Global| Jun 23 2026

Global| Jun 23 2026S&P PMIs in June Firm

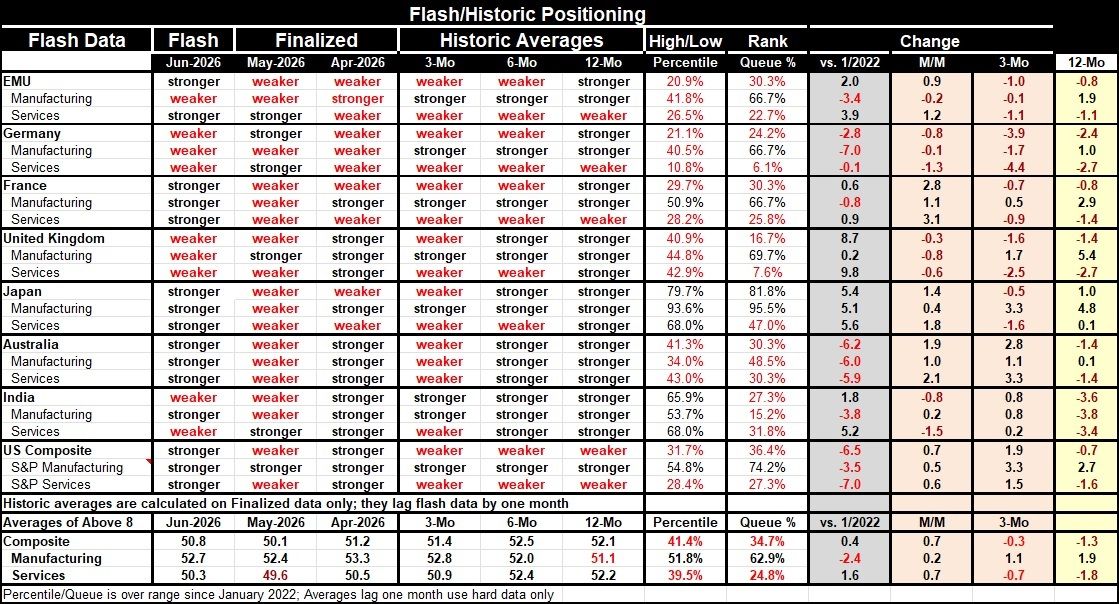

PMIs in June mark some progress The PMI report from S&P shows modest firming in conditions in June, even with the Middle East situation unresolved.

Monthly: The median reading for the 8 reporting countries or regions rose to 50.8 in June from 50.1 in May. Manufacturing improved to 52.7 from 52.4, while the services reading rose to 50.3 from 49.6, leaving a month of mild contraction behind.

Most show June improvement: Most countries or regions improved in June; the exceptions were Germany, the United Kingdom, and India, which were weaker. India was dragged down by a weaker service sector reading in June; the U.K. and Germany showed weakening conditions across the board for the composite index, the manufacturing sector, and services. On the other side of the coin, France, Japan, Australia, and the U.S. all showed improvement in each of three sectors: the composite, manufacturing, and services, in June compared to May.

Sequentially still mixed: The broader sequential readings show ongoing weakness, but these are derived from hard data and lag the monthly observations in the table that include preliminary flash estimates. All the composite readings weakened based on three-month averages except for India. However, seven of eight reporting areas showed improvement in manufacturing over three months compared to six months; the exception was Australia. Over six months, conditions are mixed, with four composite readings weaker compared to 12 months and with four stronger. However, over six months, all eight manufacturing sectors improved compared to 12 months. The 12-month readings are consistently stronger than their readings of 12 months ago. The only composite that's weaker is the U.S., while the services sectors in the monetary union, Germany, France, and the U.S. are weaker than they were 12 months ago.

Standings are weak: The queue percentile standings evaluate the current diffusion index in June compared to where it has been since January 2022, a period of about 4½ years. The queue standings show weakness up and down the line, with the exception of the manufacturing sector; that has the standing above its historic median in the monetary union, Germany, France, the U.K., the U.S., and Japan. Only Australia and India show manufacturing sectors whose current monthly standings are below their medians of the last 4½ years. In addition, Japan has a strong composite reading at its 81st percentile. Overall, the services sectors are weak and below their 50% standing every place, and below that mark by a large margin, except for Japan, where the services sector has a 47th percentile standing, only a few ticks below its median.

Summing up: A glimmer of hope but still a lot of weakness Manufacturing is stronger sequentially over three months, six months, and 12 months for every reporter except for Australia over three months. The rest of the report is not very impressive. There is some rebound in June, but here we're talking about volatile monthly data. The services sectors still show sequential weakness over 12 months, six months, and three months in the European Monetary Union, Germany, France, and the U.S. The U.K. and Japan showed three-month and six-month weakness as well. That’s too much weakness in the key job creation sector to think that this report is a positive signal.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief