HICP Detail in EMU Shows Inflation Lurking

Inflation in EMU The recent inflation data in the European Monetary Union is emblematic of the kind of issues that central banks typically have to deal with. Casual central bank observers think of central banks as “leaning against the wind,” meaning that they raise rates when inflation is high and then cut rates when the economy gets weak. Indeed, this is largely what central banks do. However, they also try to be anticipatory when they can, seeking to get ahead of surges in inflation and periods when the economy is going to weaken. It's very hard to forecast those shifts in the best of circumstances, and so a great deal of the judgment that central banks form comes from the near-term trends, even though central banks are aware that the most recent data can also be some of the most volatile and prone to revision. With these sorts of caveats, we look at the recent inflation data from the European Monetary Union, and we see less than straightforward trends.

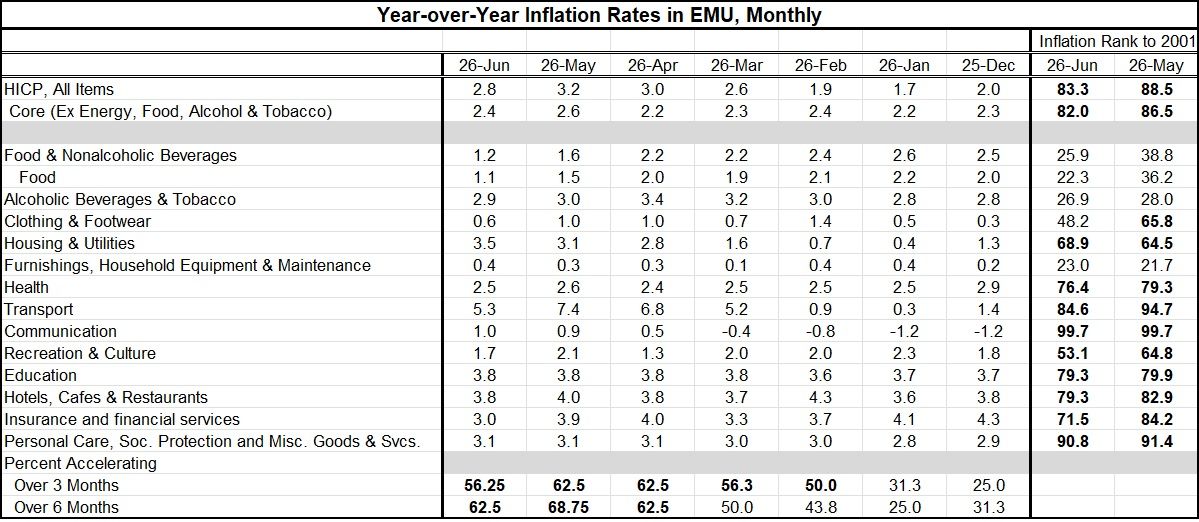

At its last meeting, the European Central Bank got out in front of events and started raising rates ahead of any action by the Federal Reserve. In June, its year-over-year HICP and core HICP rates both decelerated compared to their May values, with the headline easing to 2.8% from 3.2% and the core to 2.4% from 2.6%. Having inflation rates move in the opposite direction of policy, even in the short run, can create rough sledding for a central bank that is, in any event, trying to look at the broader trend rather than the most recent wiggle in the inflation rate.

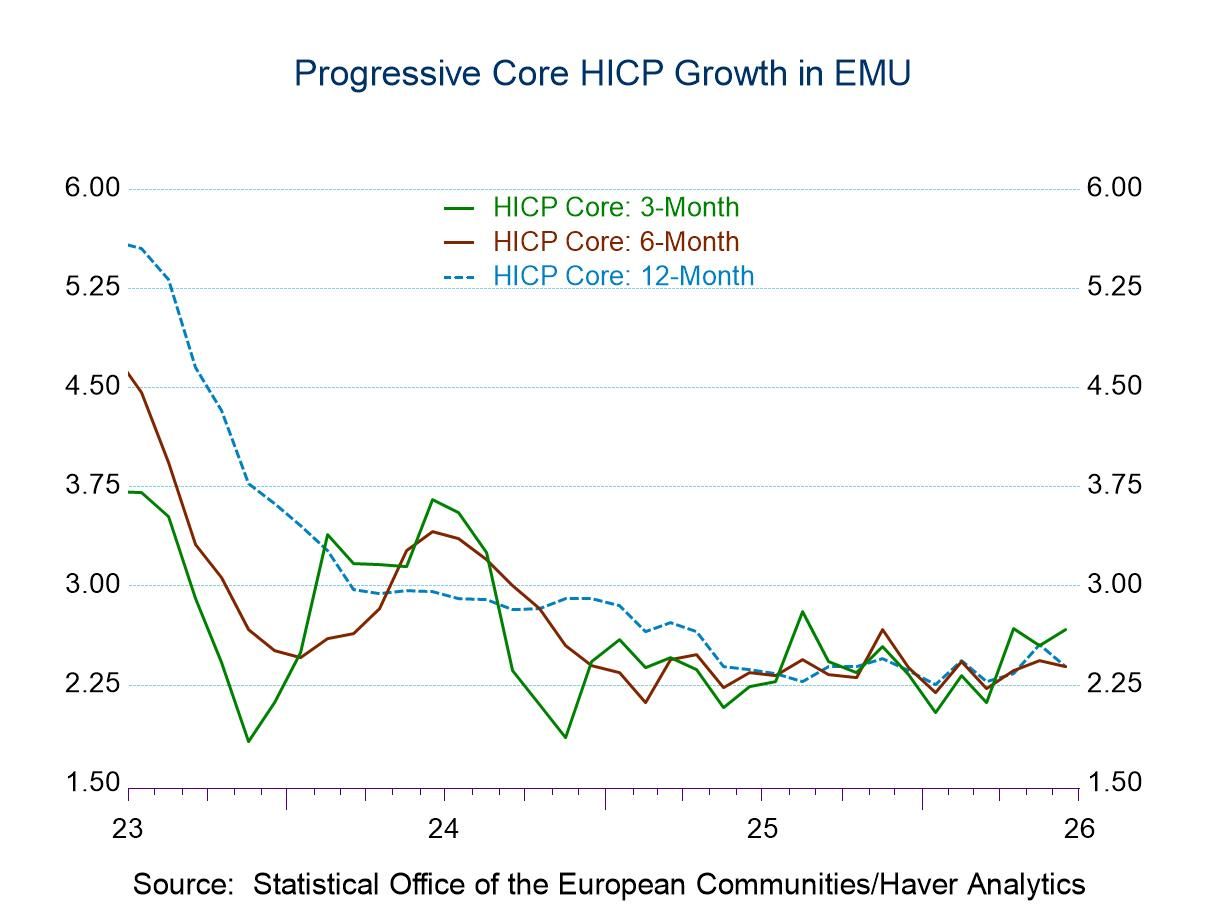

The good, the bad, and the unexpected If we go back to December, we see the HICP in the monetary union at 2%, followed by 1.7% in January and 1.9% in February. At that point, things seemed to be well in hand. The problem was that the core inflation rate in December was 2.3%; while it fell to 2.2% in January, it popped back up to 2.4% in February. So, February was one of those uncomfortable months where both the headline and core rates were popping up, but the headline rate was still below the 2% target that the ECB seeks to attain. After February, of course, the world changed; the war in Iran spiked up oil prices and that's when inflation rate in the monetary union rose to 2.6% in March, 3% in April, and 3.2% in May. June inflation has backed down from those higher rates of change; however, conditions in the Middle East that had prompted some release of air from the inflation balloon in June have reversed, and so, the outlook once again is for oil prices to remain high and for inflation to remain troublesome.

Inflation still percolates At the bottom of the table, I show the percentage of categories with inflation accelerating over three months, and since February, that percentage is over 50% in each month. The percentage of categories with inflation accelerating over six months strings out to three months in a row. The decision by the ECB to raise rates is entirely understandable given these trends. In addition, and perhaps less tethered to any particular monetary rule, included in the right-hand column, the inflation ranking in June is compared to data back to the year 2001, a roughly 25-year period. Over this timeline, the headline HICP ranks in the 83rd percentile and the core rate in the 82nd percentile. In both cases, we're looking at inflation being higher only 17% or 18% of the time during this span, which once again marks this as a strong inflation period.

Haunted by their legacy In addition, central banks are coming off a period where they had missed their inflation targets quite a lot. While the ECB had been able to land its inflation rate inside its target zone for a while, the Federal Reserve has not been able to accomplish that at all; the Bank of England is still struggling with that, and the Bank of Japan, after dueling with deflation, now has an excess of inflation. Globally, there is this environment that's looking a lot more fundamentally inflationary rather than disinflationary and certainly not deflationary, thanks to oil and war.

Complex circumstances but a clear objective Central banks certainly have to set their policies for their own domestic conditions, but global conditions do matter. The war or warlike conditions continue in Ukraine and Iran. Although the United States and Israel were able to deal Iran a potentially crippling blow to its nuclear operations, Iran tenaciously clings to its ambition to eventually nuclearize and it has added to that a claim to control traffic at the Strait of Hormuz, which most countries find to be unacceptable and which is also in violation of international law. At the same time, Ukraine has been able to penetrate Russian defenses to make strikes deep into Russia against Russian energy resources, so the war in Ukraine is going a lot better for the Ukrainians, although it also is putting the energy sector under greater peril and pressure. These days circumstances are so complicated that sometimes even good news can play out as bad news. One might think that after the evisceration that Iran got in the hands of the United States and Israel, it would be more contrite. But it has not and has only hardened its resistance. Iran is using its advantage over a peculiar piece of geography in the Strait of Hormuz to try to become a global power despite having been stripped of almost all of its military might. As it turns out, the Strait of Hormuz is so delicate that it doesn't take much for Iran to be able to create a good deal of chaos with tanker traffic using missiles, drones, and mines. All of this makes the inflation outlook so much harder to pin down. Monetary policy should not require central bankers to be military strategists, but we have, in some sense, been relegated to that sort of situation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief