Unusually Large Upward Revision in Third Estimate of U.S. Q1 2026 Real GDP Growth

by:Sandy Batten

|in:Economy in Brief

Summary

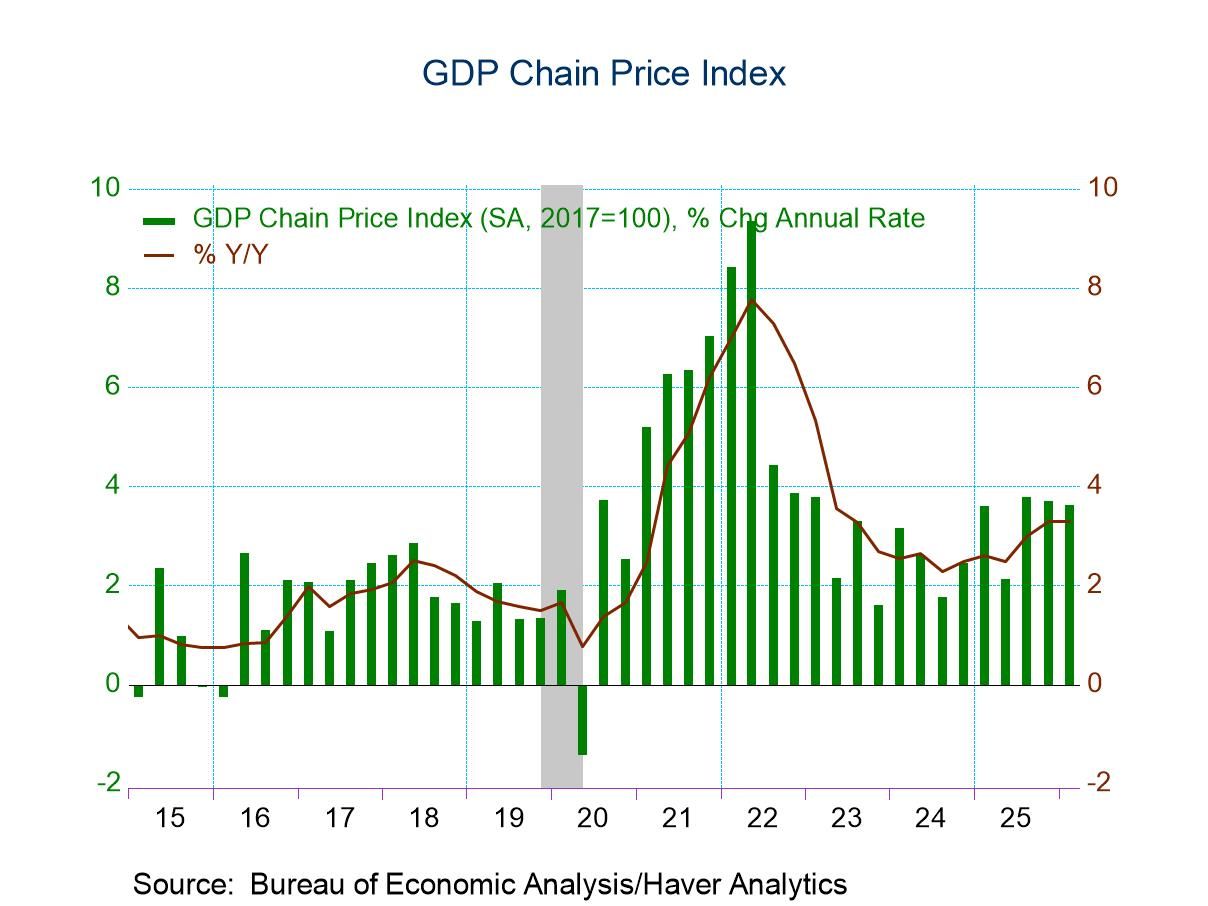

- Q1 GDP growth was unexpectedly revised up to 2.1% q/q saar in the third estimate, up from 1.6% in the second estimate and inching past the 2.0% advance estimate.

- A meaningful downward revision to imports was the primary factor behind the upward revision, leading to a much smaller subtraction from net exports.

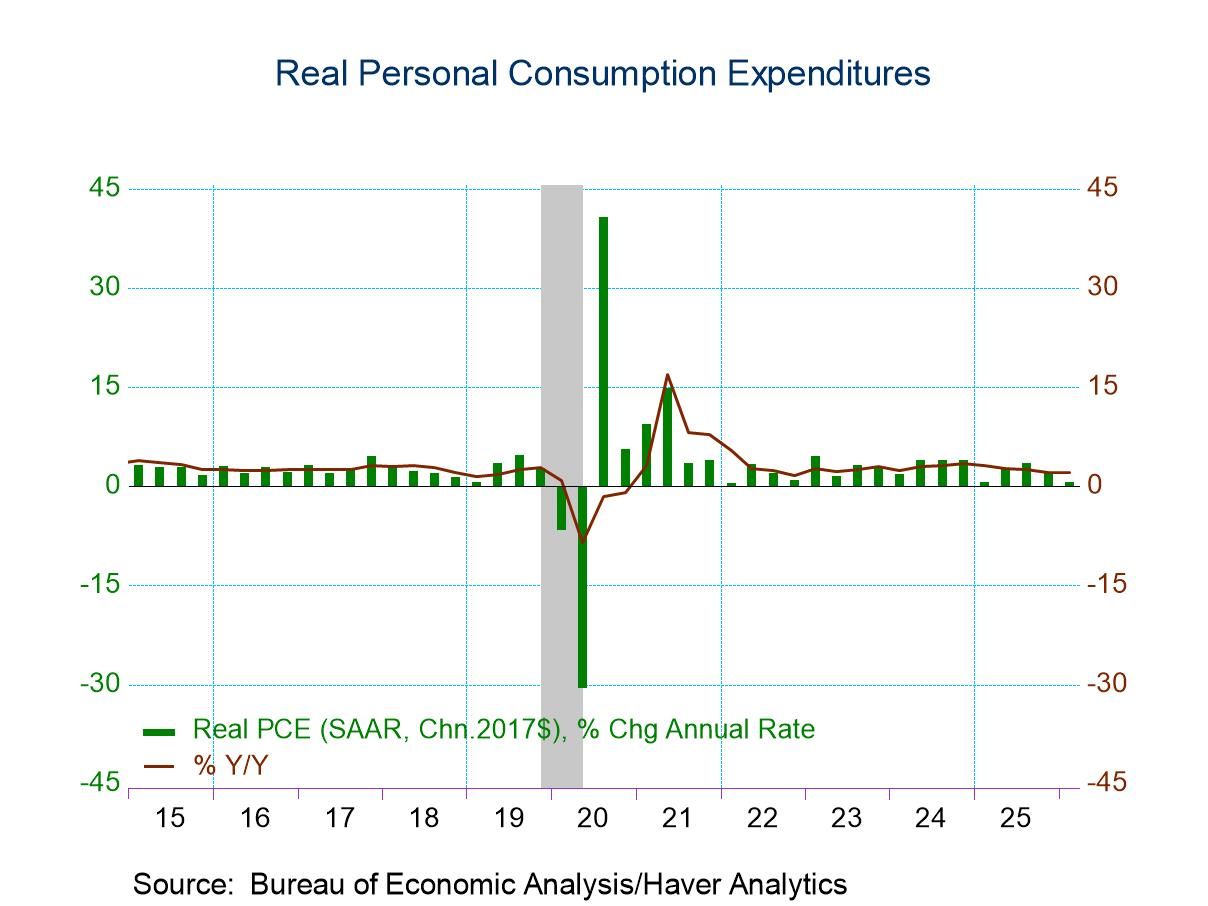

- Personal consumption expenditures growth was revised down to 0.5% q/q saar, the slowest pace since Q1 2022, due mostly to a downward revision to household spending on financial services and insurance.

- With the downward revision to import demand and PCE, domestic demand growth was revised down meaningfully to 1.7% q/q from 2.4%.

Q1 2026 real GDP growth was revised up to 2.1% q/q saar in the third estimate from 1.6% in the second estimate, slightly eclipsing the 2.0% advance estimate, according to figures released by the Bureau of Economic Analysis today. The Action Economics Forecast Survey looked for a slight upward revision to 1.7%. The major factor behind the upward revision was a large downward revision to import growth to 11.8% from 21.1% in the second estimate. The downward revision in imports was accompanied by a much smaller downward revision in export growth (10.9% versus 13.1%), leading to a meaningful downward revision to the trade deficit. Accordingly, net exports subtracted 0.4%-point from overall GDP growth in Q1, down markedly from -1.3%-point in both the second and advance estimates. The BEA stated that the downward revision to imports was widely spread—in goods (led by imports of consumer goods ex food and autos) and services (led by international travel).

The other revision of note was to personal consumption expenditures where the Q1 growth was revised down to 0.4% q/q saar from 1.4% in the second estimate and 1.6% in the advance report. The downward revision was entirely in consumption of services with small upward revisions to consumption of goods. The growth of services consumption was lowered markedly to 0.5% from 1.8% in the second estimate and 2.1% in the advance report. The BEA stated that the revision primarily reflected downward revisions to financial services and insurance (led by portfolio management and investment advice), based on newly available and updated data from the U.S. Census Bureau’s Quarterly Services Survey.

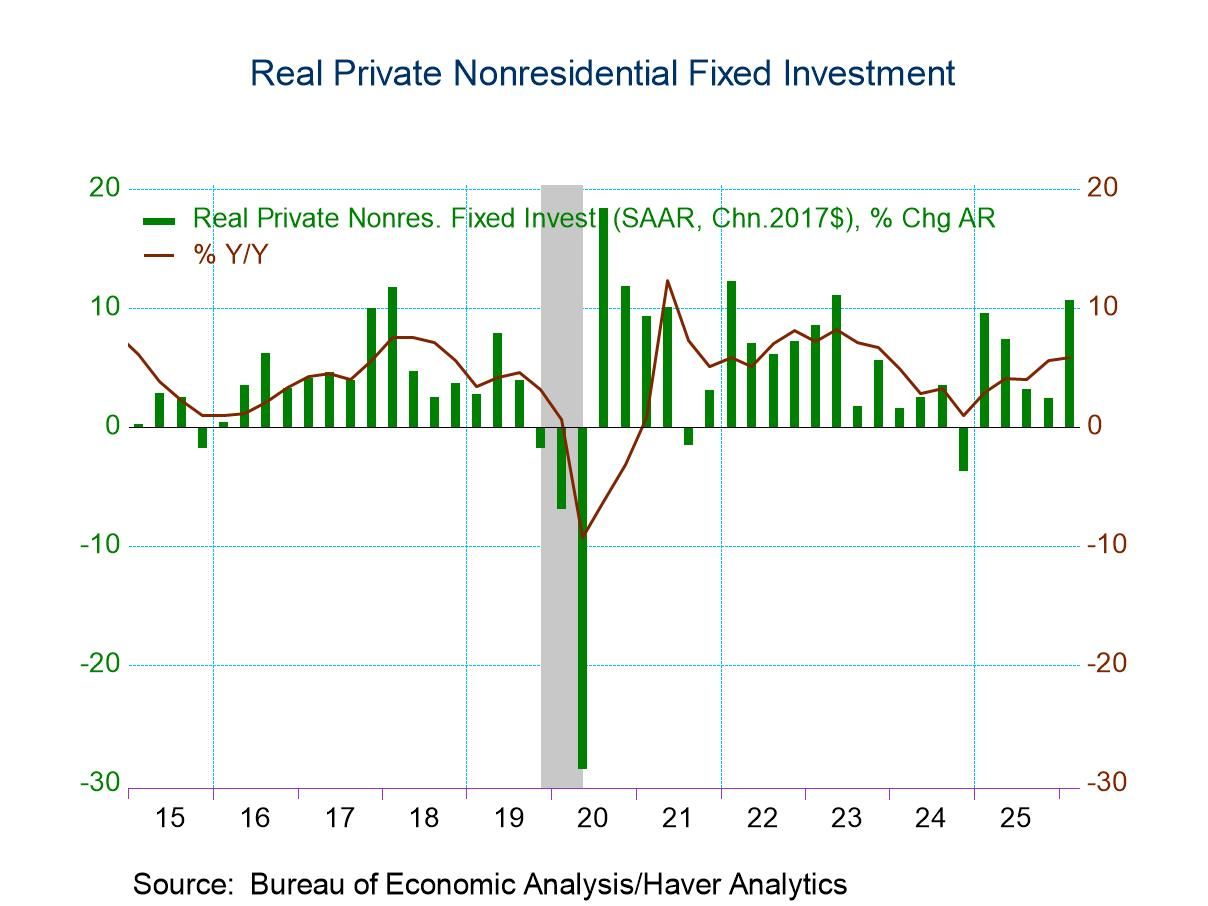

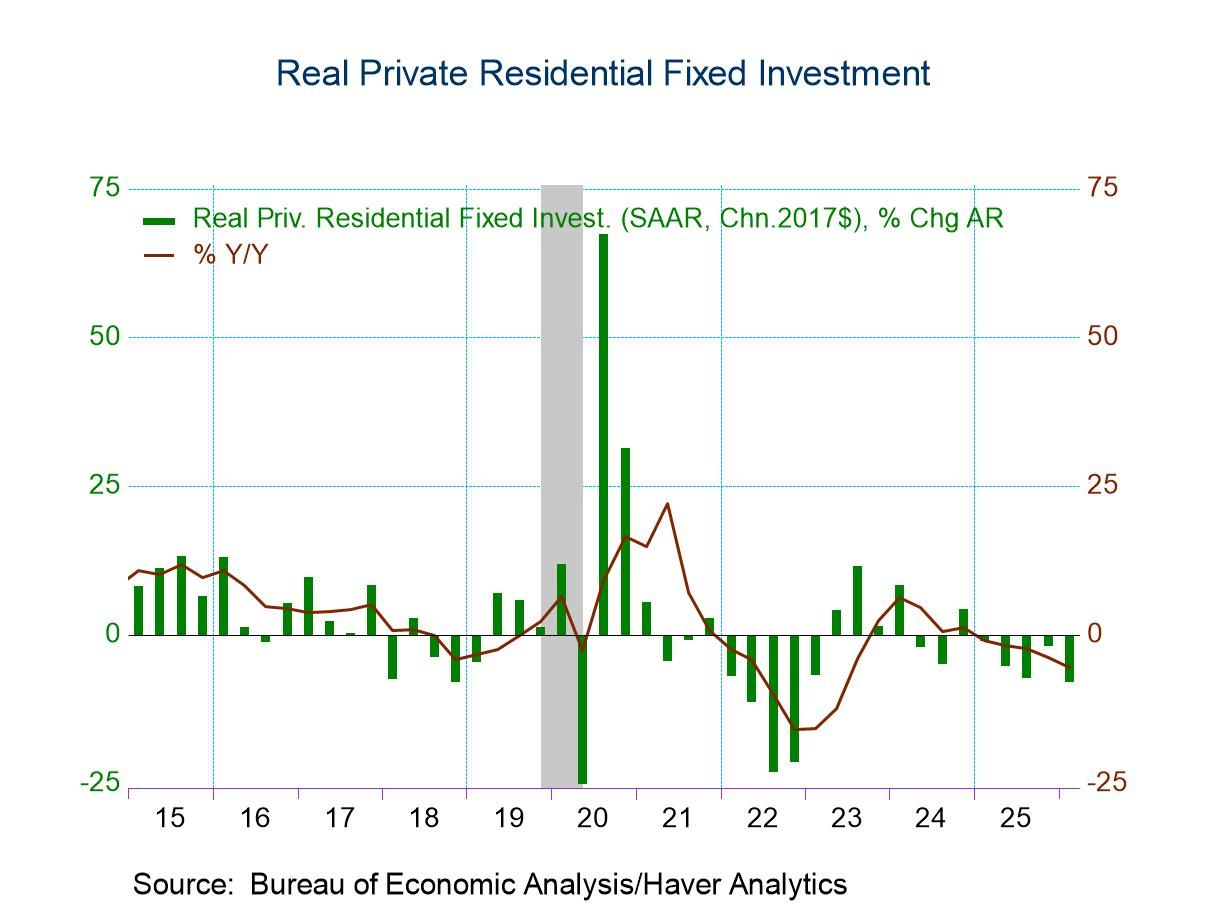

Growth of total fixed investment was little revised to 6.5% q/q saar from 6.4%. This reflected an upward revision to nonresidential fixed investment growth to 10.6% from 10.1% in the second estimate and a downward revision in residential investment growth to -7.8% from -6.3%. Growth of government spending was unrevised at 4.4%. The decline in inventories was revised slightly smaller with inventories adding 0.2%-point to overall growth versus 0.1%-point in the second estimate.

With growth in both imports and personal consumption expenditures being revised down, private domestic demand growth (final sales to private domestic purchasers, a favored gauge of demand by the Federal Reserve) was revised down meaningfully to a still-solid 1.7% q/q saar from 2.4% in the second estimate and 2.5% in the advance report.

The GDP data can be found in Haver’s USECON and USNA databases. USNA contains virtually all of the Bureau of Economic Analysis detail in the national accounts. The Action Economics consensus estimates can be found in AS1REPNA.

Sandy Batten

AuthorMore in Author Profile »Sandy Batten has more than 30 years of experience analyzing industrial economies and financial markets and a wide range of experience across the financial services sector, government, and academia. Before joining Haver Analytics, Sandy was a Vice President and Senior Economist at Citibank; Senior Credit Market Analyst at CDC Investment Management, Managing Director at Bear Stearns, and Executive Director at JPMorgan. In 2008, Sandy was named the most accurate US forecaster by the National Association for Business Economics. He is a member of the New York Forecasters Club, NABE, and the American Economic Association. Prior to his time in the financial services sector, Sandy was a Research Officer at the Federal Reserve Bank of St. Louis, Senior Staff Economist on the President’s Council of Economic Advisors, Deputy Assistant Secretary for Economic Policy at the US Treasury, and Economist at the International Monetary Fund. Sandy has taught economics at St. Louis University, Denison University, and Muskingun College. He has published numerous peer-reviewed articles in a wide range of academic publications. He has a B.A. in economics from the University of Richmond and a M.A. and Ph.D. in economics from The Ohio State University.

More Economy in Brief

Global

Global