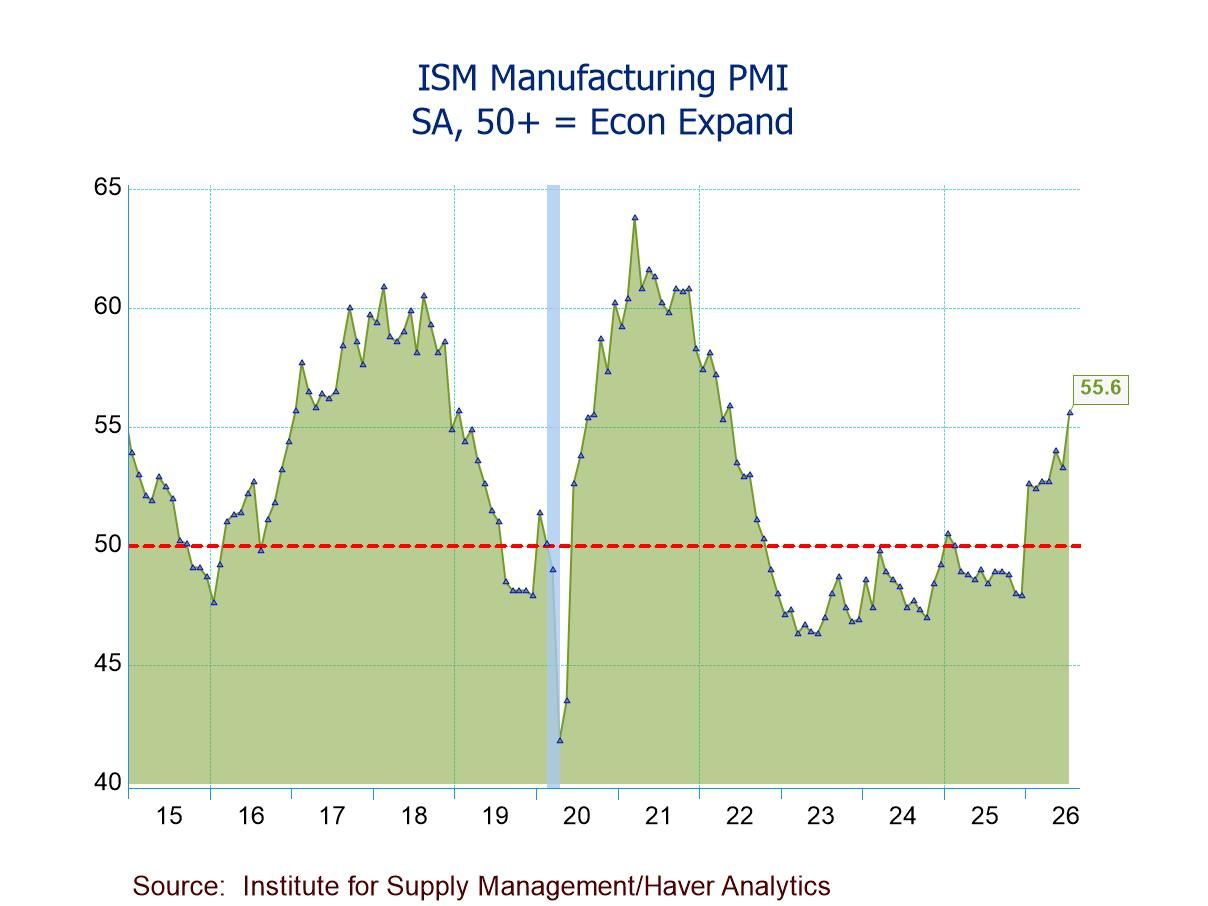

Q1 GDP: Weathering the Challenges; Trend-Like Growth

Summary

- Robust business investment led the advance; moderate support from consumers.

- Government spending jumped with the reopening of most federal agencies.

- The trade sector remained volatile, making a sizeable negative contribution in Q1.

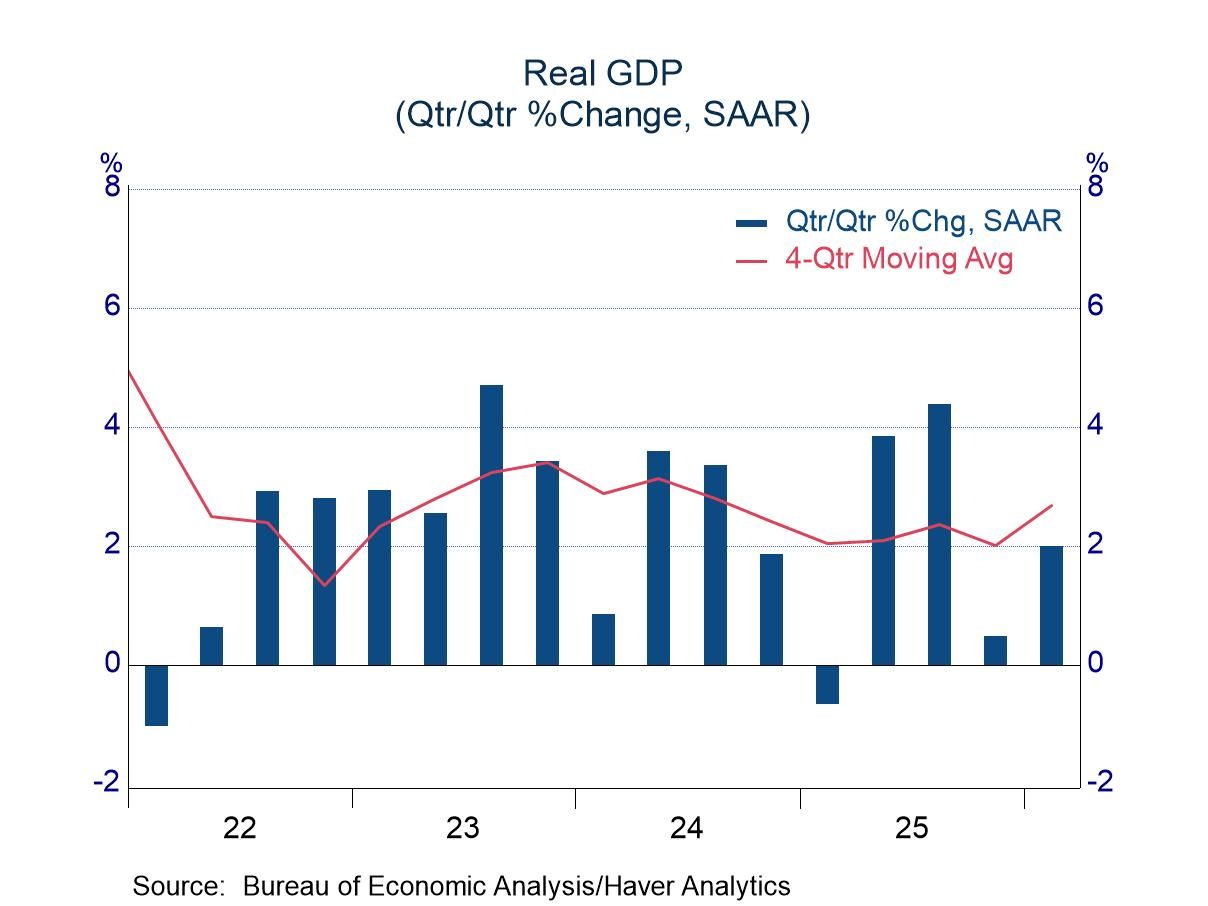

Real GDP grew at an annual rate of 2.0% in the first quarter of 2026, almost identical to the expected advance of 2.1%. The latest change was comfortably within the range of recent observations and close to the economy’s potential rate of growth. The year-over-year change totaled 2.7%, but that shift reflected what might be viewed as a special factor (robust growth in the second and third quarters that offset a trade-tariff-induced drop in 2025-Q1 GDP).

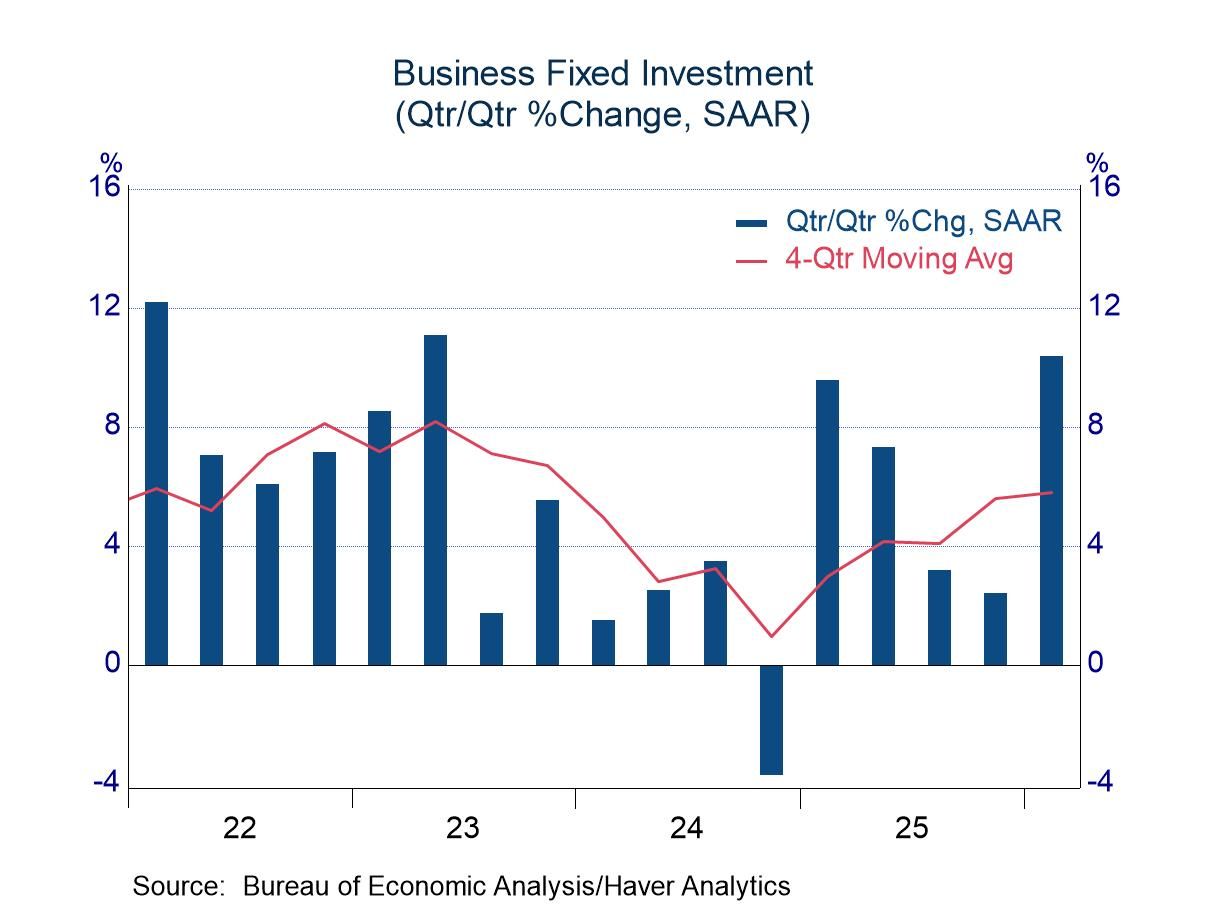

Business fixed investment was the star of the show in the first quarter, registering growth of 10.4%. Outlays for information processing equipment and software were especially strong, while outlays for industrial equipment and Research & Development contributed positively as well. Outlays for structures remained decidedly soft, dropping for the ninth consecutive quarter. Building of data centers have been vigorous, but softness in offices and manufacturing facilities has dwarfed the strength in this new area.

Federal spending surged 9.4% in Q1, but the rise reflected the reopening of most federal agencies after their closure during much of the fourth quarter. Excluding this noise, support from the federal government has been softening. Nondefense outlays peaked in the fourth quarter of 2024, and they were 6.9% shy of that total in the first quarter. Defense spending also peaked in 2024-Q4 and has eased 2.4% since then. Defense spending most likely will grow in coming quarters because of the efforts in the Middle East. Orders for defense goods have already started to rise.

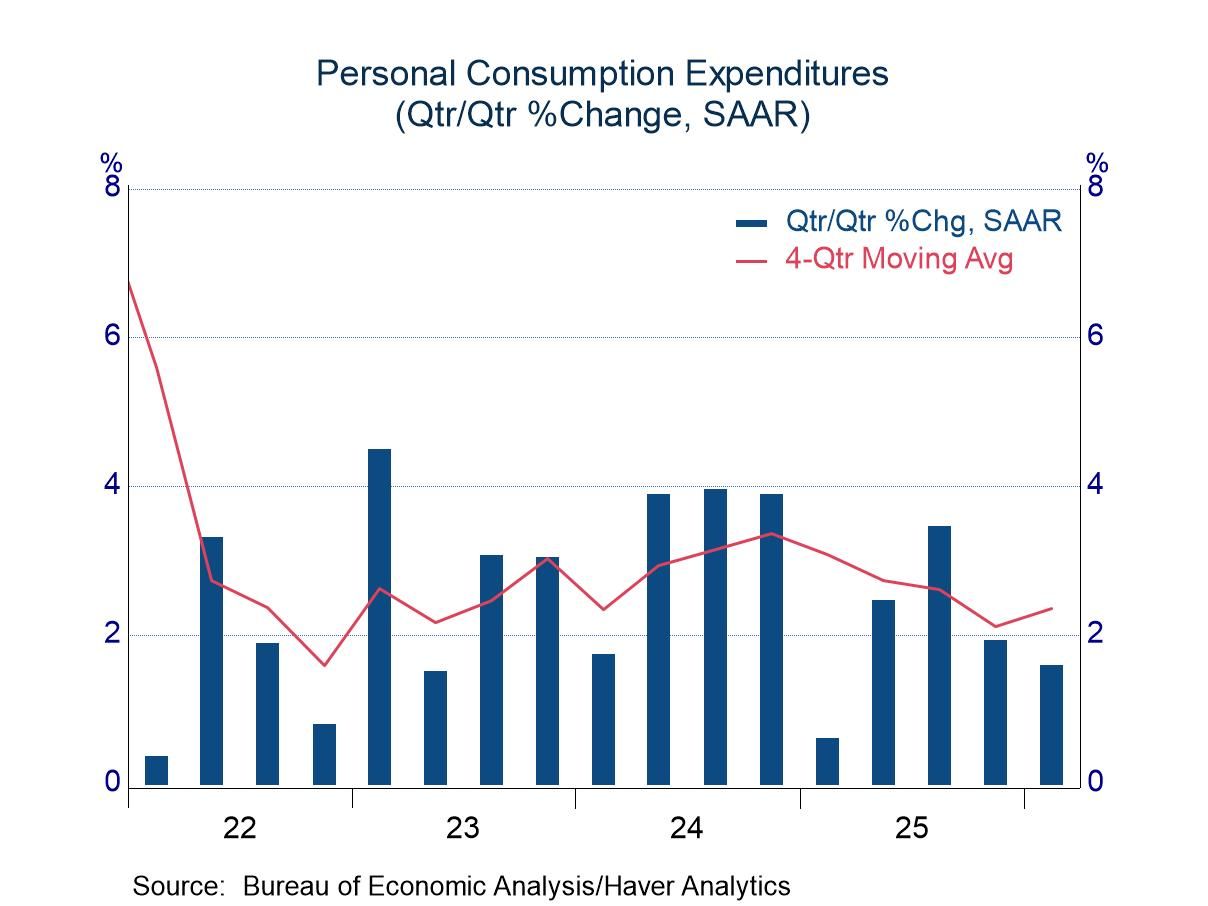

Consumer spending rose 1.5% in the first quarter, a bit shy of the 2.1% pace over the four quarters of last year and less than half the rates in 2023 and 2024. Consumer spending showed signs of softening in late 2025 and January of this year, but activity picked up in February and March. Firm tax refunds might have provided a boost to household spending in the latest months. Some of the tax cuts from the One Big Beautiful Bill were applied retroactively to 2025, but withholding schedules were not adjusted last year. Thus, many households are receiving larger-than-normal tax refunds.

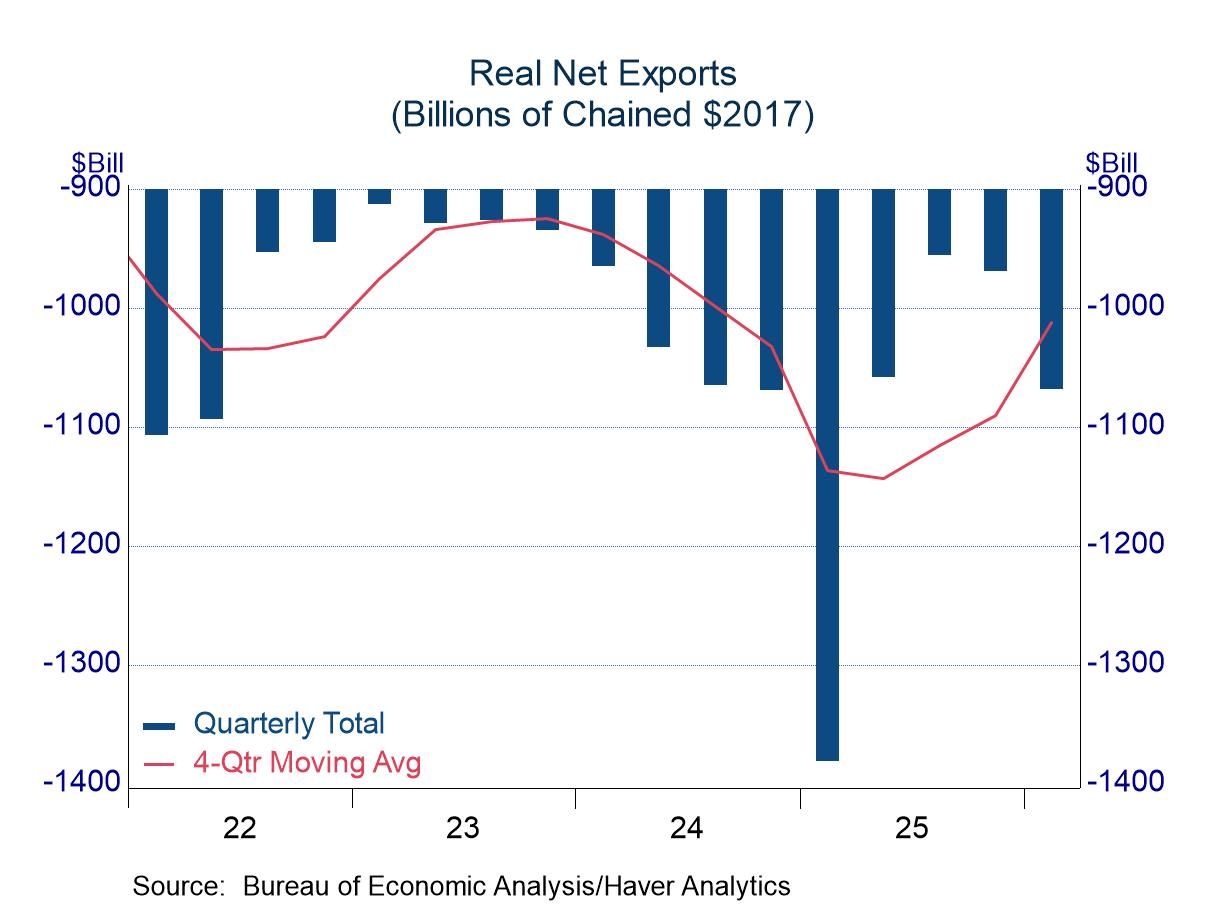

International trade acted as a drag on economic growth in Q1, with net exports subtracting 1.3 percentage points from the GDP increase. Exports did well in the first quarter with growth of 12.9%, but imports were even stronger with a jump of 21.4%. The real trade deficit of $1.1 trillion was noticeably smaller than the shortfall of $1.4 trillion in 2025-Q1 when importers were rushing to get goods into the US before the imposition of tariffs. Still, the trade shortfall was sizeable and its effect on growth noticeable.

The GDP data can be found in Haver’s USECON and USNA databases. USNA contains virtually all of the Bureau of Economic Analysis detail in the national accounts. The Action Economics consensus estimates can be found in AS1REPNA.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Asia

Asia