Personal Income, Consumption, and Prices in May

Summary

- Energy prices rose sharply for the third consecutive month; core prices were unsettling as well.

- A jump in nominal income translated to a modest advance in real terms, allowing consumers to remain reasonably active.

The price index for personal consumption expenditures rose 0.4% in May, although the measure almost rounded up to 0.5% (0.4498%). May marked the sixth consecutive month with headline prices increasing 0.3% or more. This series of changes has pulled the year-over-year inflation rate to 4.1%, up from 2.3% just over one year ago (April 2025). Energy prices, of course, have been the most important factor behind the acceleration in inflation, and they remained an issue in May, increasing 4.0% after advances of 3.9% and 11.6% in the prior two months. Food prices have moved erratically in the past year, with jumps and lulls leaving an average monthly increase of 0.2%. The noise was evident in recent months, with food prices increasing only 0.1% in May after a jump of 0.5% in April.

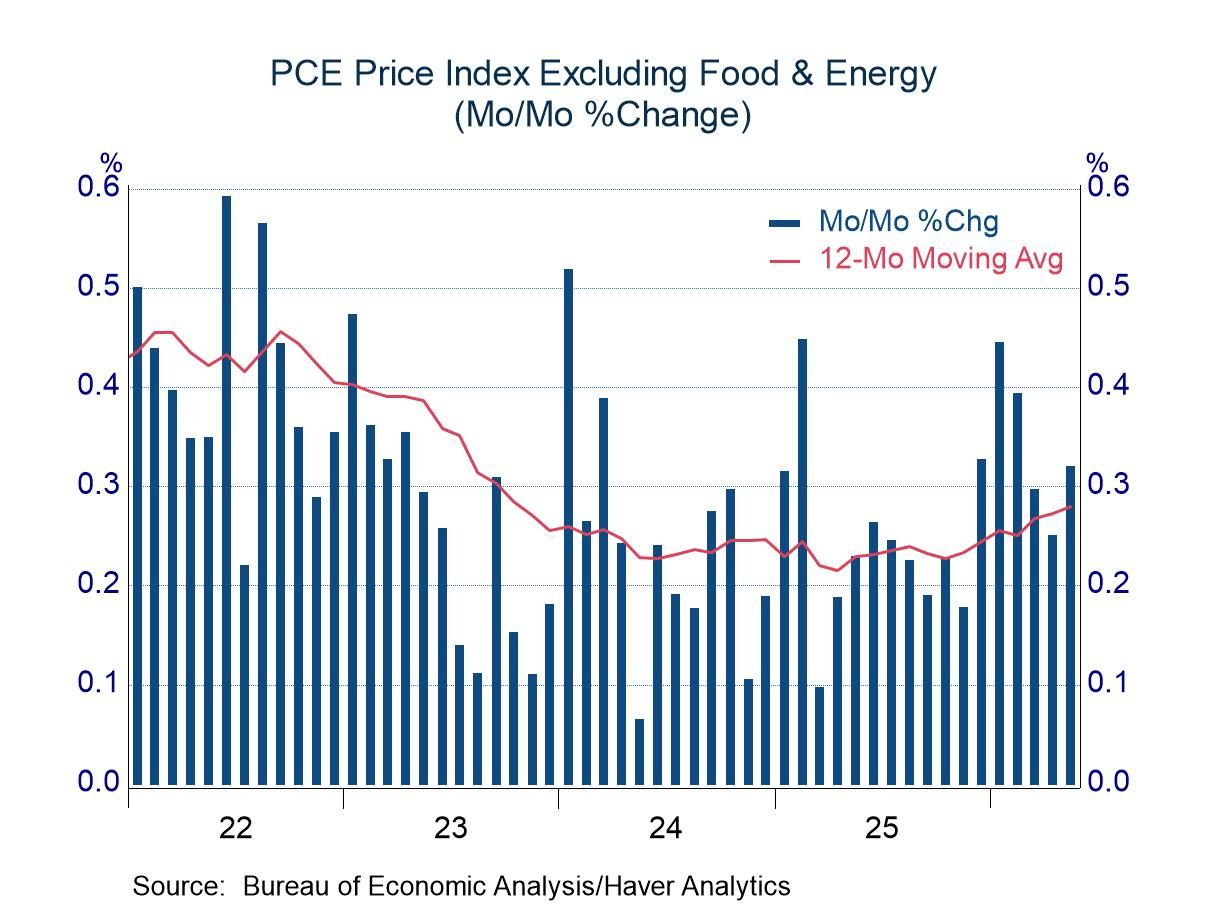

Core prices also have contributed to the pickup in inflation. After averaging monthly increases of 0.24% during 2025, core prices have increased at an average rate of 0.34% so far this year. The year-over-year increase in core inflation totaled 3.4% in May, up from a recent low of 2.6% in April of last year. Both the headline and core inflation rates are uncomfortably above the Federal Reserve’s target of 2.0%.

Total personal income rose briskly in May (0.7%). A surge in farm income played an important role (up 125% month-to-month, most likely reflecting government support payments), but nominal results also were firm elsewhere (up 0.5% ex farm income). Inflation reduced the purchasing power of this income gain, but aggregate income still advanced slightly in real terms (0.2%).

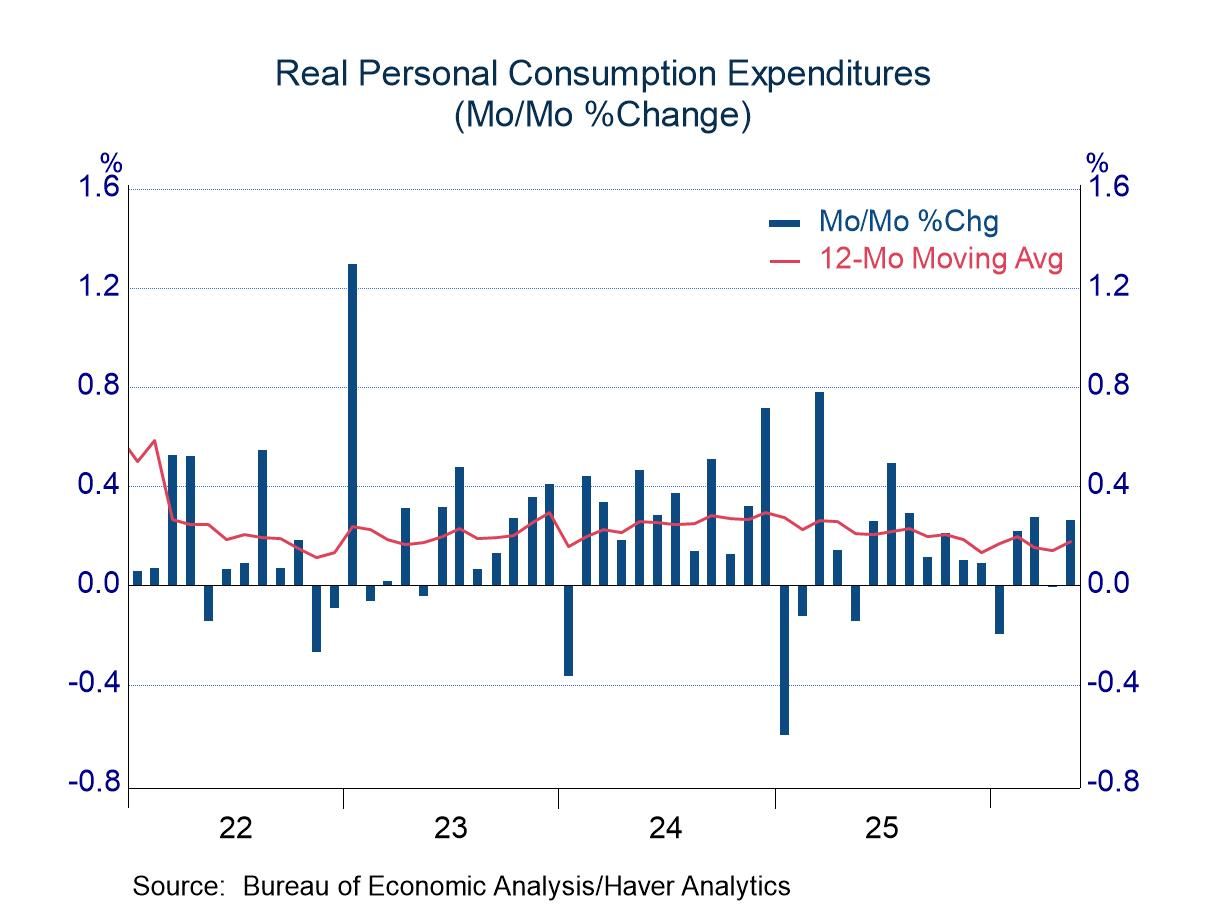

Given the recent surge in energy-driven inflation, May marked only the second monthly increase in real income so far this year. Tight budgets have dampened consumer spending, but individuals have not pulled to the sidelines. Real consumption expenditures rose 0.5% (annual rate) in the first quarter, and results for April and May suggest that real PCE is on track to increase 1.5% to 2.0% in the second quarter.

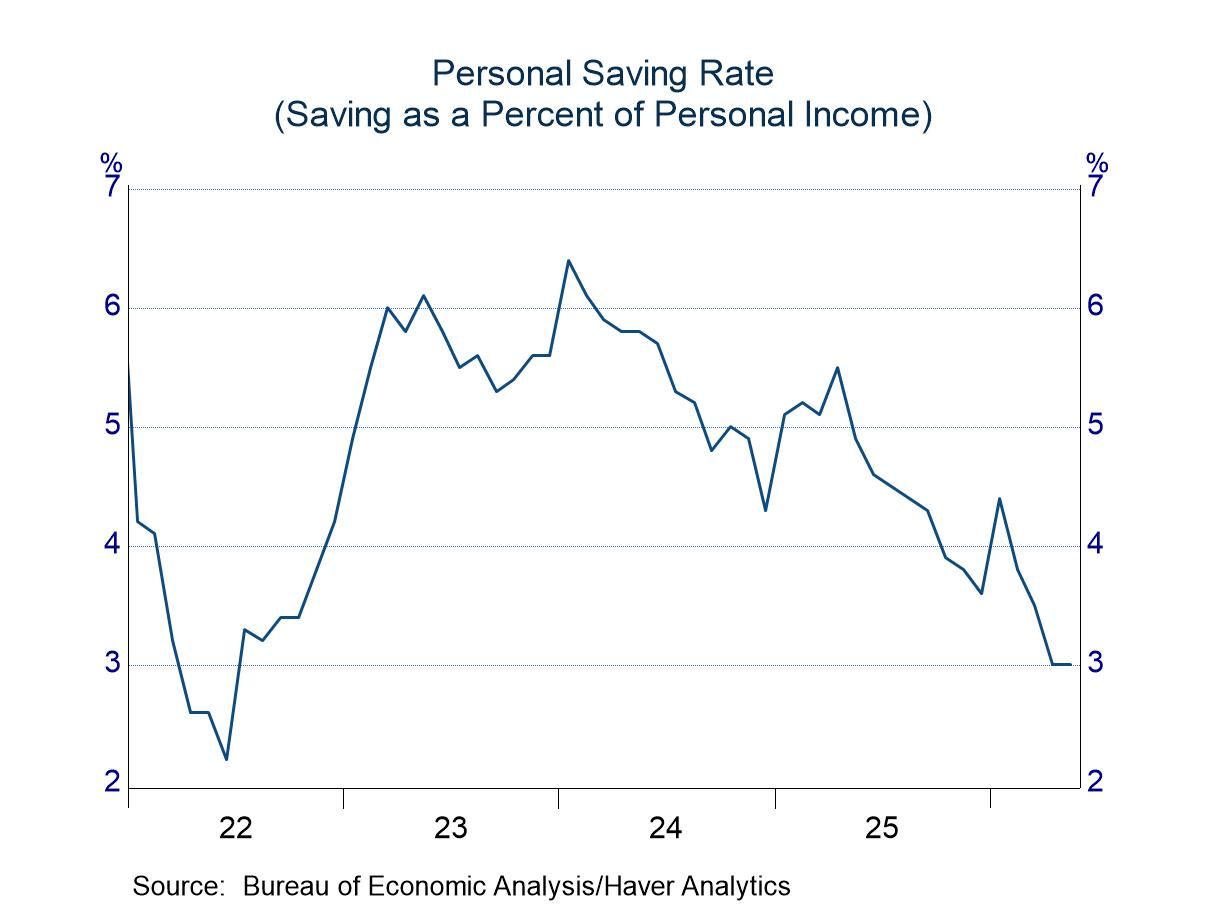

Households have managed to remain moderately active in their spending by limiting their saving. The saving rate has drifted lower since early 2024 moving to 3.0% in May (chart, below right). The erosion in saving perhaps seems reckless, but some of the reduction could be a response to the strength in the equity market, where wealth gains have possibly limited the incentive to save. Also, larger-than-normal tax refunds this year because of tax cuts in the One Big Beautiful Budget Act have allowed many households to spend actively despite modest increases in real income.

The personal income and consumption figures are available in Haver’s USECON database with detail in the USNA database. The Action Economics forecasts are in AS1REPNA.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global