June Housing Starts: Contrasting Movements in Multi-Family and Single-Family

Summary

- Multi-Family starts rebounded from a soft reading in May.

- Single-family activity dipped from upwardly revised levels; softish trend overall.

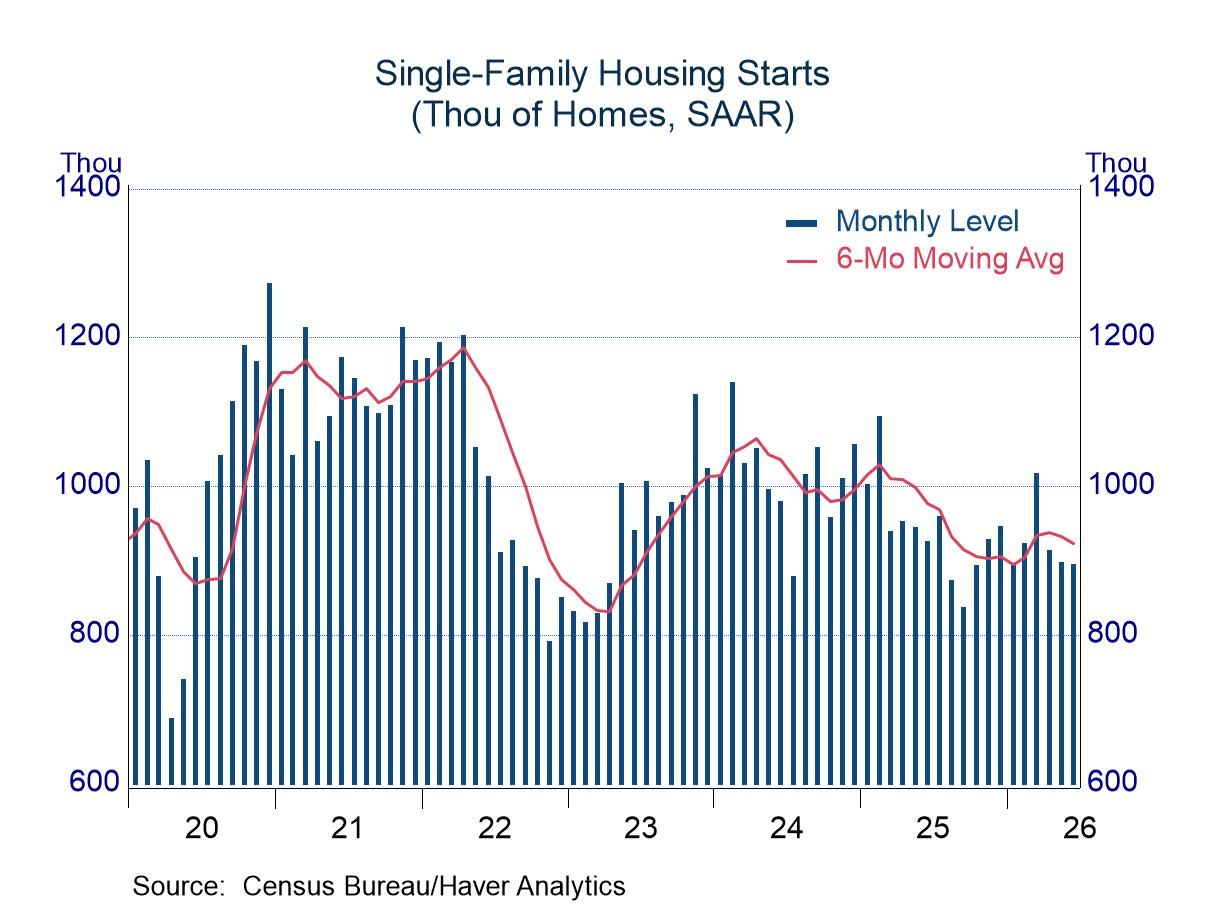

Total housing starts jumped 19.0% in June, but the sharp advance was less impressive than it might appear. The increase reflected a striking gain of 76.2% in the multi-family sector, but the surge followed a soft month in May. Moreover, single-family building lost a bit of ground (off 0.2%).

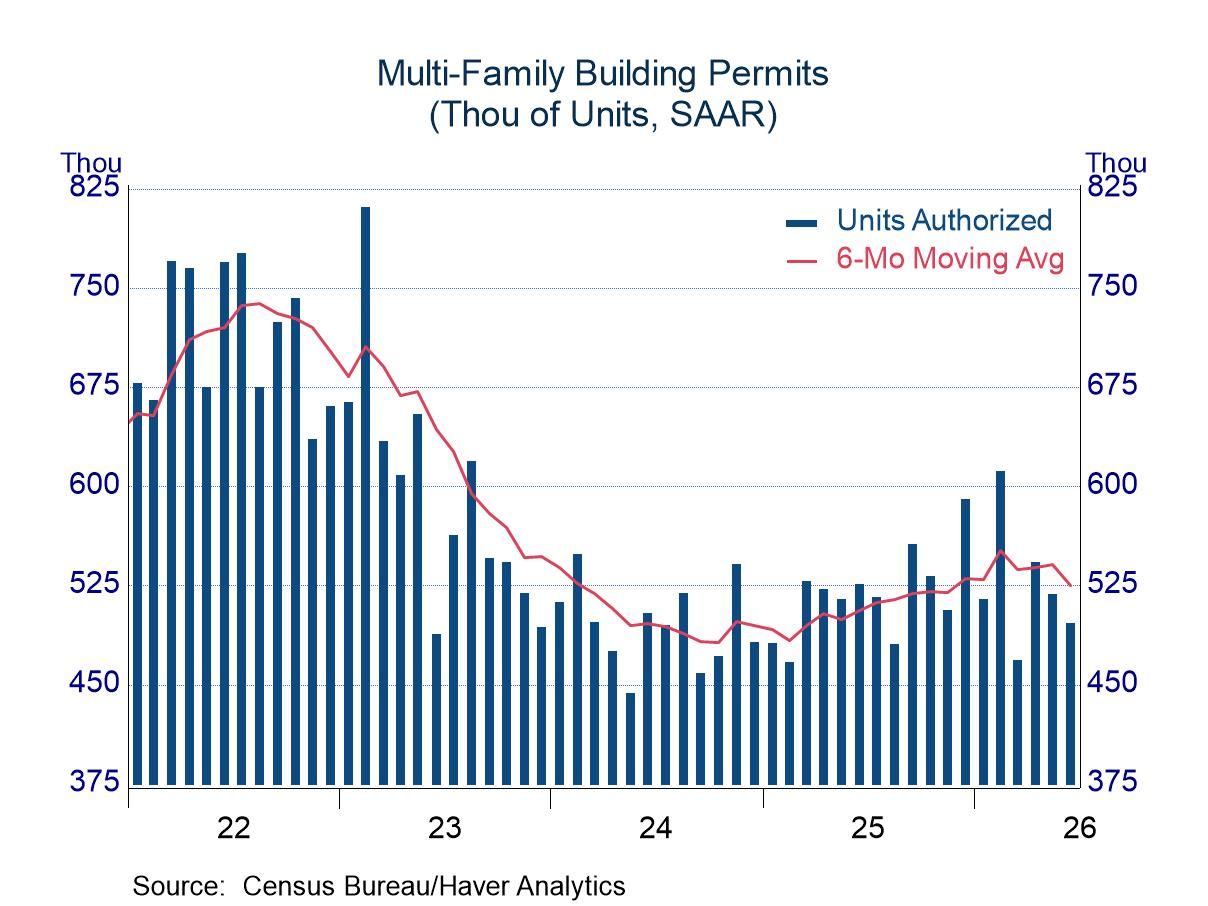

The increase in multi-family starts was the fourth largest in the history of the series (data available from 1959). The change involved a large dose of random volatility, as it followed a drop of 39.6% in the prior month, which pushed the level of multi-family starts to the low end of the recent range. Still, the surge in June moved multi-family starts to the upper end of the range from the current cycle and reinforced the upward trend in multi-family activity.

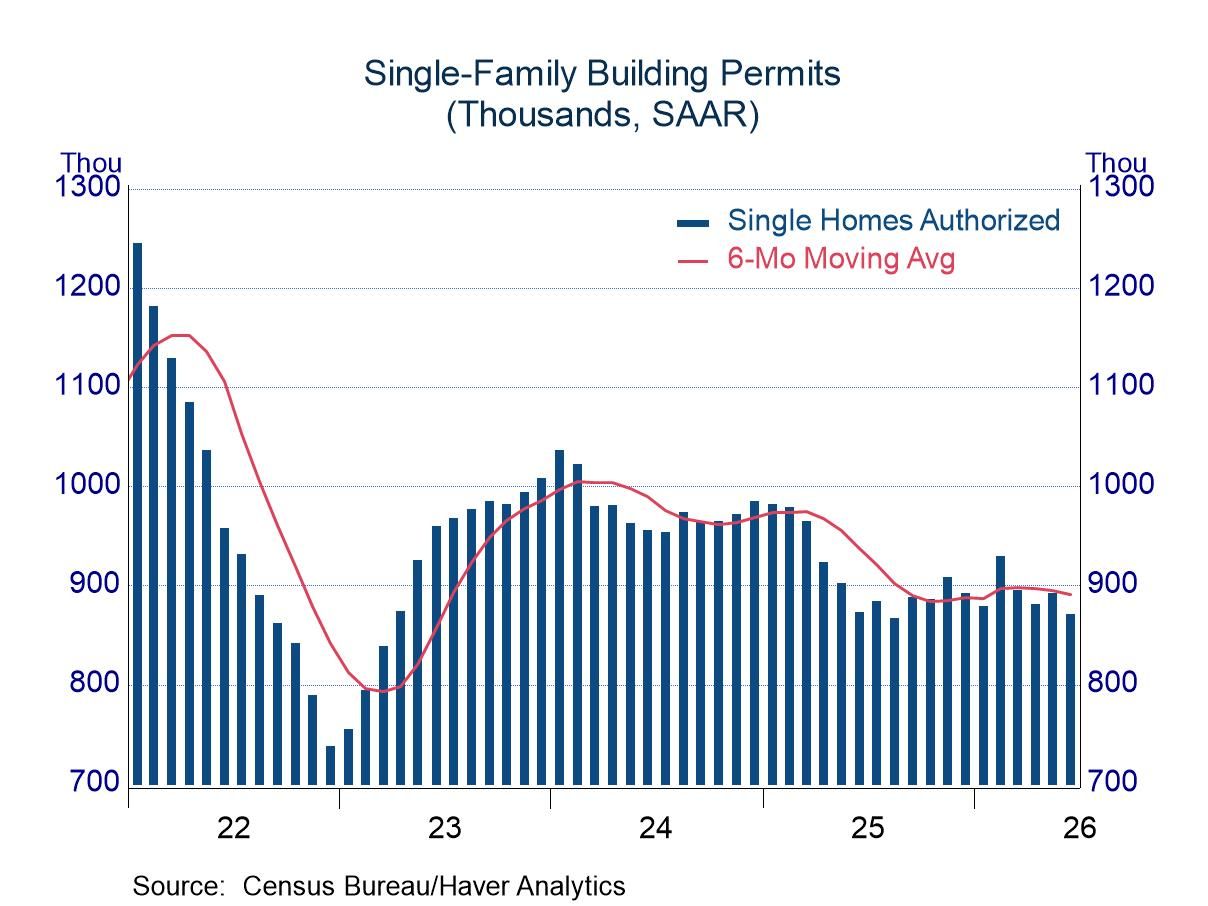

The dip in single-family starts occurred from upwardly revised readings in both April and May (1.7% firmer than previously believed in both months). The revisions, although notable, were not strong enough to have a marked influence on the generally soft performance in the single-family sector. After trending lower during most of 2024 and 2025, single-family building has changed modestly in recent months. The upward revision in April and May gave an upward bump to single-family starts, but the underlying trend is still close to flat.

Building permits are less volatile than starts, and the higher degree of stability usually provides a clearer view of underlying trends. Overall, permits drifted lower during 2024 and 2025 before inching up in the first half of this year. The upward nudge in 2026 primarily reflects planned activity in multi-family building; single-family permits have been tracing a largely sideways trend (charts below).

In general, the housing sector has been soft in the past few years. Activity slowed noticeably in 2022 and 2023 in response to higher interest rates. (Mortgage rates rose from the neighborhood of 3.0% in 2021 to a peak of more than 8.0% in late 2023.) With higher interest rates generating affordability challenges, residential construction has constrained GDP growth in most recent quarters (negative contributions to GDP growth in 12 of the past 17 quarters; an average drag of 0.2 percentage point).

The housing starts and permits figures can be found in Haver’s USECON database. The expectations figure is contained in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief