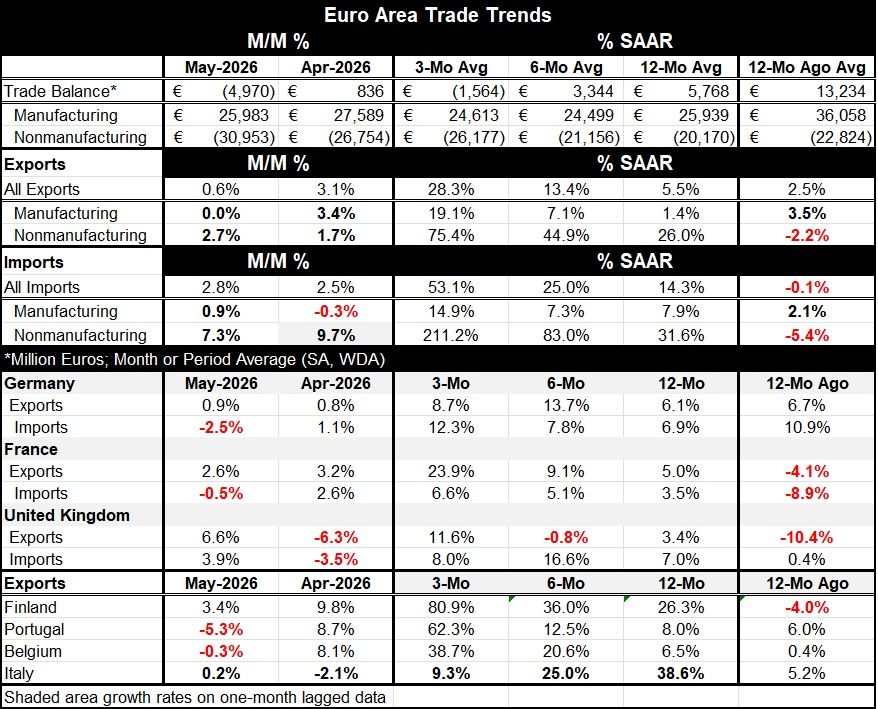

EMU Trade Balance Swings to Deficit in May

Global trade volumes continue to expand Despite military actions around various geopolitical hotspots, war zones, and other geopolitical tensions, plus the imposition of tariffs, World Trade volumes in dry goods have continued to expand significantly since early 2025.

Exports from the European monetary Union have grown over the past year by 5.5%, while imports have surged ahead at a 14.3% annual rate. The growth in trade is driven mostly by nonmanufactured goods, and this is largely a pricing effect as inflation has remained high and oil prices during this period have risen sharply.

The trade balance and its dynamics The euro area trade balance in May slipped into a deficit of €4.97 billion after having a surplus of only €836 million in April. Over the last 12 months, the surplus averaged €5.7 billion per month. We can build up the trade balance several different ways to explain it. One way to understand it is that there are certain tensions between manufactured and nonmanufactured goods. The balance on manufactured goods trade 12 months ago was an average €36 billion over the previous 12 months, whereas it's currently showing a 12-month average that has fallen to a €26 billion surplus. However, all of the trend changes appear to have occurred between a year ago and earlier this past year, since the 12-month, six-month, and three-month averages, as well as the stand-alone reading for May, show manufacturing surpluses in the neighborhood of €25 billion. For nonmanufactured goods, 12 months ago the average monthly deficit was €22.8 billion, whereas over the last 12 months the average has been about €20.2 billion; that's a slightly smaller deficit. The sequential nonmanufacturing deficit balance, however, crept up through the course of the last 12 months, and in May it registered a €30.95 billion deficit. Erosion in the deficit position of the euro area is significantly based on an increased deficit in nonmanufactured goods.

Aggregate trade flows show exports accelerating from 12-months to six-months to three-months, with the same progression for imports, except that the import growth rates are substantially higher than for exports. Exports of manufactured goods accelerate from 12-months to six-months to three-months, but the exports of nonmanufactured goods are stronger and accelerate much more on that same timeline. Imports show manufactured goods in a relatively weak acceleration mode from 12-months to three-months as well. For nonmanufactured goods, the import growth rates post incredible results; they're extremely strong. This, of course, is mostly a pricing effect reflecting the impact of oil prices.

The table includes a few bilateral comparisons. Germany shows accelerating imports, and while there's steady growth in exports, they're not accelerating the same as imports. For France, exports accelerate quite strongly while imports accelerated, but with much less vigor. Much of this has to do with France’s greater reliance on nuclear power as France gets about 65% or more of its electricity from nuclear energy compared to only 11% for Germany, which has cut back and is transitioning away from nuclear power, making it more dependence on other energy sources and boosting energy imports. U.K. exports and imports are both showing growth, but there is no clear trend.

The table also presents export data for five European nations. Exports accelerate for each of them except for Italy, where exports are in a markedly different and decelerating pattern.

On balance, trade trends are in flux although manufacturing trends seem to be quite stable. Volatile oil and other commodity prices are causing severe swings in trade flows across Europe and certainly globally as well. With the situation in the Strait of Hormuz still unresolved, the outlook for trade will continue to expect volatility.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief