Global| Apr 30 2026

Global| Apr 30 2026Charts of the Week: Tension Beneath the Surface

by:Andrew Cates

|in:Economy in Brief

Summary

Against a backdrop of persistent geopolitical tensions, firmer energy prices and a busy week of central bank meetings—including the Fed, ECB, BoE and BoJ—financial markets have remained notably resilient, even as the macro narrative has softened at the margin. The message from this week’s charts is one of growing tension beneath that surface calm. Front-end bond yields have moved higher, signalling a shift toward a more cautious, “higher-for-longer” policy outlook (chart 1). At the same time, real-time recession indicators for the United States suggest risks remain contained for now (chart 2). Consumer confidence data paint a more uneven picture, with sharper declines in the euro area and UK than in the US, highlighting regional vulnerabilities to the current energy shock (chart 3). The ECB’s latest bank lending survey reinforces this, pointing to tighter credit conditions and weaker demand—factors that are likely to weigh further on European growth (chart 4). By contrast, developments in the semiconductor sector underline a different dynamic: an intensifying global boom, with accelerating price pressures reflecting both strong AI-driven demand and emerging supply-side constraints linked indirectly to energy and logistics disruptions (chart 5). Finally, labour market data confirm that the AI surge is not merely a market narrative but a tangible structural shift, with hiring for AI-related roles accelerating across economies (chart 6). Taken together, these signals point to a more complex macro environment—one in which resilient markets coexist with softening growth, more persistent inflation risks and increasingly delicate policy trade-offs.

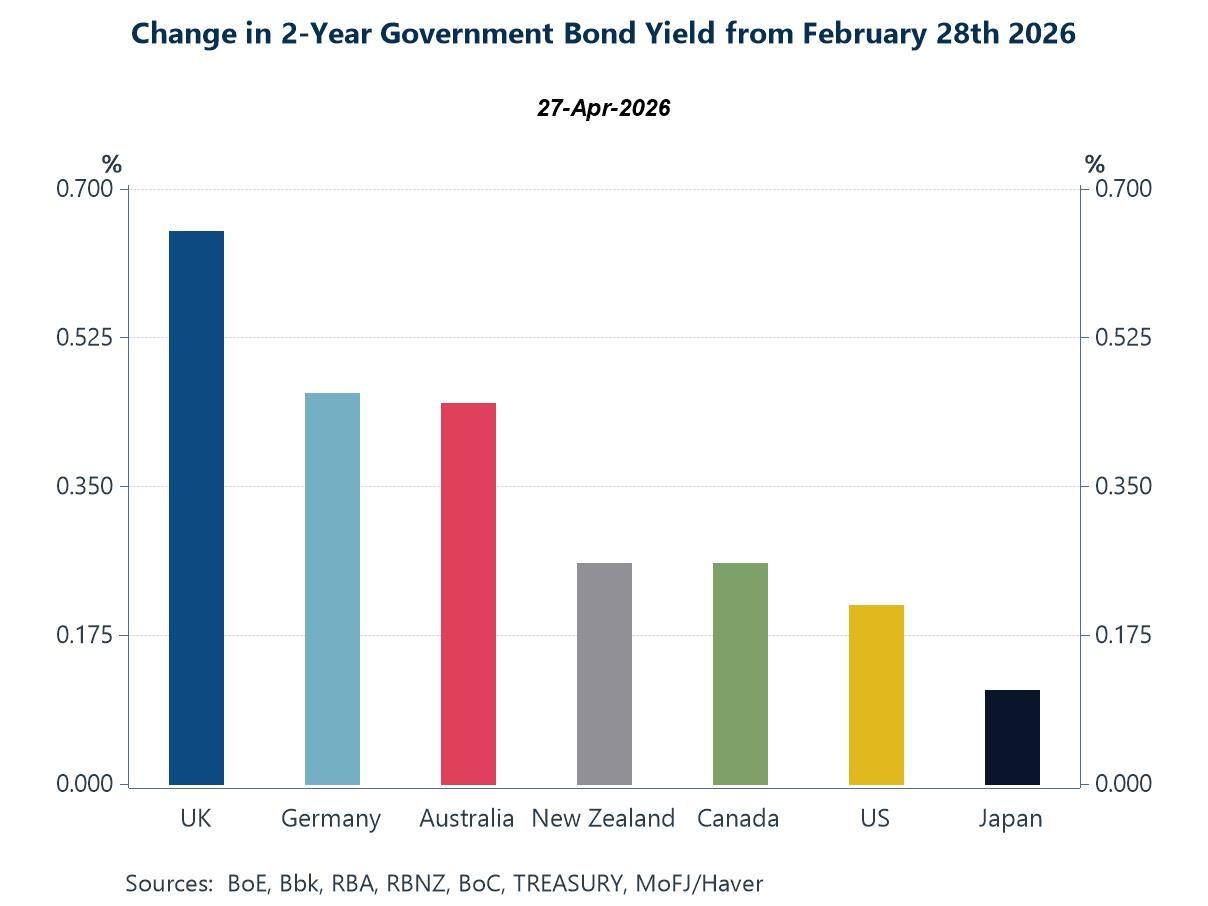

Front-End Yields Reflect Policy Reassessment Against a backdrop of key central bank meetings either having just taken place or imminent, short-dated government bond yields have moved decisively higher across most major economies since the escalation of the Middle East conflict, with the sharpest increase seen in the UK. The rise in 2-year yields reflects a repricing of near-term monetary policy expectations, as markets respond to the inflationary implications of higher energy prices and the growing likelihood that central banks will delay easing cycles. Moves have been most pronounced in economies where inflation is expected to be more persistent—most notably the UK—while increases have been more modest in the US and particularly Japan, where policy normalisation remains gradual. In effect, the front end of the curve is signalling a shift away from the “rate cuts soon” narrative that prevailed earlier in the year toward a more cautious, higher-for-longer policy outlook.

Chart 1: Markets Reprice “Higher for Longer” as Energy Shock Bites

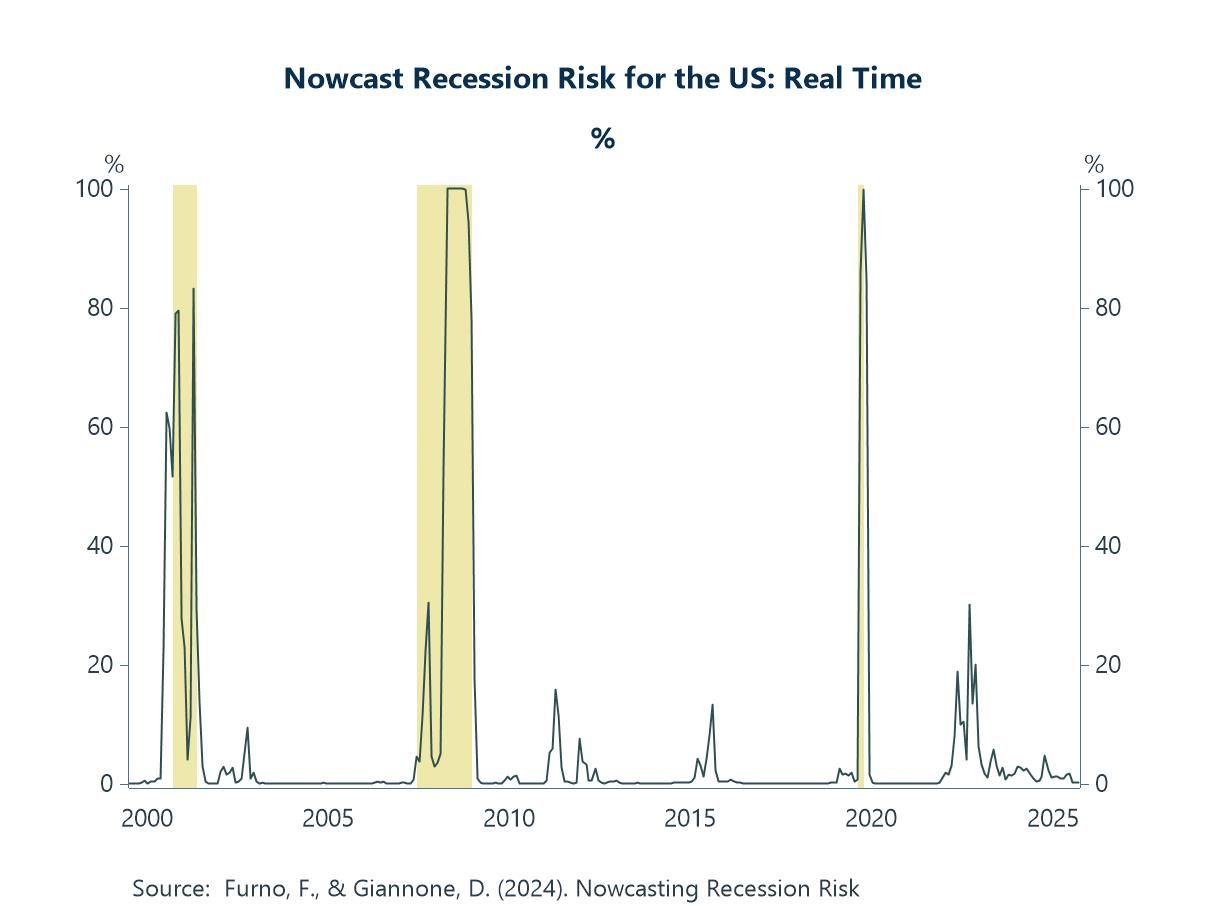

US Recession Risks Remain Contained—For Now Despite the recent deterioration in the macro backdrop, real-time recession risk indicators for the US remain relatively subdued. This is notable given the combination of softer growth momentum, higher bond yields and heightened geopolitical risk. The nowcast—derived from a blend of high-frequency activity data and financial stress measures—has historically tended to move sharply when conditions turn, rather than drift higher gradually. That asymmetry is important in the current environment. While recession risks are not yet flashing red, past cycles suggest they can reprice abruptly, and arguably at present if energy-driven inflation were to feed much more forcefully into financial conditions or begin to weigh more materially on demand.

Chart 2: A Nowcast of US Recession Risk

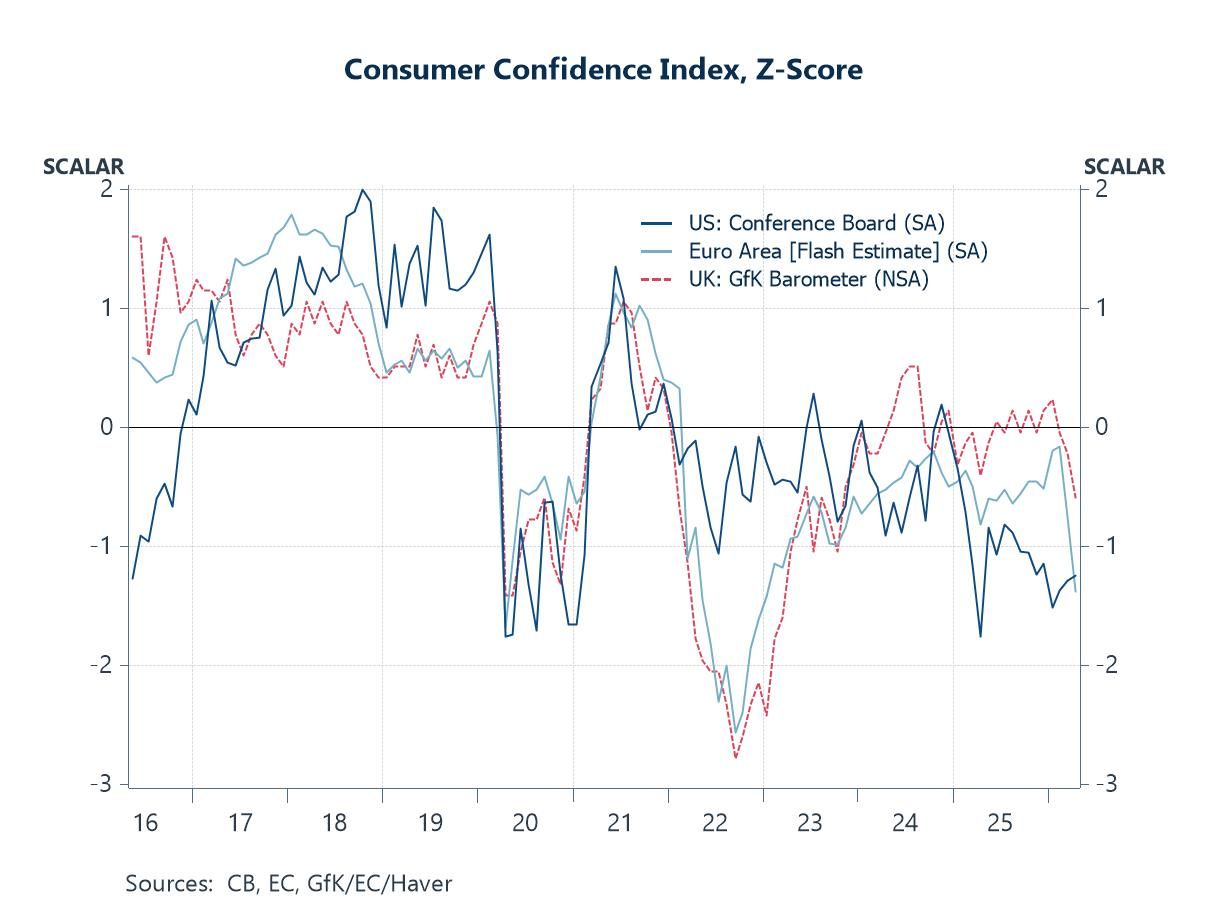

Consumer Confidence Diverges: Europe and UK Slide, US Stabilises Consumer confidence has weakened across the major economies, but the deterioration has been more pronounced in the euro area and the UK than in the US. While sentiment in the US has recently edged up, it remains at relatively subdued levels. By contrast, confidence in Europe and the UK has fallen more sharply, reflecting greater exposure to higher energy costs and a more direct squeeze on real household incomes. This divergence is consistent with broader macro trends, suggesting that demand in Europe may prove more sensitive to the current shock, with weaker sentiment feeding more quickly into consumption.

Chart 3: Consumer confidence gauges in the US, euro area and UK

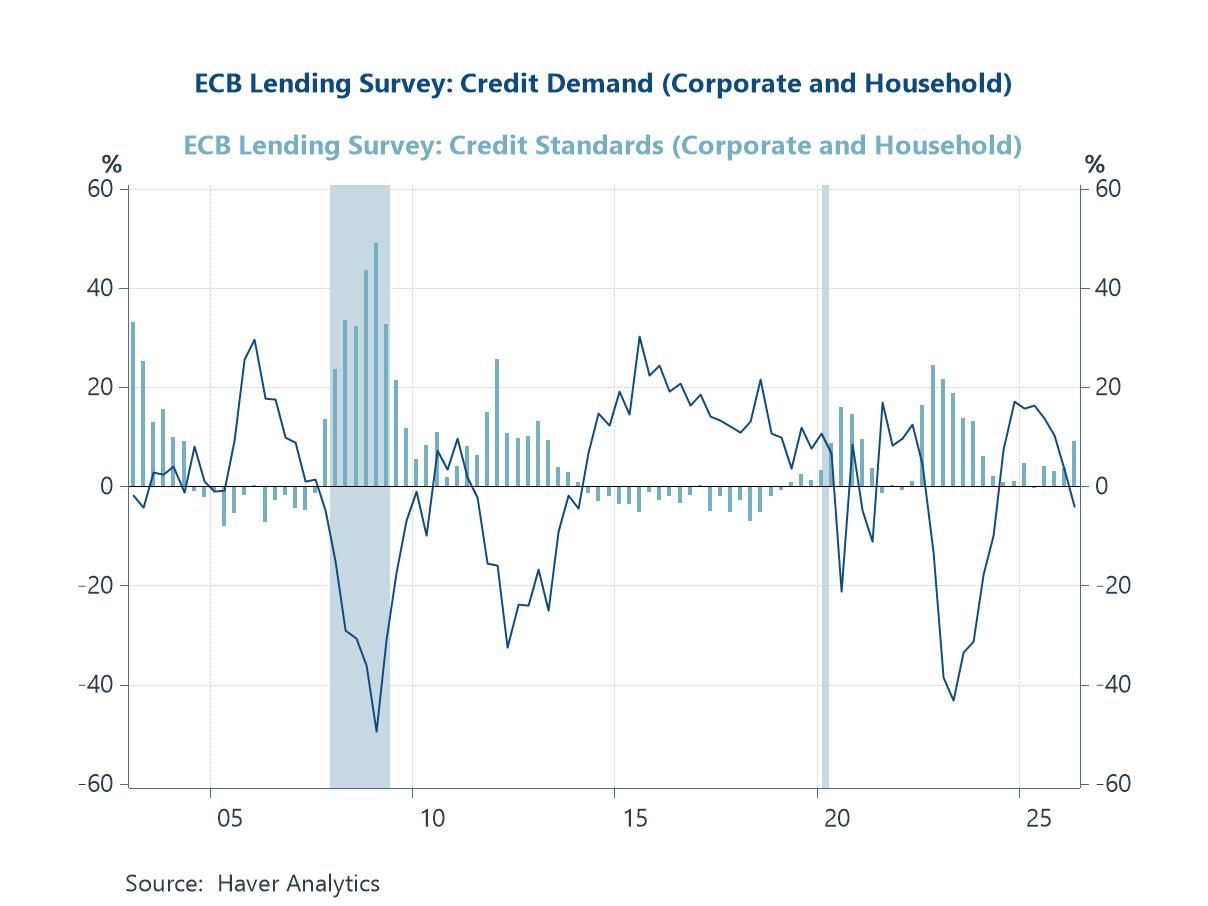

Euro area Credit Conditions Turn More Restrictive The latest ECB lending survey points to a clear tightening in credit conditions across the euro area, with banks raising lending standards for both firms and households while loan demand weakens. This combination—more restrictive supply alongside softer demand—is typically associated with a cooling in activity, particularly in interest-sensitive sectors. Recent evidence suggests that higher perceived risks, rising funding costs and geopolitical uncertainty are all weighing on banks’ willingness to lend, while weaker confidence and reduced investment appetite are dampening borrowing needs. The result is a tightening in financial conditions that is likely to amplify the broader slowdown already evident in survey data, reinforcing the more fragile growth dynamics now emerging across the region.

Chart 4: ECB Lending Survey: Tighter Credit, Weaker Demand

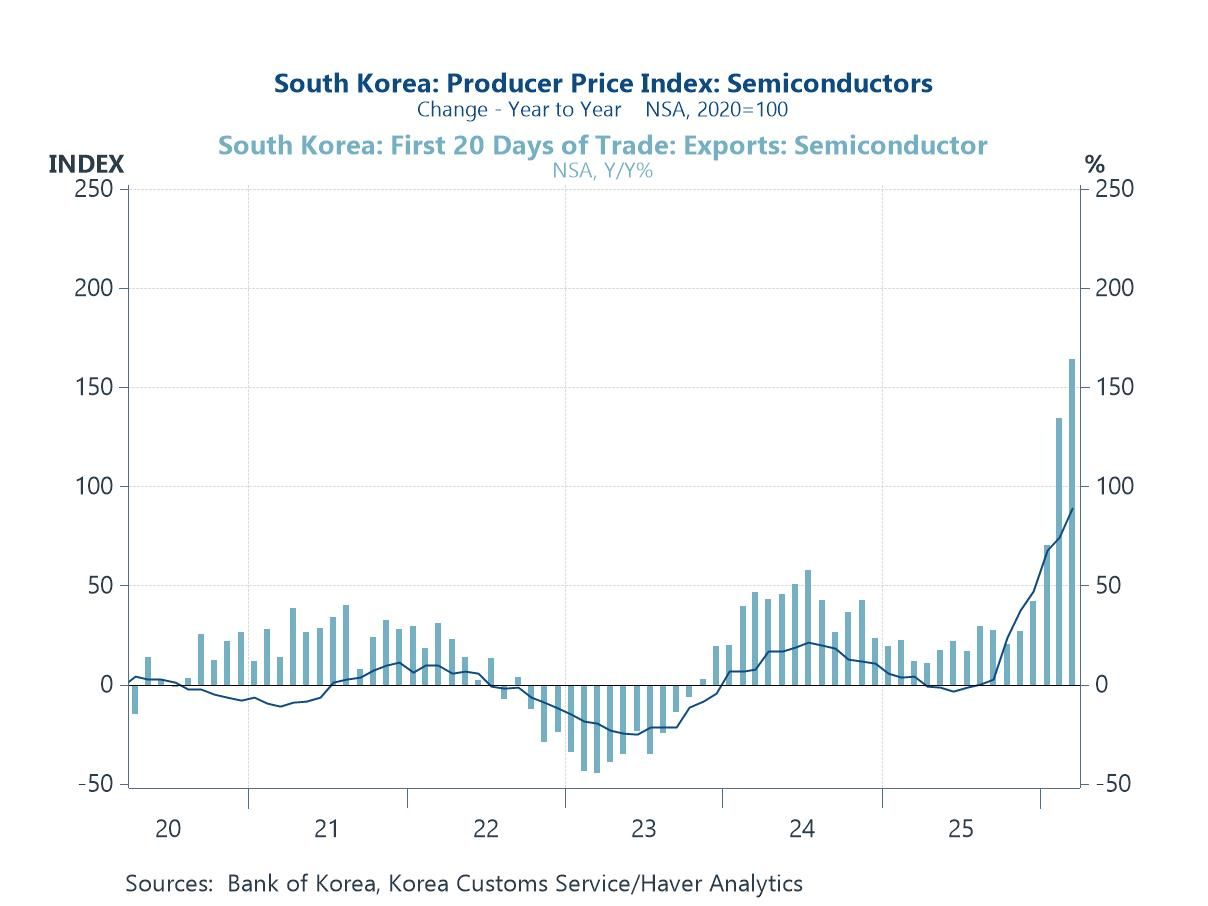

An Intensifying AI Boom with Supply-Side Undercurrents Against the backdrop of surging AI-related investment, semiconductor prices are not just high—they are rising at an increasingly rapid pace. This chart shows a clear acceleration in both prices and export values, pointing to an intensifying boom in global chip demand. While this is in part a reflection of strong, structural demand, supply-side factors may also be playing a growing role. Although the Middle East is not a direct source of key chip-making minerals, it is central to the energy and petrochemical inputs that underpin semiconductor production. Ongoing geopolitical tensions are therefore likely feeding into higher costs and renewed frictions across supply chains. The combination of accelerating demand and tightening supply conditions suggests that semiconductor inflation could prove more persistent—and more globally consequential—than currently assumed.

Chart 5: South Korea: Semiconductor Prices Continue to Accelerate

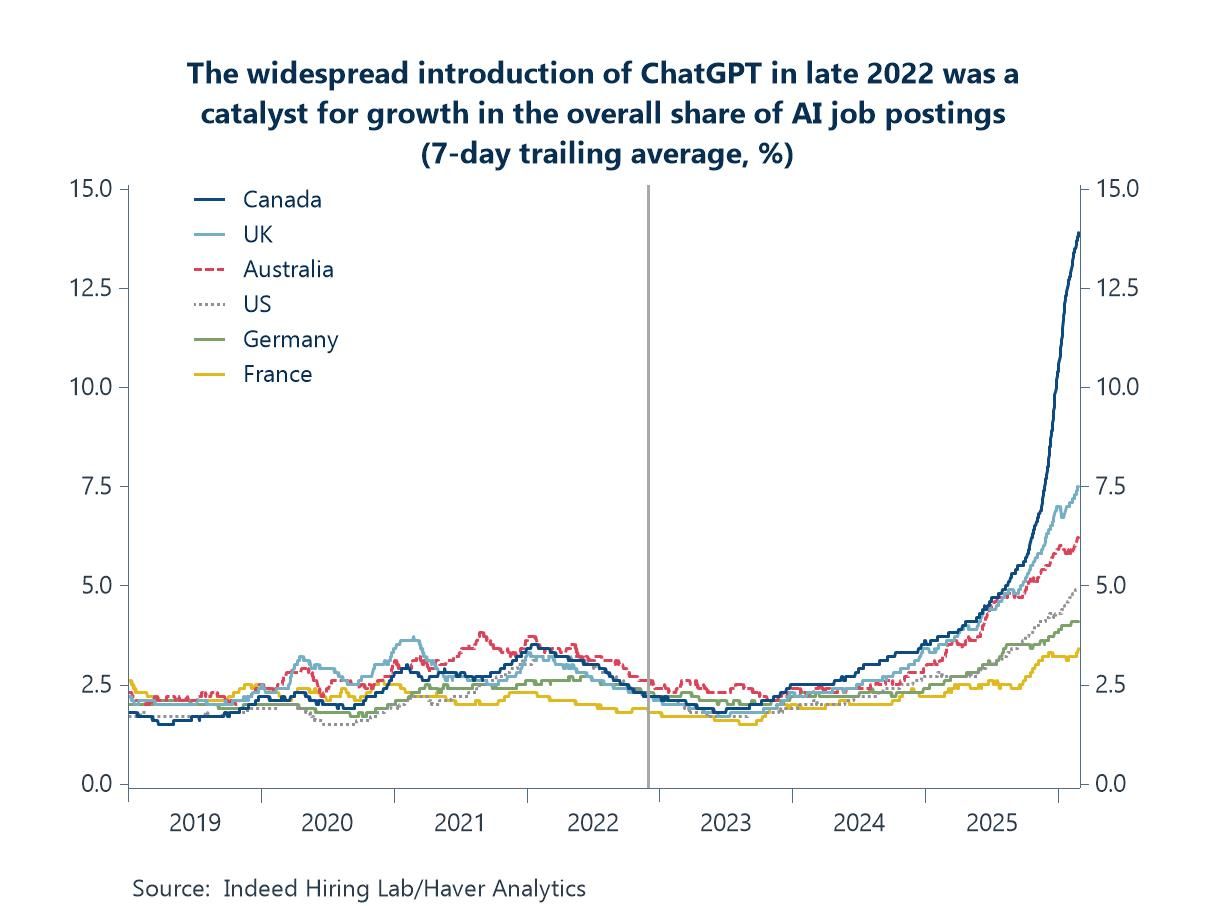

Labour Markets Reflect the AI Acceleration Our final chart this week highlights the extent to which the current AI boom is now feeding through into labour markets. This high-frequency indicator—based on the share of job listings containing AI-related keywords—shows a sharp and sustained increase since the widespread adoption of generative AI tools in late 2022. What began as a more traditional build-out in machine learning roles has evolved into a broader and more intense wave of hiring tied to generative AI capabilities, with demand accelerating markedly across multiple economies. The scale and persistence of this trend point to a structural shift rather than a cyclical upswing, reinforcing the view that AI is becoming an increasingly important driver of investment, productivity expectations and, potentially, broader macroeconomic dynamics.

Chart 6: AI Hiring Surges as Generative Boom Intensifies

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief