Personal Income and Consumption

Summary

- The inflation rate for personal consumption expenditures remains uncomfortably high.

- Solid income growth, but cautious spending by households.

The monthly report on personal income and consumption contains a wealth of information on the earnings and spending of households, but the price measures in the report are likely to receive more scrutiny than the other measures. Two factors account for the keen interest in the inflation figures. The price index for personal consumption expenditures is the measure targeted by the Federal Reserve, and thus observers will be using the index to assess the likelihood of additional easing in monetary policy. In addition, the conflict in the Middle East is drawing more attention to inflation risks.

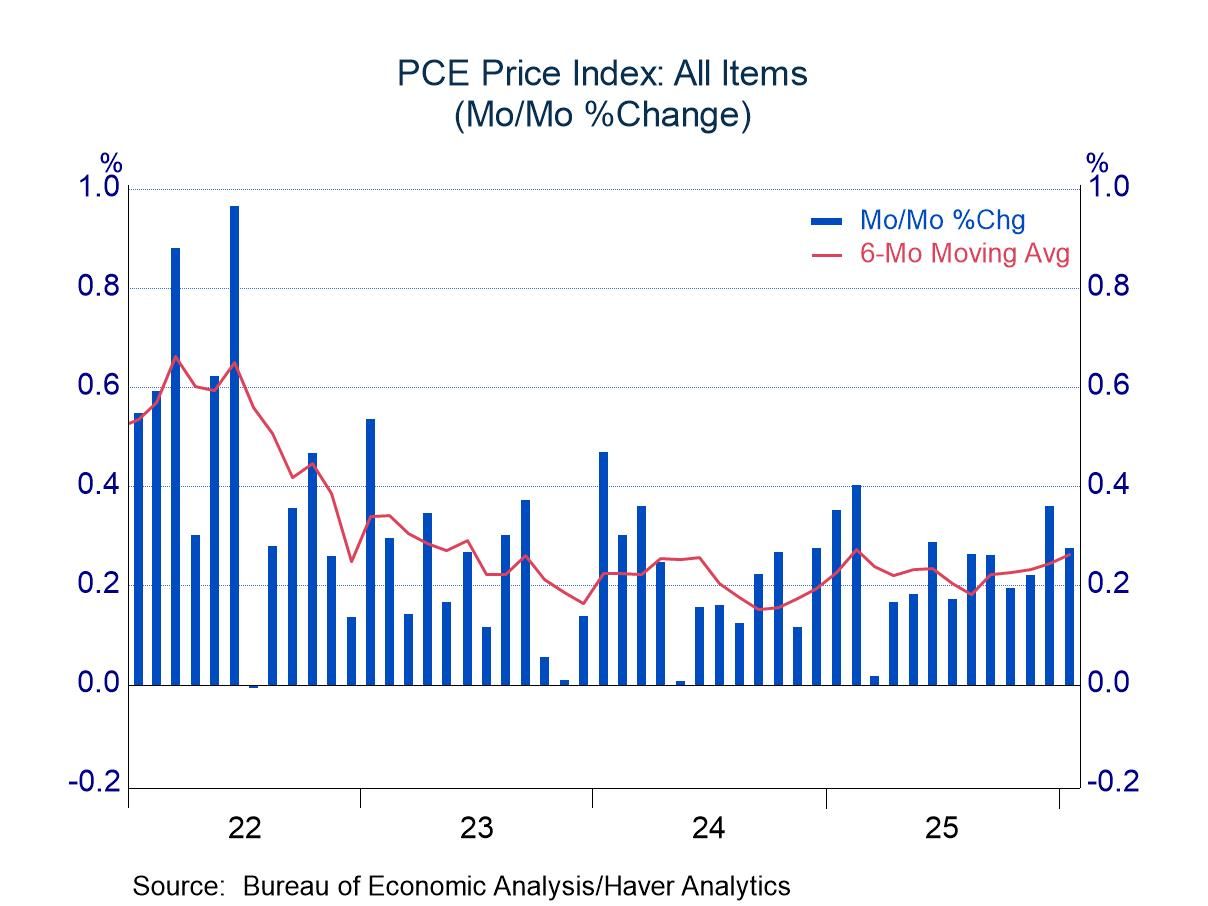

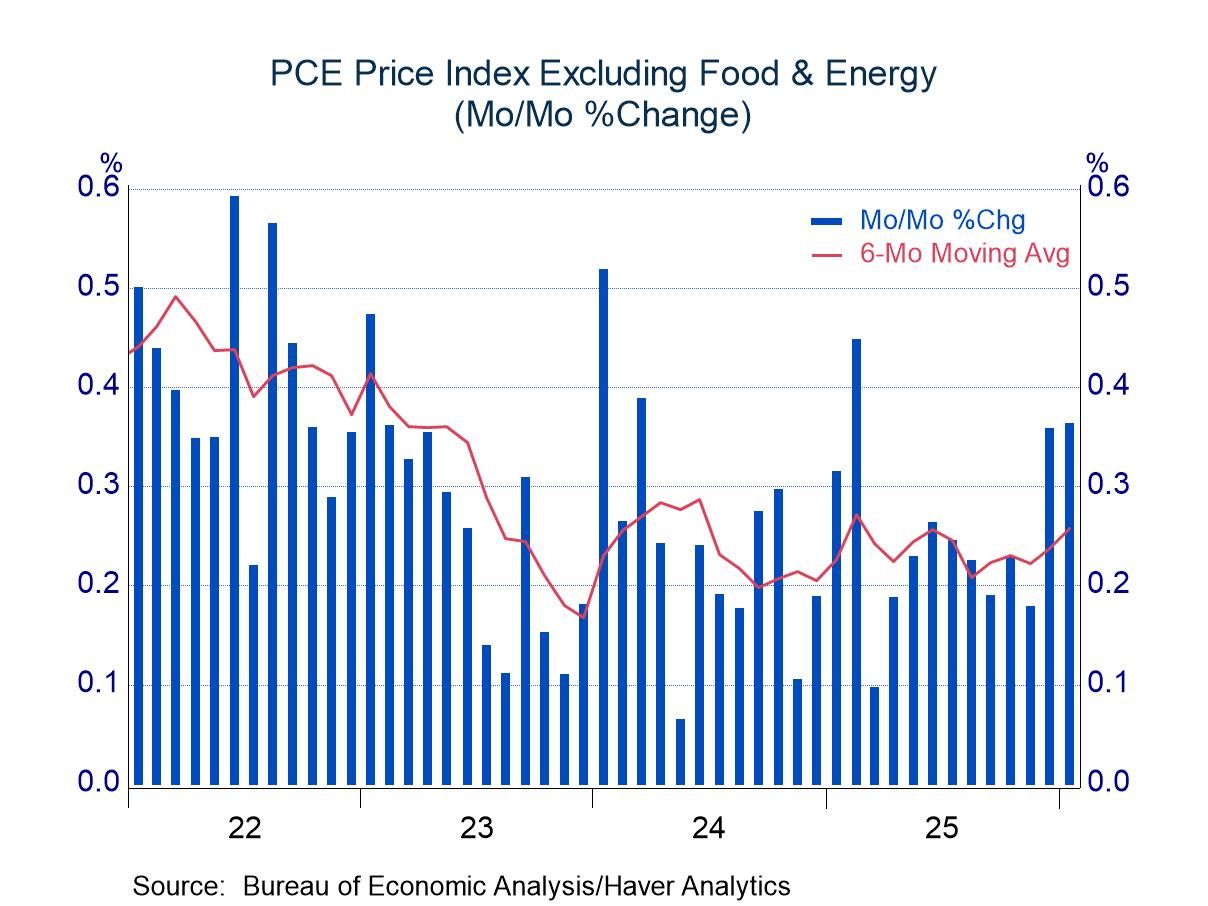

The inflation results for January were unfavorable, with the headline measure increasing 0.3% and the index excluding food and energy advancing 0.4%. The latest results left the year-over-year advance in the headline measure at 2.8%, down one tick from the reading in January, but still noticeably above the Fed’s target of 2.0%. The increase in the core index pushed the year-over-year change to 3.1% versus 3.0% in January. Both the direction of change and the deviation from target are likely to weigh heavily on Fed deliberations.

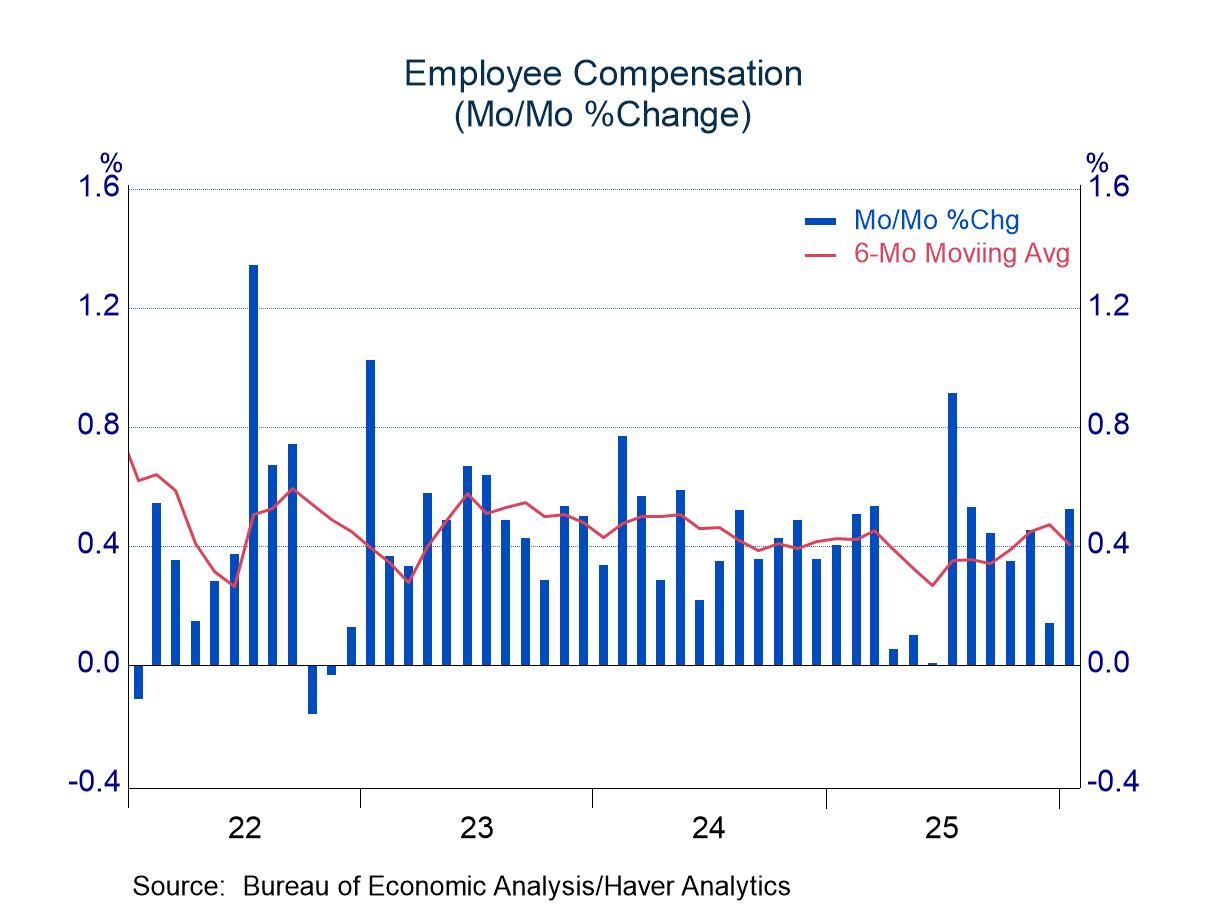

The inflation readings in the report dampened firm increases in nominal income flows. Total personal income rose 0.4% in January, but this nominal advance translated to a real gain of only 0.2% (and rounding up to get there; 0.152% when calculated with more precision). Employee compensation was among the strongest components of income with an increase of 0.5% (0.2% in real terms). Dividend income was robust with an increase of 2.0%, but it is perhaps too early to get excited about the increase. Dividends also rose sharply in January of 2024 and 2025 only to be largely offset by declines in February. Hold the champagne until next month.

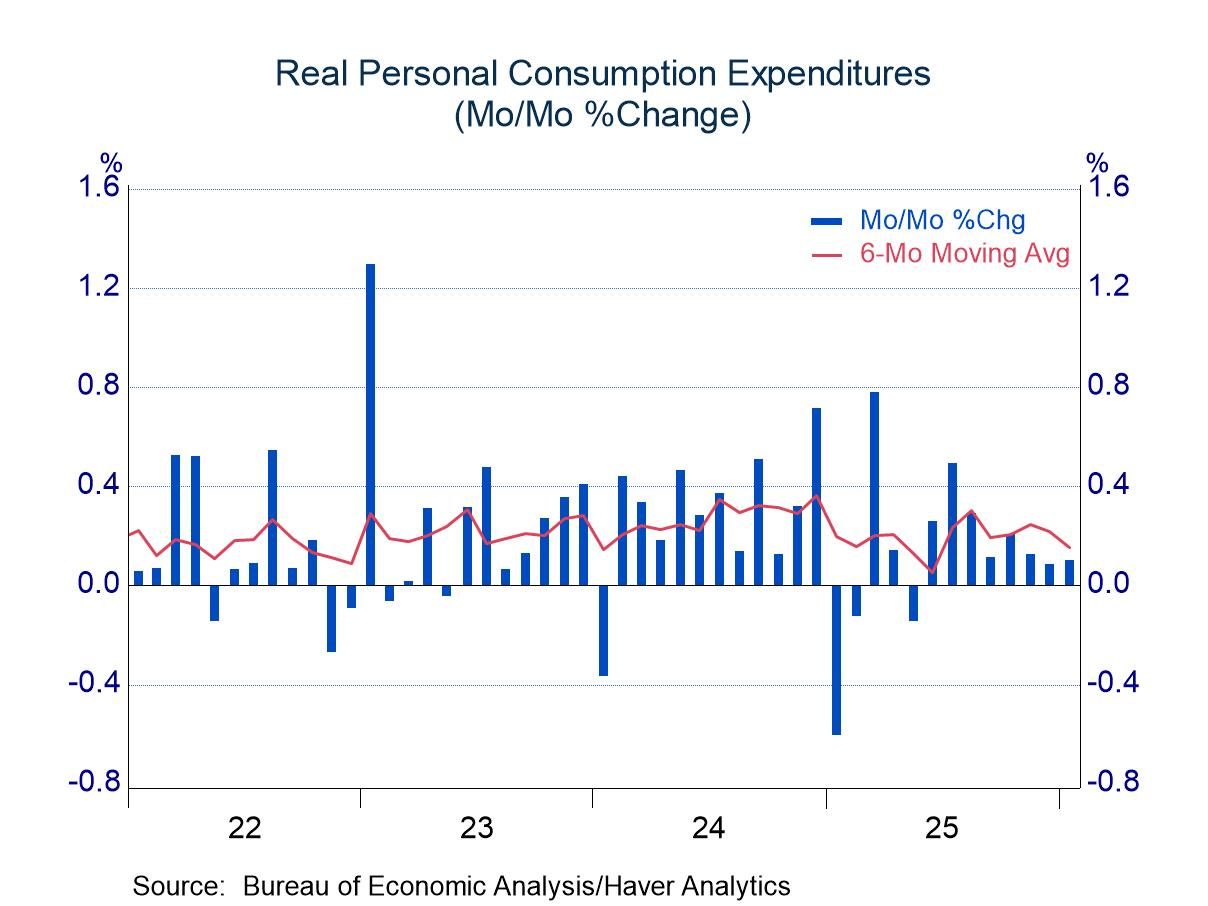

Although income growth was respectable, consumers spent cautiously. Nominal outlays rose 0.4%, but this translated to an increase of only 0.1% after adjusting for inflation. The modest increase sets the stage for a possibly slow quarter for consumer spending in the GDP accounts. If real outlays were to remain at their January level for the next two months, growth of real consumer spending in the GDP accounts would total only 0.8% in Q1. Increases of 0.2% in both February and March would lift growth of consumer spending to 1.6% in the first quarter, still noticeably shy of the 2.9% average in the prior three years.

The personal income and consumption figures are available in Haver’s USECON database with detail in the USNA database. The Action Economics forecasts are in AS1REPNA.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global