MOF Japan Business Outlook Survey

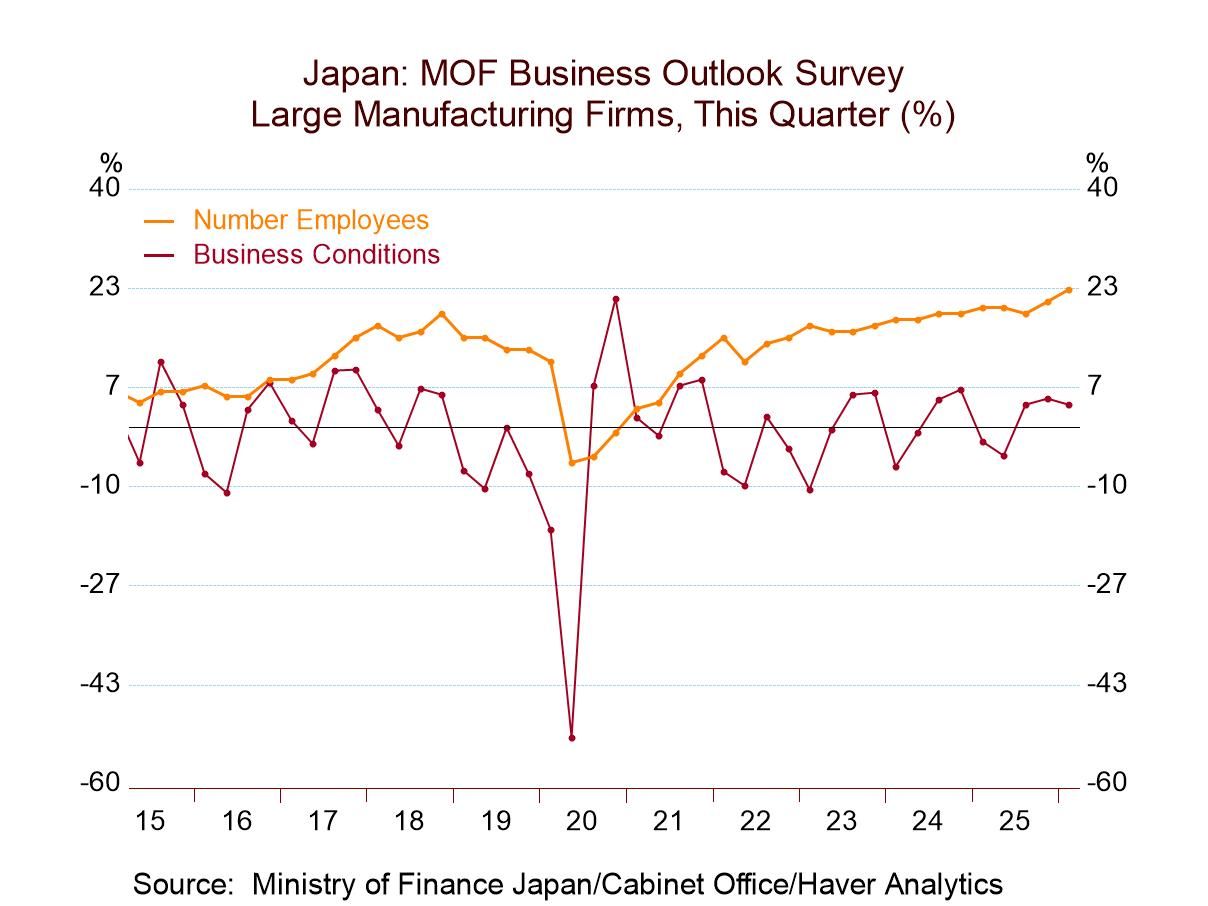

Japan's Ministry of Finance business outlook survey shows a slow but positive improvement in the outlook for employment among large firms, while the outlook for large manufacturing firms’ hiring continues to cycle and oscillate around zero (see Chart).

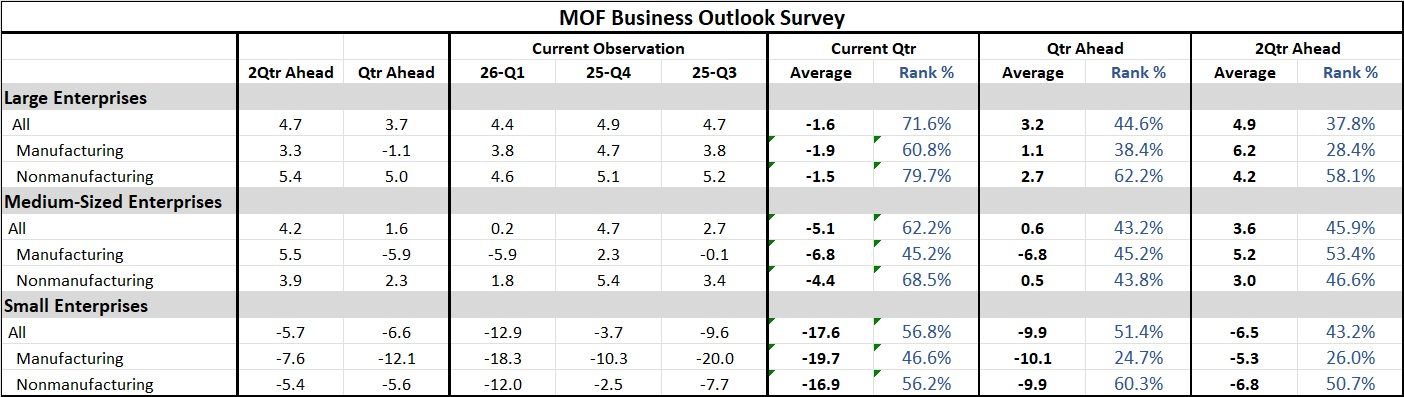

The assessment on current observations of the economy slipped to +4.4 for all large enterprises in the first quarter of 2026, compared to +4.9 in the fourth quarter of last year. For large manufacturing enterprises, the assessment slipped to 3.8 from 4.7. There were also slippages reported for medium-sized enterprises as well as for small enterprises; for both the total and manufacturing sectors, assessments were worse, the smaller the reporting unit (on both a net reading basis and a percentile standing basis).

The quarter-ahead assessment slipped to 3.7 from the 4.4 assessment of the first quarter for all large enterprises. For large manufacturing enterprises, the outlook slipped from plus 3.8 in the first quarter of this year to -1.1. The second quarter ahead outlook, however, improved to 4.7 from 3.7 for all large enterprises, and the manufacturing outlook for two quarters ahead picked up to 3.3 from -1.1 in the quarter ahead. However, that 3.3 outlook for large manufacturing enterprises is still below the first quarter assessment (of 3.8) as well as below the fourth quarter and the third quarter assessments of 2025.

The percentile standing of the quarter-ahead assessment for all large enterprises is 44.6. For manufacturing firms, the percentile standing is 38.4, and for nonmanufacturers it is 62.2. The percentile standing values compare the current observation with a history of observation readings back to 2007; values above the 50th percentile are above their historic medians. We can see for the quarter ahead for large enterprises all of their responses are above their medians, and the relative strength resides among nonmanufacturing enterprises; they report the highest standings.

For the second quarter ahead, the percentile standings slip for the total group of large enterprises as well as for manufacturing and nonmanufacturing, separately. This occurs even though the net assessments improve from the quarter ahead to two quarters ahead. You can get an inkling ‘why’ by looking at the ‘average’ and noting that the average two-quarter ahead reading has been higher than the average quarter-ahead reading. So, to rank higher than the quarter-ahead, the second-quarter ahead has a higher hurdle to go over. The standing for nonmanufacturing slips from a 62.2 percentile for the quarter ahead to a 58.1 percentile standing for the second quarter ahead. Large manufacturers take a relatively large step back to a 28.4 percentile standing two quarters ahead from the 38.4 percentile for one quarter ahead. These step backs are reflected in the headline which steps back to 37.8 for two quarters ahead from a 44.6 percentile standing for the first quarter ahead.

What is evident in this survey is that large enterprises that the MOF surveys are becoming increasingly pessimistic as we look farther into the future, since the current rankings for all large enterprises, large enterprise manufacturers, and large nonmanufacturers show the strongest percentile standings among this triad of readings for the current quarter, with the quarter-ahead standings weaker and two-quarter-ahead standings weaker still. This growing pessimism is not a good feature.

Medium and small enterprises not as dismally inclined Medium-sized firms: The transit to greater pessimism that we see for large enterprises as we look further into the future does not carry over to medium enterprises. Medium enterprises do see lower readings for the quarter ahead compared to the current-quarter assessments, and generally the quarter ahead provides assessments that are below the 50% mark, making them below median expectations as well. However, for two quarters ahead, the percentile standings improve, and at least for medium-sized manufacturing enterprises, there is a reading above the 50-percentile mark for that category two-quarters ahead, putting it even above the 45.2 percentile reading posted for the current quarter.

Small firms: For small enterprises, there is no real generalization across the various types of firms. Manufacturing firms’ percentile standing from the current quarter to the quarter ahead just about halve themselves, a sharp step back for manufacturers. However, for nonmanufacturers, there's an improvement from a 56.2 percentile standing in the current quarter to a 60.3 percentile standing in the quarter ahead. These two groups are moving in opposite directions for two quarters ahead. Manufacturers stop that deterioration and gain back just a small measure of what they lose in the quarter ahead with their two-quarter ahead standing, while nonmanufacturers lose some of their ebullience as the percentile standing drops to a 50.7 percentile reading from 60.3 but still sports an above-median value.

Summing up As a bellwether, the large enterprises and particularly manufacturing firms are the preferred gauges. On this basis, the results of the survey are disappointing. Although current assessments are quite fine, the outlook is certainly off-putting and that may be surprising with new Prime Minister, Takaichi, having just taken office and won a large majority in a snap election. Perhaps firms are more concerned about prospects for fiscal policy and whether there will be excessive stimulus and possibly they are also more concerned about the potential for the Bank of Japan to be held back from raising rates to contain growing inflationary pressures. But even with the new apparently very popular Prime Minister in office, it's surprising to see the MOF survey create such a weak set of readings.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global