Revised Productivity: No adjustment to Robust Growth in Q3

Summary

- Strong growth in output with little increase in labor input reinforced a firm underlying trend in productivity.

- Efficiency gains in Q3 more than offset growth in labor compensation.

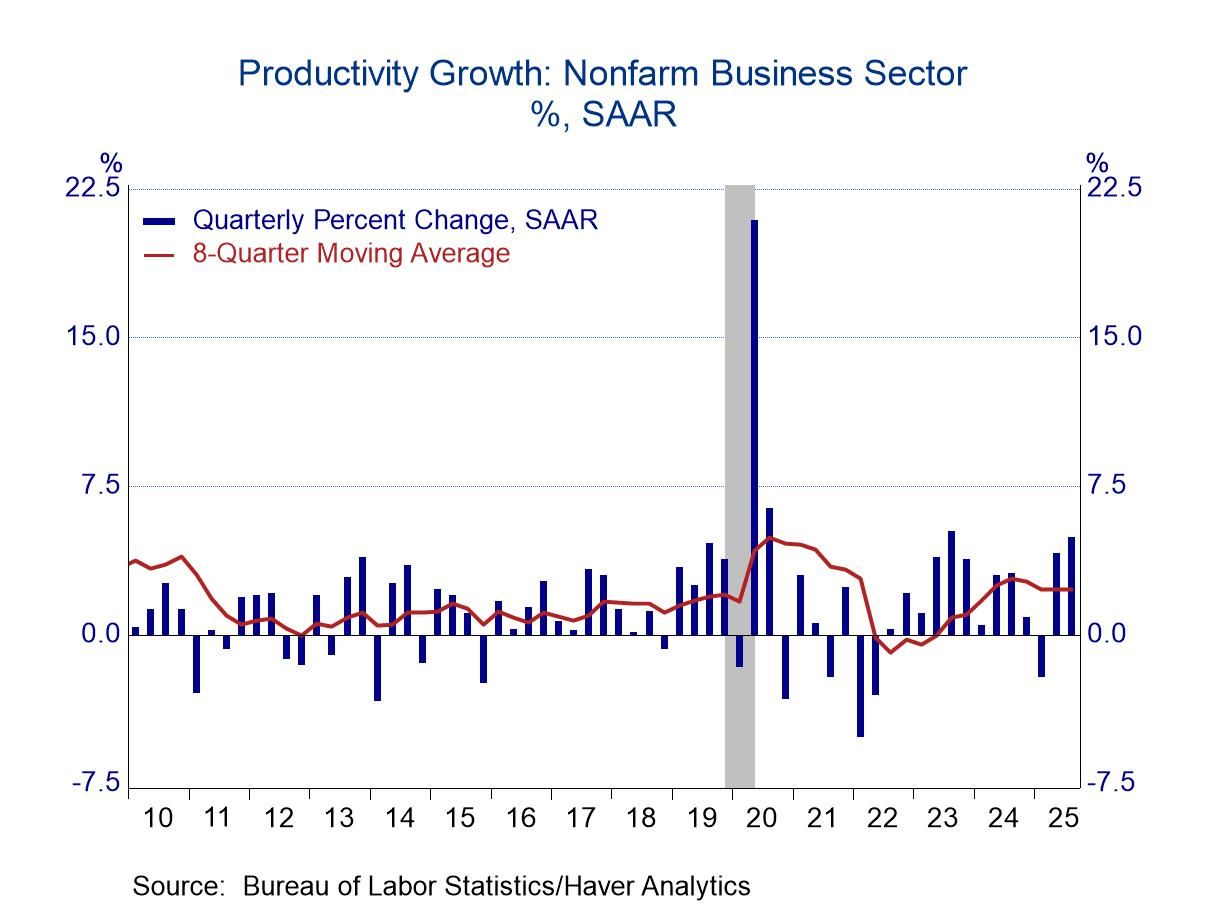

Revised data show no adjustment to the initial estimate of 4.9% growth in labor productivity during the third quarter (nonfarm business sector). This strong showing reflected a robust advance in output (5.4%) with little increase in labor input (0.5%).

Productivity figures often swing widely from quarter-to-quarter, and thus, quarterly observations should be interpreted cautiously. In this case, though, the strong results continued a pattern of generally firm increases that have been evident since late 2022. In the chart above, the 8-quarter moving average (to smooth volatility) shows stronger results than those seem before the pandemic. Average compound productivity growth from the end of 2022 to the present totaled 2.6%, up considerably from the average of 1.1 percent in the 2013-18 period.

The chart shows a jump in productivity in 2020-21. However, this gain probably reflects emergency measures adopted by businesses to survive during the Covid pandemic rather than genuine gains in efficiency, although lessons might have been learned that added momentum in subsequent quarters.

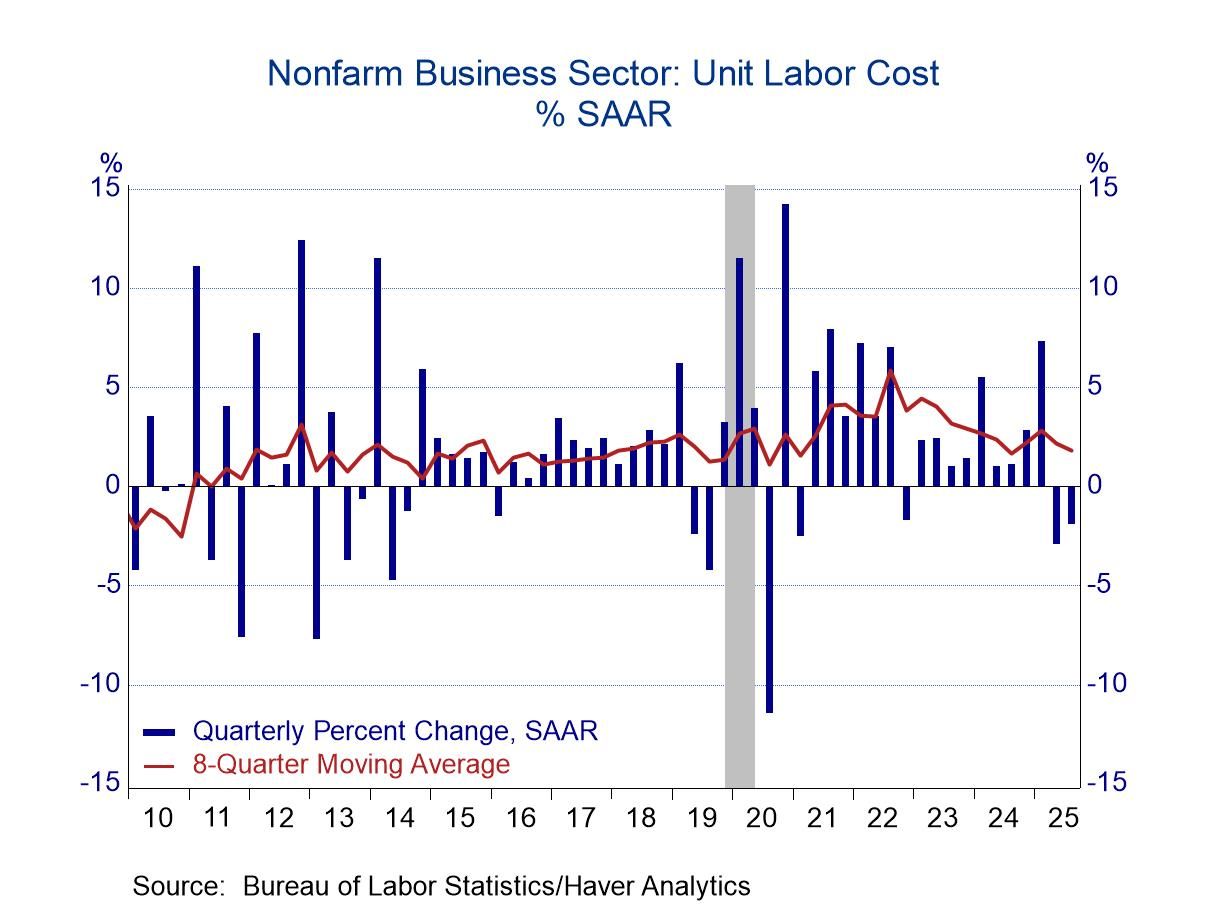

Productivity is a key factor in an economy’s inflation environment, as healthy efficiency gains allow businesses to absorb labor costs without raising prices. With strong gains in productivity, unit labor costs (labor compensation adjusted for productivity) have settled recently. Indeed, unit labor costs have declined in the past two quarters and the latest reading on the 8-quarter moving average totaled only 1.8%, easily consistent with the Federal Reserve’s inflation target of 2.0%.

The productivity and labor cost data are available in Haver’s USECON database. The Action Economics expectations figures are in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global