Q1 Current Account: Modest Slippage in Early 2026

Summary

- Improvement in the trade balance offset by weaker net investment income.

- Annual revision showed wider deficit in 2025.

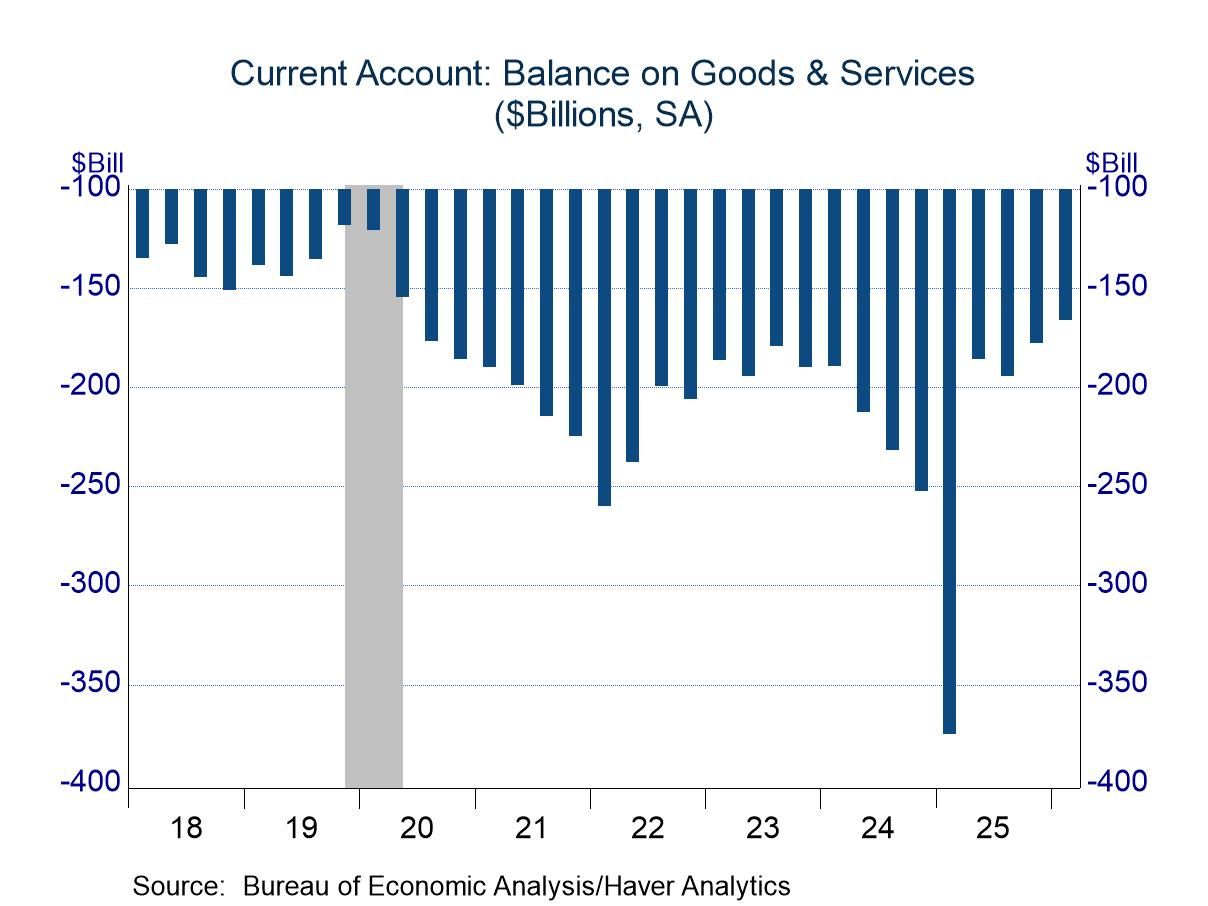

The US current account balance, which consists of international trade and income flows, deteriorated slightly in the first quarter, moving to a deficit of $226.8 billion versus a shortfall of $221.1 billion in the fourth quarter of last year. Trade flows moved slightly in favor of the US, as the deficit narrowed by $11.6 billion to $165.8 billion, with trade in both goods and services contributing to the improvement. The latest reading on the trade deficit was among the best of the post-pandemic period.

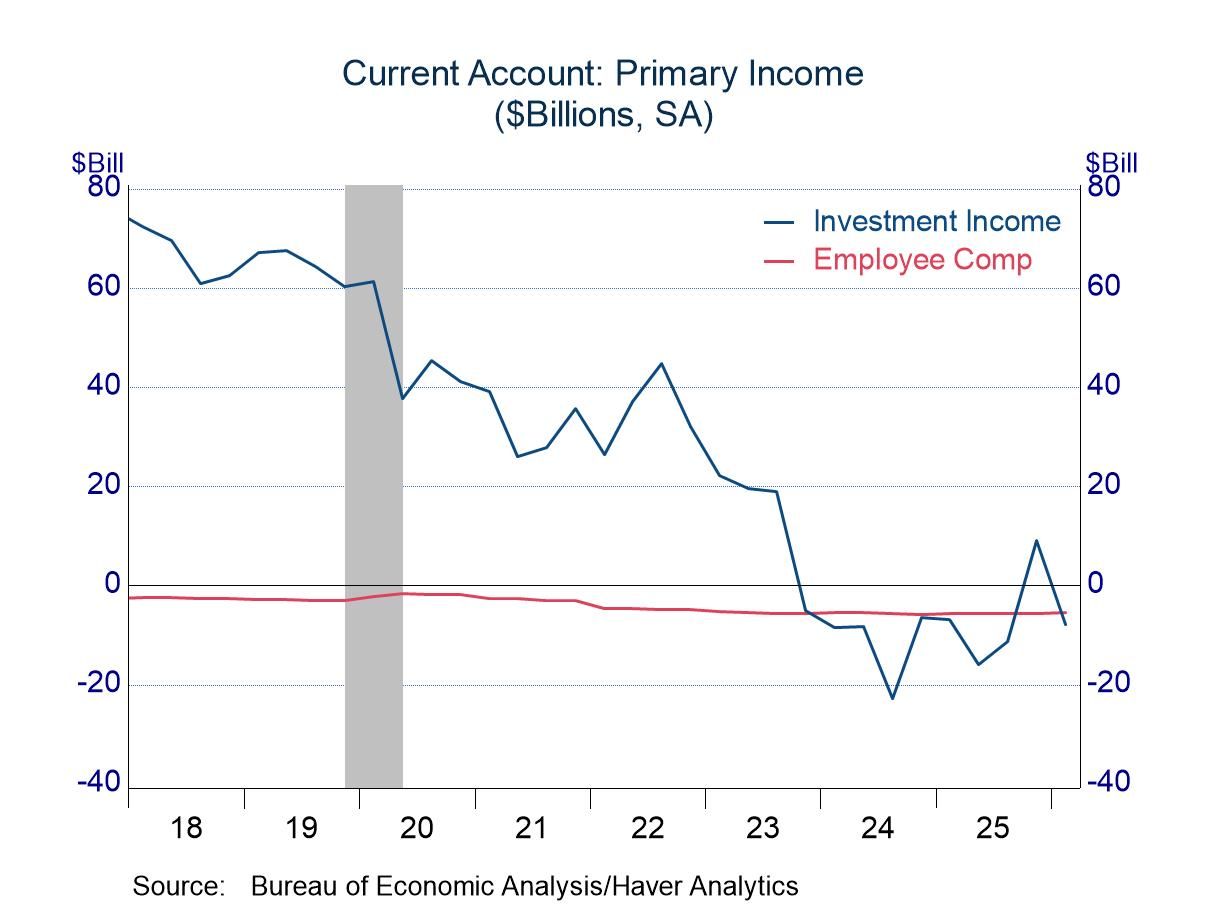

The improvement in trade was more than offset by softening in both primary income and secondary income. Primary income consists of net receipts of both investment income and employee compensation, with net flows defined as receipts of US residents from abroad less US payments to residents in foreign countries. Net investment income is by far the larger of the two components, and it accounted for nearly all of the slippage in primary income, dropping $17.0 billion to -$7.8 billion. The shift pushed net investment income back into negative territory after a quarter in the plus column (chart, lower left). Employee compensation rose, but the change was less than 0.1%.

Secondary income consists largely of transfer payments (payments made without receiving something of economic value in return). Examples include personal remittances (foreign workers sending funds to families in their home country), charitable donations, taxes, fines, and penalties. Payments made by US residents easily exceed payments received, leaving a regular deficit in secondary income. This component of the current account was essentially unchanged in Q1.

Annual revisions to the current account were notable, as both the trade balance and the balance on primary income were revised to show deeper deficits. The trade deficit for all of 2025 now totals $294.3 billion versus a previous estimate of $279.0 billion. Primary income now shows a deficit of $11.9 billion versus a surplus of $3.2 billion.

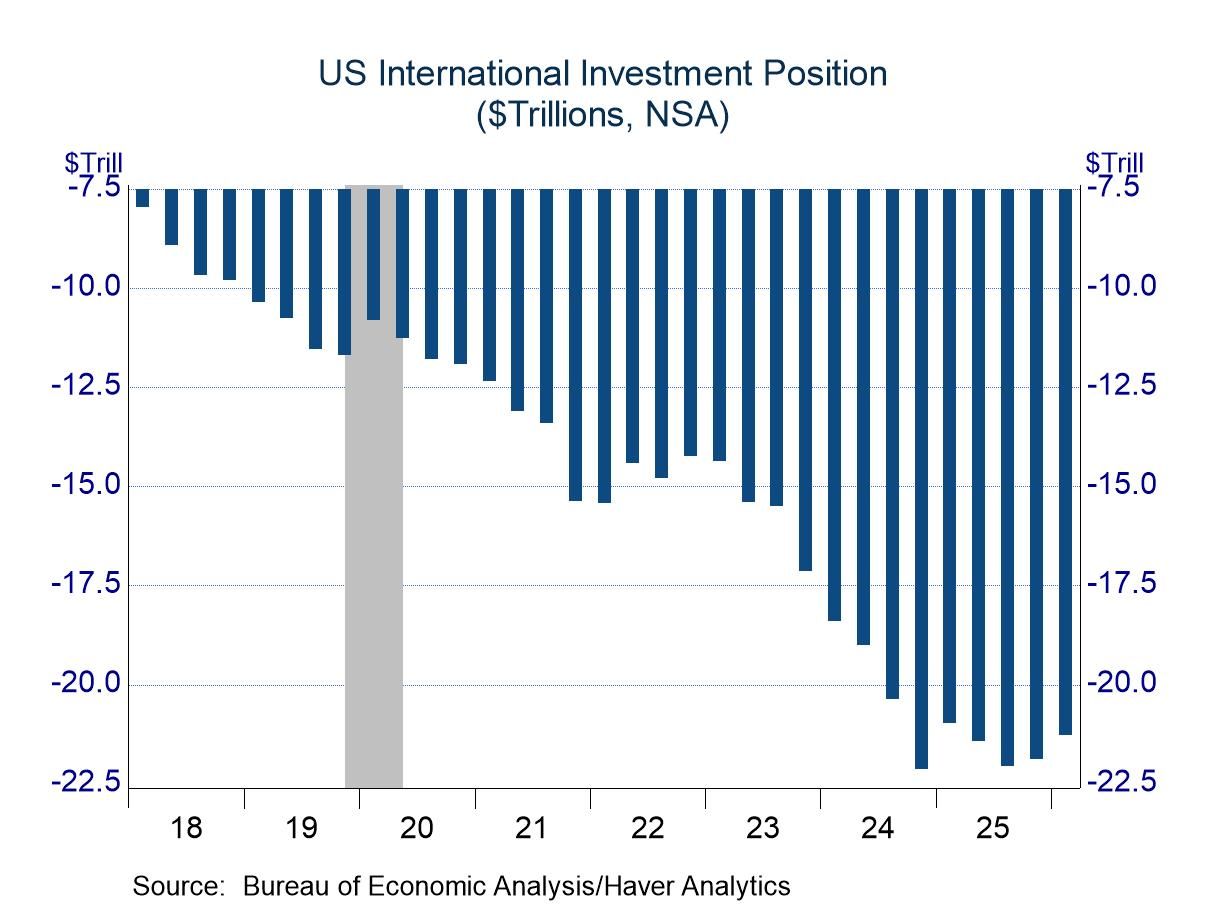

The shift to a deficit position in primary income is not shocking, as positive readings on average in 2025 (and prior years) were surprising in light of the international investment position of the US. Foreign investors hold far larger amounts of US assets than US investors hold of foreign assets (chart, lower right). That is, the US has a deficit in investment holdings. However, despite the differential in asset holdings, US investors typically earned higher rates of return on their foreign investments than foreigners earned on their US investments. Although the gap in asset holdings has been large, higher returns earned by US investors left net positive investment income. Revised data now suggest that the net international investment position of the US has slipped to such a degree that higher rates of return will no longer offset the differential in asset holdings. Positive quarters might be apparent at times (such as 2025-Q4), but net investment income (and primary income in total) will probably be negative in quarters ahead.

Balance of Payments data are in Haver’s USINT database, with summaries available in USECON. The expectations figure is in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

Global

Global