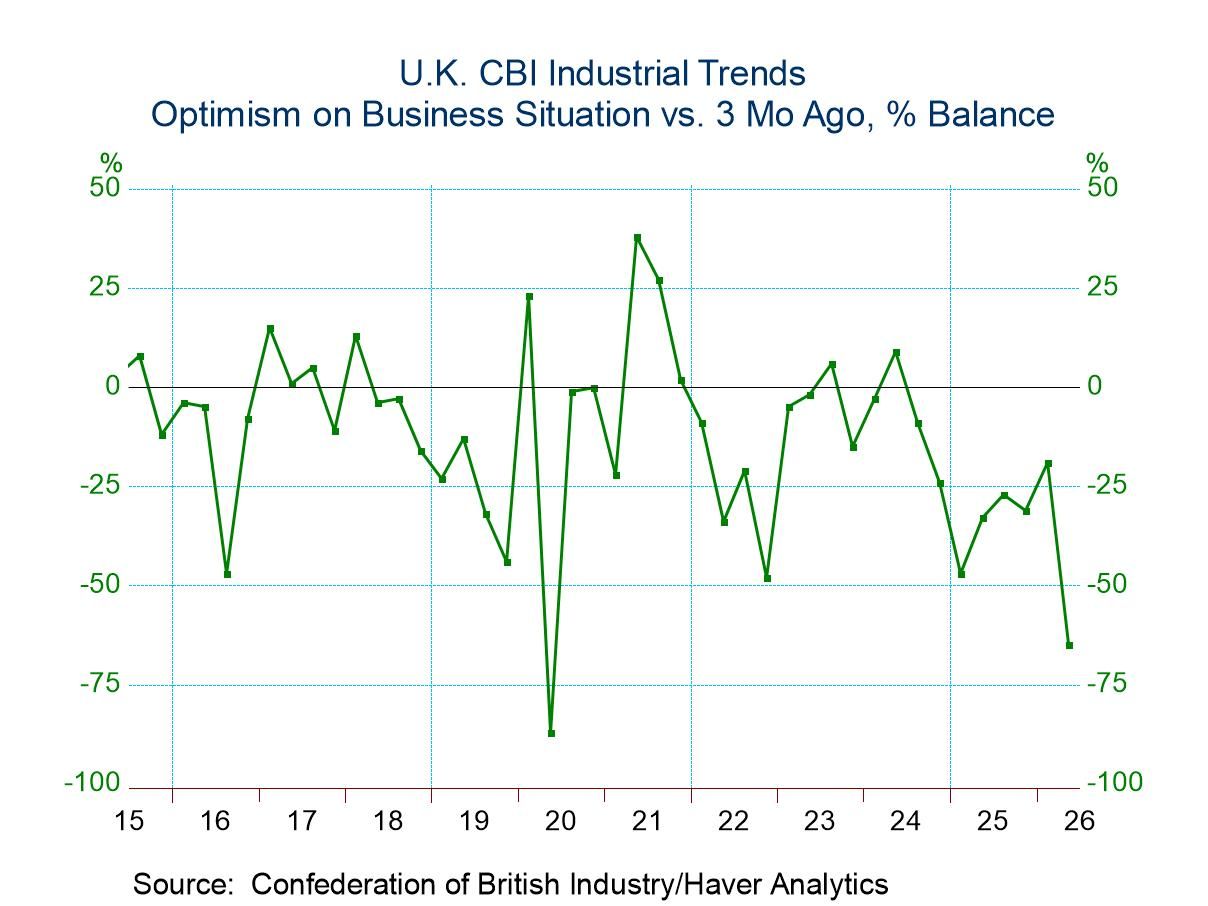

U.K. CBI Industrial Quarterly Survey Weakens

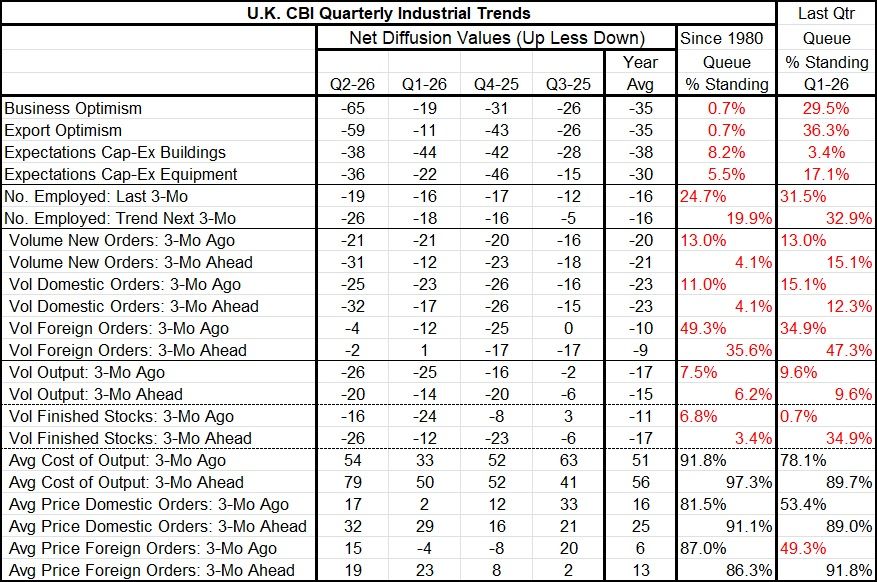

The Confederation of British Industry (CBI) shows business optimism falling sharply in Q2 2026, joined by a drop in export optimism. Expectations for capital goods spending excluding buildings improved slightly on the quarter, with the index reading rising to -38 from -44. Expectations for capital spending excluding equipment fell significantly to -36 in the second quarter from -22 in the first quarter. The two capital spending measures each have rankings below the 20th percentile; for capital spending excluding buildings, the figure is extremely weak.

The number employed over the last three months shows a slight decline to -19 from -16; however looking ahead to the next three months, the decline repeats, falling to -26 from -18 in the first quarter. The rankings for these two metrics are both in the low 30th percentiles.

New order volume for three months ago and three months ahead remain weak, with the three-month ago reading stuck at -21 and the three-month-ahead reading falling from -12 in the first quarter to -31 in the second quarter. The rankings for these two metrics are each at the 15th percentile or lower.

The volume of domestic orders for three months ago edged slightly lower, to -25 from -23; however for three months ahead it weakens more sharply to -32 from -17. Both of these metrics have rankings at the 15th percentile or weaker.

The volume for foreign orders from three months ago improved to -4 from -12. The volume for three months ahead has weakened only slightly, from +1 in the first quarter to -2 in the second quarter. The three-month-ago reading has a 35th percentile ranking, while the three-month-ahead ranking is at its 47th percentile. The foreign sector appears to be carrying some stimulus to the U.K. economy.

The volume of output from three months ago was slightly weaker in the second quarter, while the volume of output for three months ahead is expected to weaken from a -14 reading in Q1 to -20 in Q2. Both metrics have a lower 10th percentile standing.

The average cost of output three months ago rose sharply to an index reading of in the second quarter 54 from 33 in the first quarter. Looking ahead to the next three months, another ratchet up is in progress, to a reading of 79 from 50 in the first quarter. These are suddenly extremely strong readings, with three-months-ago reading at a 78th percentile standing and the three-month-ahead reading at essentially a 90th percentile standing.

The average price for domestic orders three months ago has gone up from an index value of 2 in the first quarter to 17 in the second quarter, while the average price for domestic orders for three months ahead edged up to a reading of +32 from +29 in the first quarter. The three-month-ago reading has a 53rd percentile standing, while the three-month-ahead reading has an 89th percentile standing. Price expectations are hot.

The average price on foreign orders for three months ago rose from -4 in the first quarter to +15 in the second quarter, logging a 49th percentile standing, pretty close to its historic median. The average price for foreign output for three months ahead moved down to +19 from +23 in the first quarter and has a very strong 91.8 percentile standing. The Q/Q pressure eased a bit but remains intense.

The survey also cites factors that are likely to be limiting to output in the three months ahead. The most significant item is a shortage of skilled labor; credit and finance conditions also rank high, and to a lesser extent, the availability of materials and components is a concern. Concerns about inadequate demand are below the median levels of those concerns registered through the history of the survey. Demand is not an issue.

On balance, there is a good deal of pessimism on the outlook, and it's not surprising given the global survey results we have seen from the PMI data and the conditions that exist in the Middle East, with the impeded functioning of traffic through the Strait of Hormuz. Inflation in the U.K. remains high; it's just another factor that the economy will have to deal with as it tries to press ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia