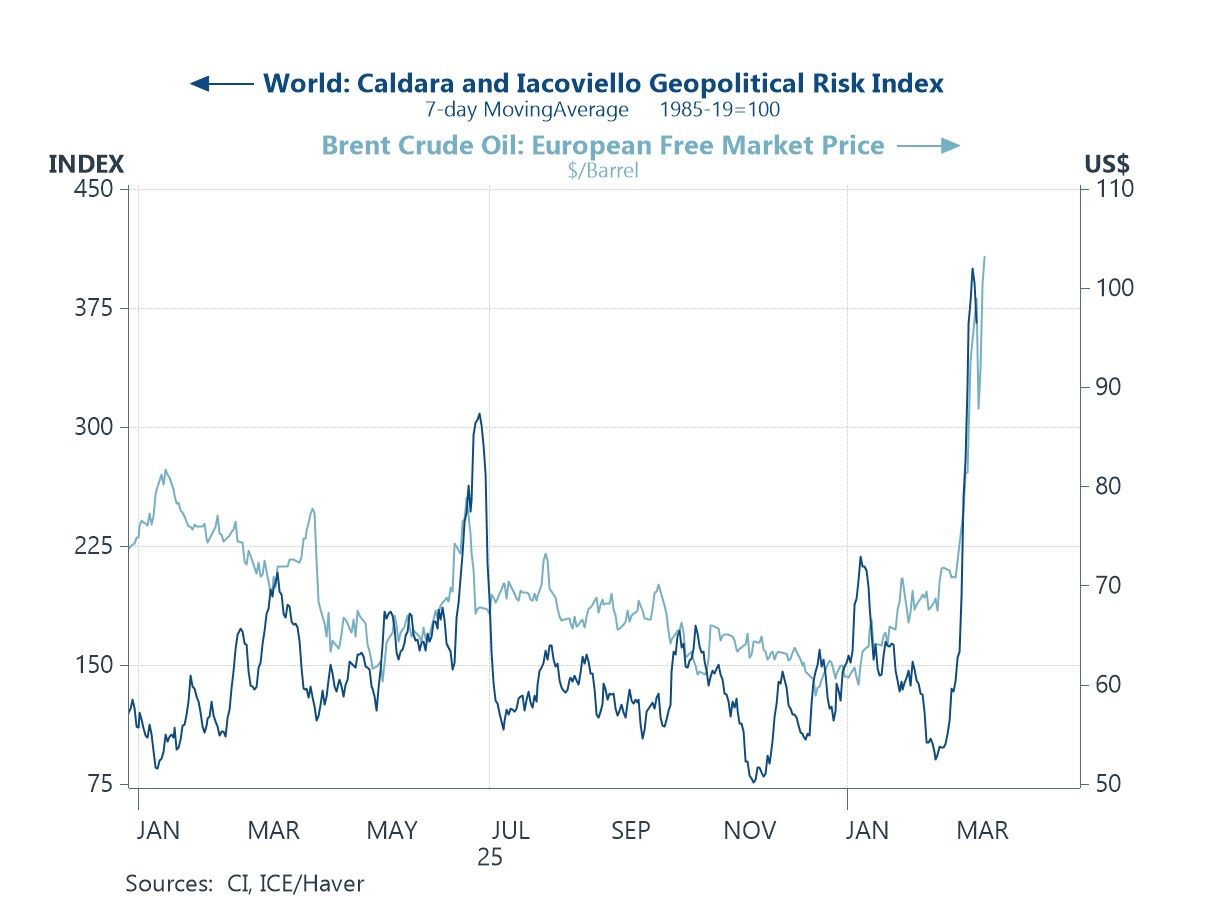

In our Letter this week, we examine the ongoing Iran war through an Asian lens. Geopolitical uncertainty and crude oil prices have remained elevated (chart 1), despite early reports concerning the potential for a brief conflict that tempered investor caution. Attention has now centred on the Strait of Hormuz, through which a significant share of global oil typically flows. With shipments now nearly halted (chart 2), much of the world’s energy flow has effectively stalled. While these developments have broad global implications, their impact on Asian economies is more nuanced. This partly reflects differences in energy mixes across the region (chart 3), as well as the historical relationship between oil prices and energy inflation (chart 4). Further compounding the challenges faced by Asian oil importers are currency effects: a broader risk-off turn in markets has weighed on several Asian currencies (chart 5), raising the local-currency cost of energy imports. Amid these pressures, several regional central banks are also set to decide on policy this week (chart 6), alongside major Western counterparts such as the Federal Reserve. Near-term rate cut expectations have been pushed back in many cases amid renewed inflation concerns, while in some Asian economies markets are even pricing in the possibility of further rate hikes.

The Iran war Two weeks in, the Iran war continues with no clear end in sight. Crude oil prices and geopolitical risk therefore remain elevated, as shown in chart 1, despite earlier news that had briefly tempered investors’ heightened caution. Even reports that the 32 members of the International Energy Agency are set to release around 400 million barrels in emergency reserves have done little to curb the surge in crude prices. Latest reports indicate that reserves for Asia will be released immediately, while supplies for Europe and the Americas will only become available from the end of March. Meanwhile, uncertainty surrounding the Strait of Hormuz continues to underpin elevated prices. The strait—currently blocked by Iran—handles roughly 20% of global oil flows. Iran has recently indicated that it may allow ships from certain countries to transit the waterway, though the situation remains fluid.

Chart 1: Global geopolitical risk and crude oil prices

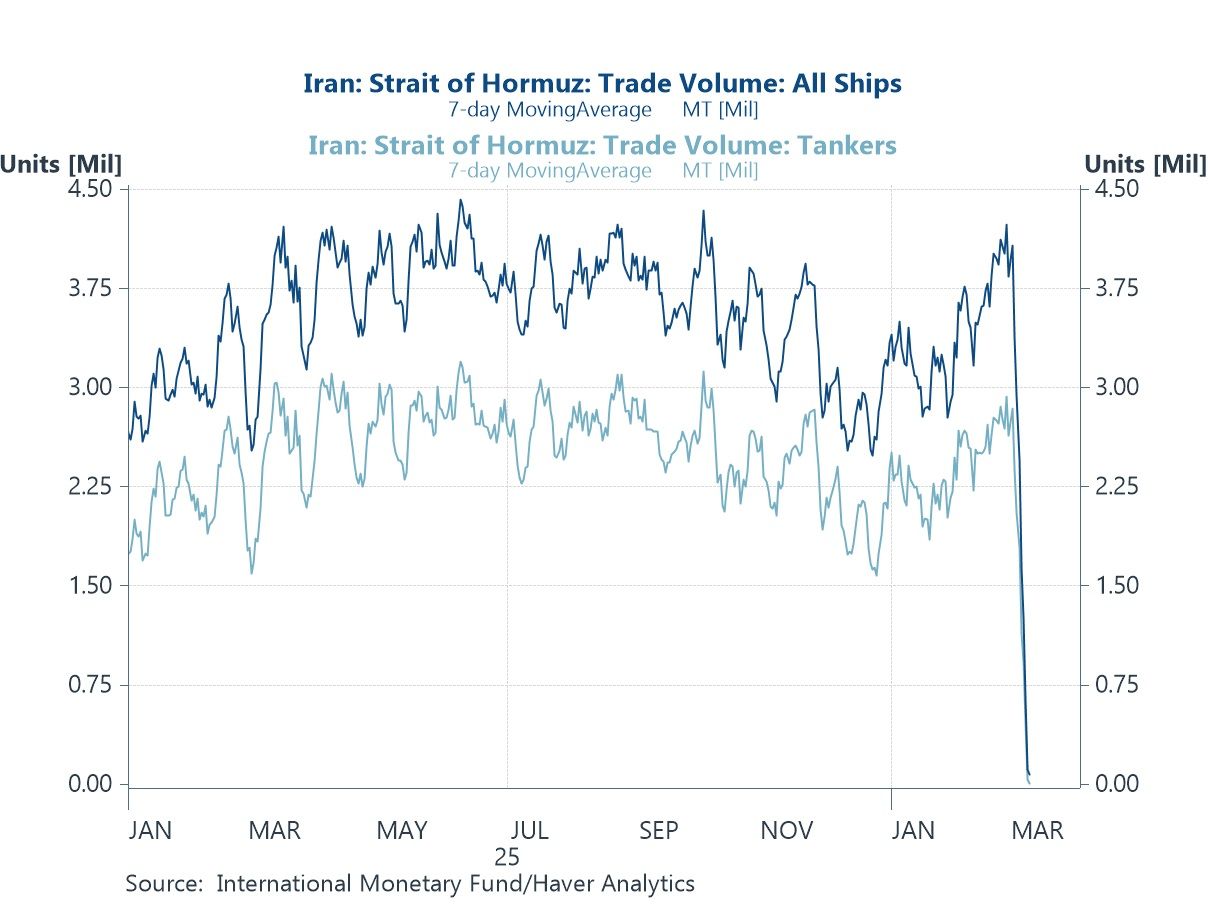

To illustrate the severity of the current choke point along the Strait of Hormuz, chart 2 shows the 7-day moving average of shipping volumes through the strait, based on estimates from the International Monetary Fund. The average has effectively fallen to zero for tanker traffic, while overall shipping volumes—including container ships, dry bulk carriers, and other vessels—have also dropped close to zero. This stands in stark contrast to the multi-million metric tons of average daily shipping volumes typically observed previously. While such shipping estimates may not capture every vessel and can be partially circumvented, the broader picture remains clear: the flow of energy—the lifeblood of the global economy—is now severely constrained. Strategic reserves may provide a temporary buffer, but a prolonged blockage would be difficult to sustain indefinitely and could carry significant economic consequences.

Chart 2: Trade volume through the Strait of Hormuz

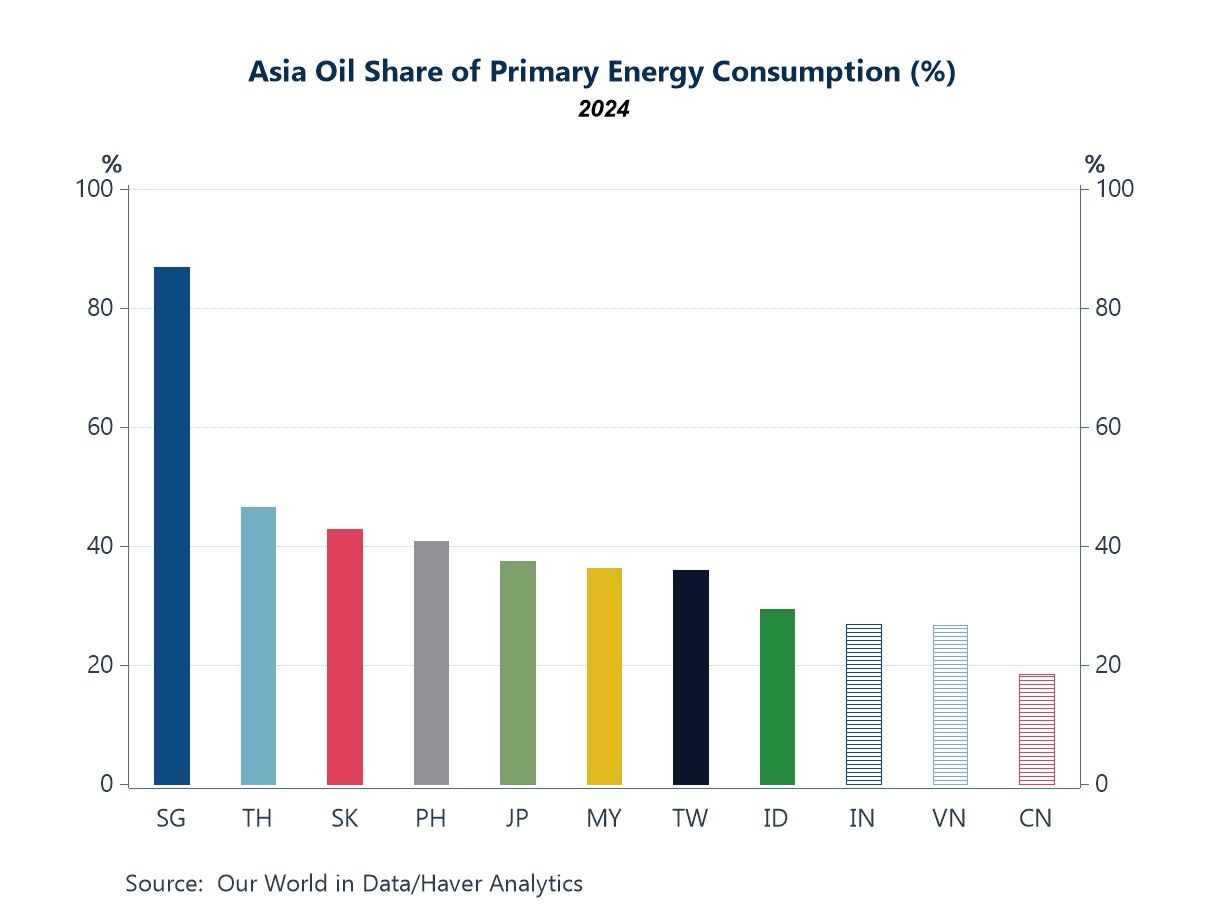

Asia’s exposure While the ongoing blockage of the Strait of Hormuz presents a global oil supply shock, its implications for Asia are more nuanced. Among Asian economies, Singapore stands out with the highest oil share in primary energy consumption—nearly 90%—while China has the lowest at just above 18%, as shown in chart 3. Other Asian economies generally fall between 25% and 50%. China’s relatively low oil share largely reflects its greater reliance on other energy sources, particularly coal and renewables. A high oil share in energy consumption alone does not necessarily constitute a major vulnerability in the context of an external supply shock. However, many Asian economies remain heavily dependent on imported oil to meet their energy needs. The combination of these two factors—significant oil intensity in energy consumption and high reliance on oil imports—places much of the region in a potentially precarious position.

Chart 3: Asia’s oil share of primary energy consumption

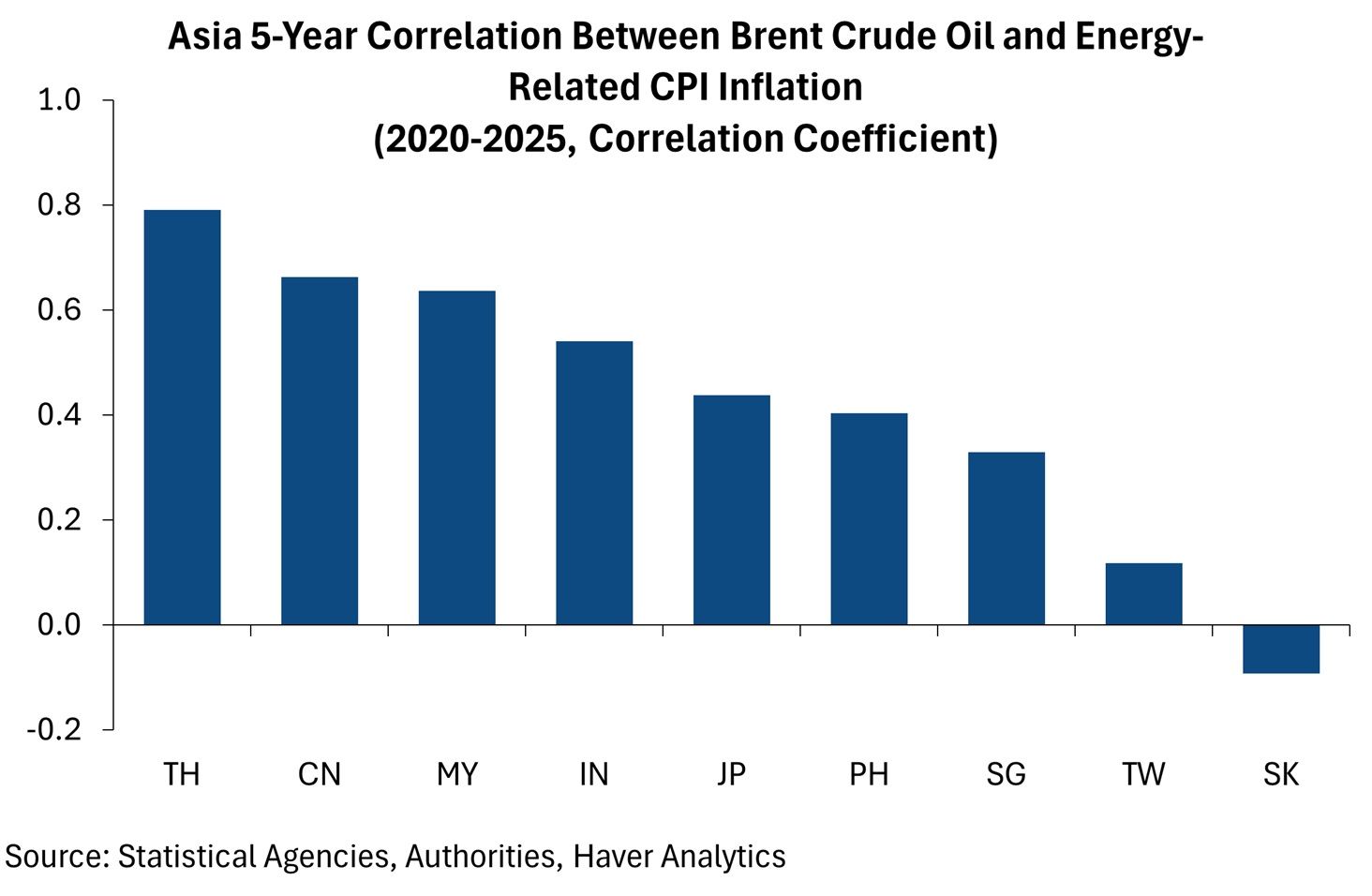

Given Asia’s exposure to external oil supply shocks—now immediately visible through higher oil prices—one of the most direct channels of concern is inflation. Chart 4 illustrates what could potentially unfold, based on the historically strong correlations between Asian economies’ energy-related components of CPI inflation and Brent crude oil prices, which serve as a benchmark for global crude prices. In several cases, the relationship is substantial; for example, Thailand records a five-year correlation coefficient of nearly 0.8. That said, the relationship is not uniformly strong across all economies. In places such as Taiwan and South Korea, the correlation appears weaker, which may partly reflect domestic policy measures such as price caps—though the durability of such interventions remains uncertain. Moreover, governments that maintain energy subsidies or similar support mechanisms could face increasing fiscal strain, as higher global oil prices gradually erode available fiscal resources.

Chart 4: Asia 5-year correlation between Brent crude prices and energy-related CPI inflation

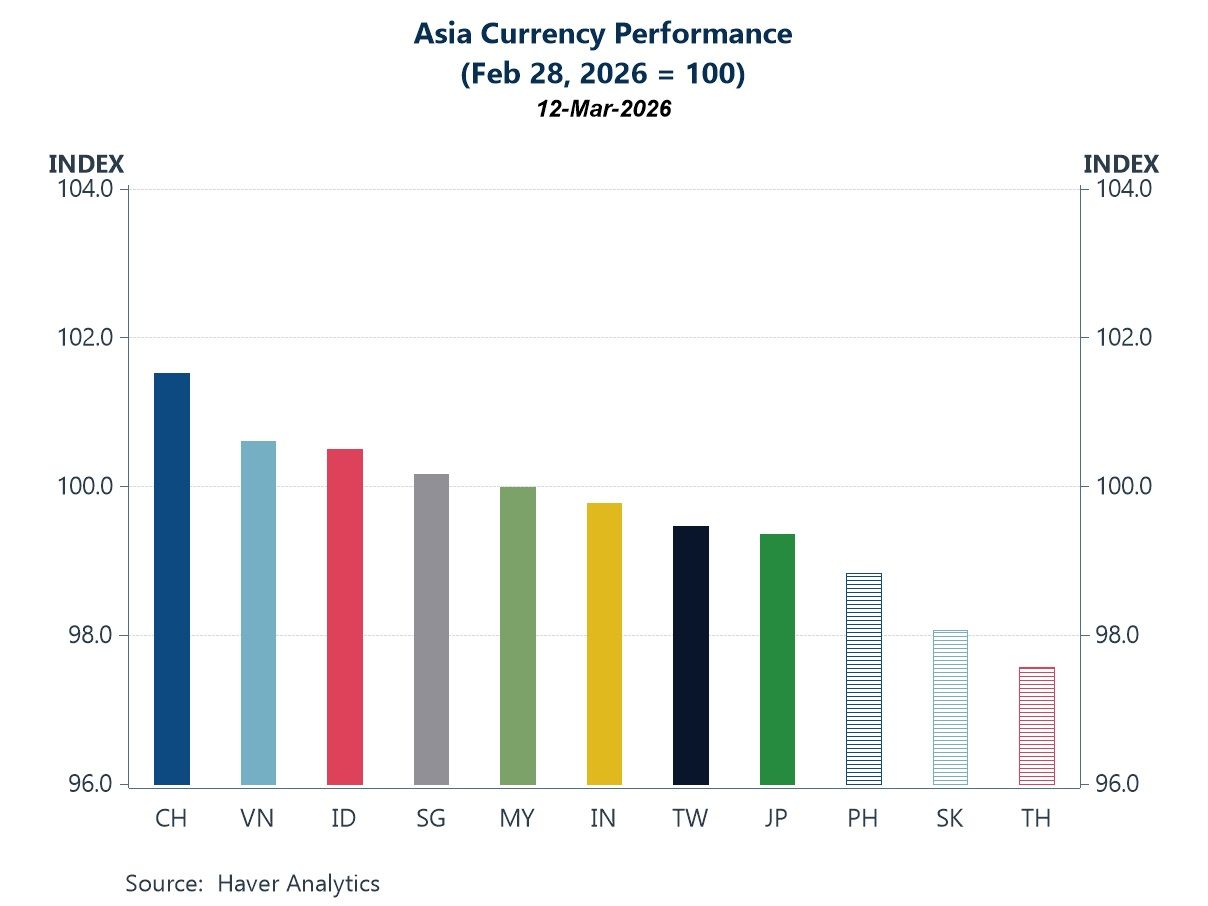

As if these pressures were not sufficient, Asia’s oil importers also face compounding currency effects. The deterioration in the global geopolitical environment has dampened risk sentiment broadly, which often weighs on Asian currencies, as shown in chart 5. With crude oil prices surging due to the supply shock, and regional currencies weakening at the same time, the cost of importing oil is being pushed higher by two forces simultaneously—higher global oil prices and adverse exchange rate movements. This dual pressure further amplifies the burden on many Asian economies that rely heavily on imported energy.

Chart 5: Asia FX performance

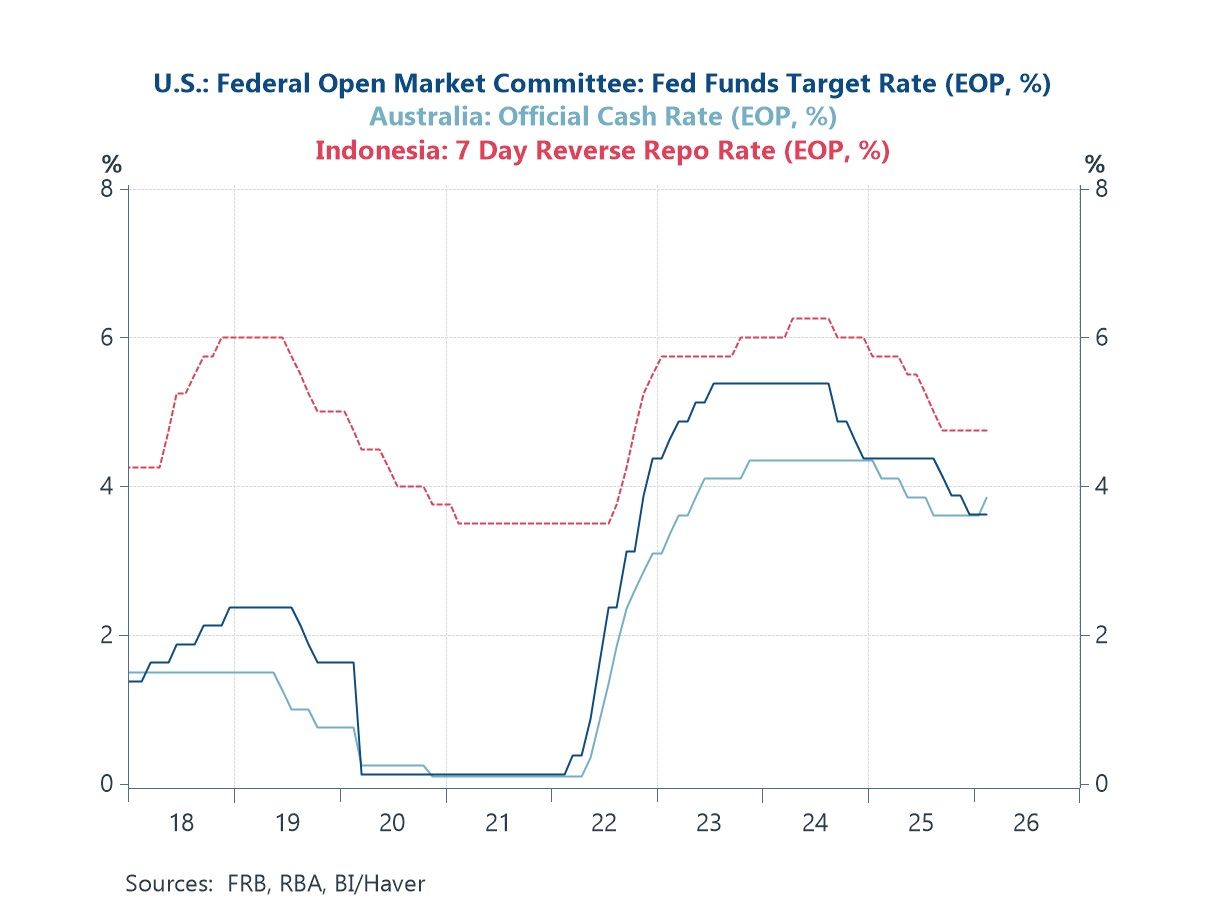

Monetary Policy Given the ongoing surge in crude oil prices and the still-fluid situation in the Middle East, it is perhaps unsurprising that market expectations for near-term central bank easing in several economies have been dialled back. In some cases, expectations of rate hikes have even begun to build, largely on the back of renewed inflation concerns. That said, if the spike in crude oil prices ultimately proves transitory, there would in principle be little reason to delay policy easing if economic conditions warrant it. The key uncertainty now lies in how long the current surge will persist. Alongside the Americas and Europe, Asia will see a series of central bank decisions in the coming week, including from the Reserve Bank of Australia, Bank Indonesia, and Central Bank of the Republic of China (Taiwan). Unlike in many other economies—where investors largely expect policy rates to remain unchanged in the near term—markets are pricing in another 25-basis-point rate hike at the Reserve Bank of Australia’s meeting this week. Meanwhile, expectations for near-term rate cuts by Bank Indonesia may be pushed further out, given the ongoing uncertainty surrounding Iran and the associated inflation risks.

Chart 6: US, Australia, and Indonesia policy rates

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief