Global| Apr 23 2026

Global| Apr 23 2026Charts of the Week: Risks Build, Markets Shrug

by:Andrew Cates

|in:Economy in Brief

Summary

Financial markets have remained notably calm in recent weeks despite rising geopolitical tensions in the Middle East, a more downbeat macroeconomic narrative and elevated uncertainty. Measures of financial stress and volatility remain low, and equity markets continue to look through both the conflict and softer data. That resilience sits alongside a more nuanced macro backdrop. The IMF’s latest WEO revisions point to a classic stagflationary energy shock—growth downgraded and inflation revised higher—although the global impact remains modest and uneven, with some economies still benefiting from stronger momentum (chart 1). At the same time, market pricing appears increasingly detached from the data flow, with volatility declining even as growth surprises have turned more negative relative to inflation (charts 2 and 3). Incoming inflation data reinforce the idea of a largely headline-driven shock, with nowcasts rising in line with higher energy prices but only limited pass-through into core inflation so far (charts 4 and 5). However, it remains early days. Survey evidence, such as the latest ZEW release, suggests that inflation expectations may already be responding in a more concerning way, with a marked rise alongside weakening growth sentiment (chart 6). Taken together, the key question for markets is whether this remains a contained, energy-driven shock that can be looked through—or whether it begins to embed more persistently via expectations, forcing a reassessment of the currently benign outlook.

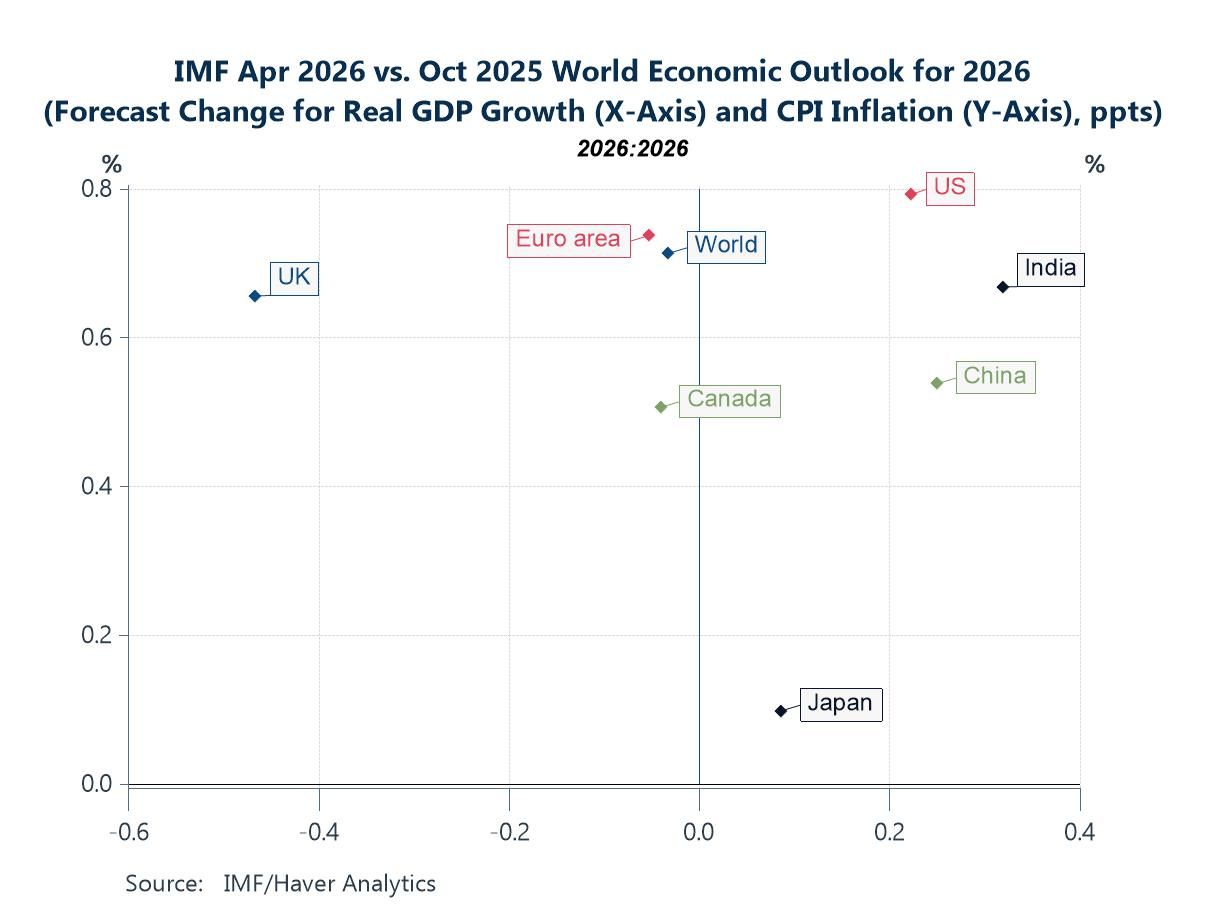

Energy shock lifts inflation, trims growth The IMF’s latest WEO revisions for 2026 broadly reflect the classic stagflationary impact of the recent Middle East energy shock, with growth downgraded and inflation revised higher across most major economies. Higher energy prices act as a tax on real incomes while simultaneously pushing up costs. That said, the picture is not uniform: a number of economies—notably the US, China and India—have seen growth upgrades, reflecting stronger-than-expected momentum so far in 2026. By contrast, the UK stands out at the stagflationary extreme, combining one of the largest growth downgrades with a relatively strong inflation uplift—consistent with its weaker underlying momentum, greater energy sensitivity and more persistent domestic inflation dynamics. More broadly, while the global revisions remain modest—pointing to resilience in activity—the message is that disinflation is no longer a smooth glide back to target but increasingly contingent on energy prices and geopolitical developments.

Chart 1: IMF WEO Revisions for 2026: A Contained Stagflation Shock?

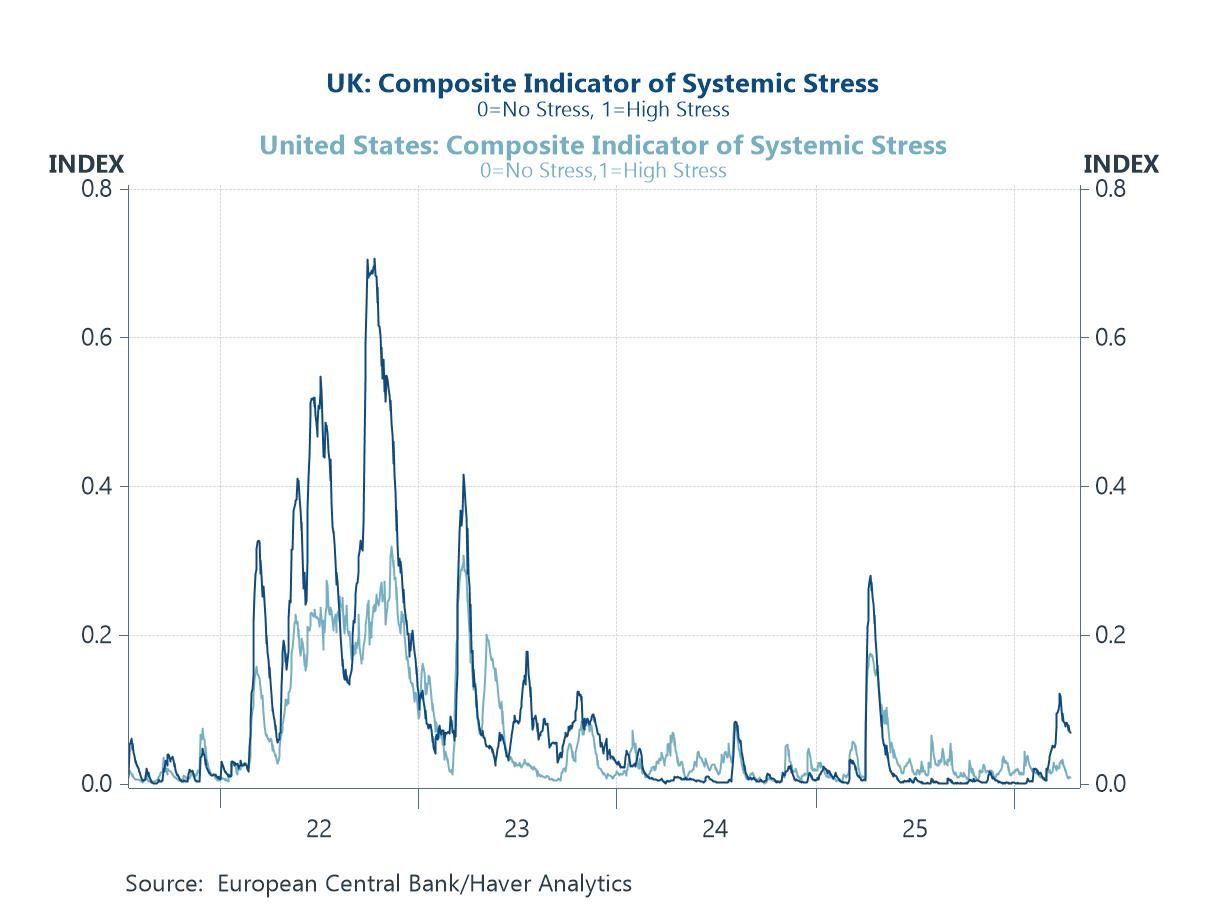

Markets largely shrug off rising economic pessimism Notwithstanding a more downbeat assessment from economists—including the IMF’s stagflationary tilt to the outlook—there has been remarkably little follow-through into financial markets. Measures of systemic stress in both the US and UK remain low by historical standards, suggesting that investors are, for now, largely looking through the Middle East conflict. There are several possible explanations: corporate profits remain resilient, the AI-driven investment narrative continues to dominate market thinking, and markets may be assuming that any energy shock will be temporary and contained. In effect, investors appear to be pricing a benign baseline in which geopolitical risks do not materially disrupt growth, inflation expectations or policy. The UK is a partial exception, with a somewhat more visible uptick in stress, which aligns more closely with the IMF’s more challenging growth-inflation trade-off and the economy’s greater sensitivity to energy prices.

Chart 2: ECB Gauges Suggest That Financial Stress Remains Contained Despite Geopolitical Risks

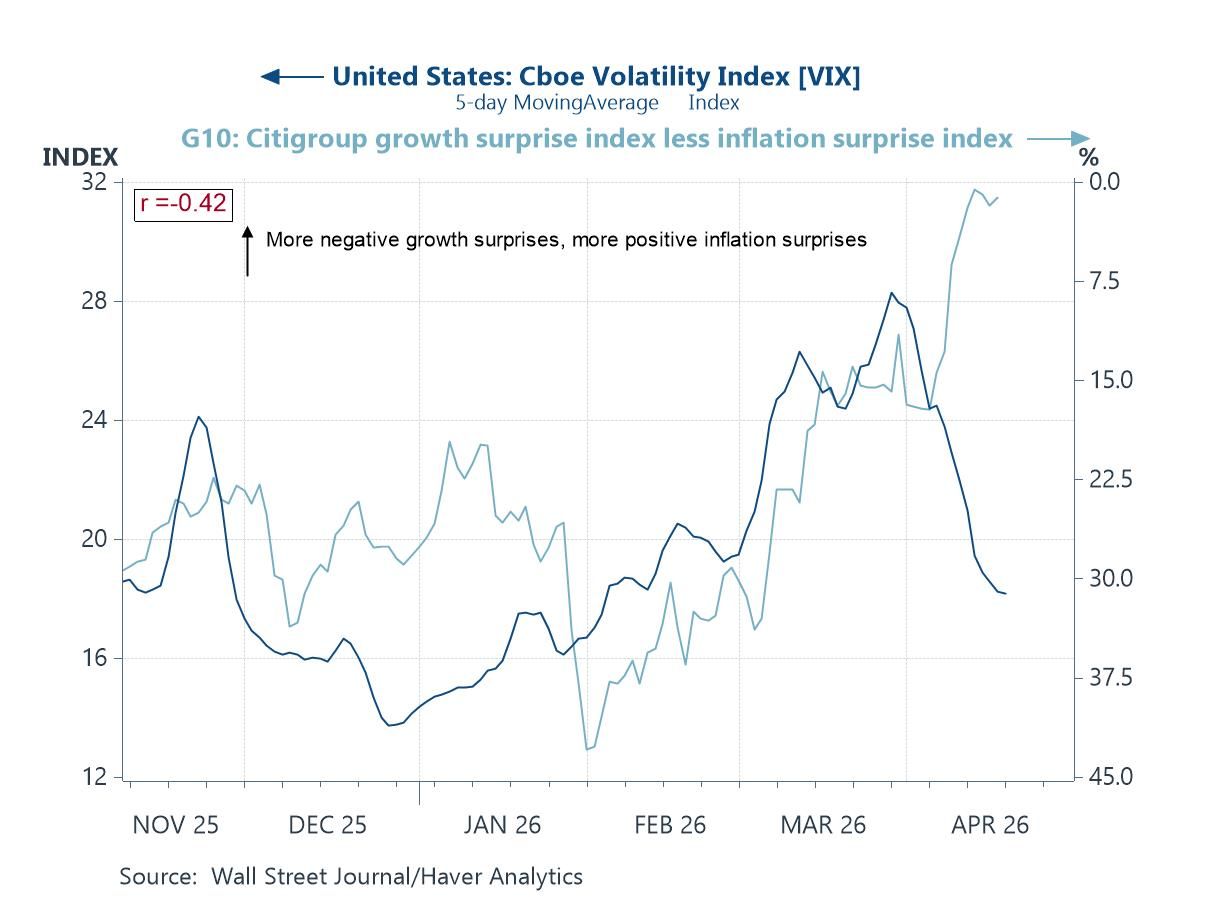

Volatility falls despite deteriorating growth surprises Market optimism is also increasingly at odds with the incoming data flow. Typically, equity volatility declines when growth surprises are positive and inflation surprises are benign. However, the recent pattern has broken that relationship. Growth surprises across the G10 have turned increasingly negative (our series is inverted in the chart below), yet volatility has continued to fall. In other words, markets are becoming less sensitive to weakening macro data, continuing to price a benign outlook even as the data deteriorate. This divergence reinforces the broader theme: investors are, for now, looking through both geopolitical risks and softer economic momentum, placing greater weight on resilience in earnings, the AI-driven narrative and the assumption that policy will remain supportive.

Chart 3: Markets Look Through Weakening Data Flow

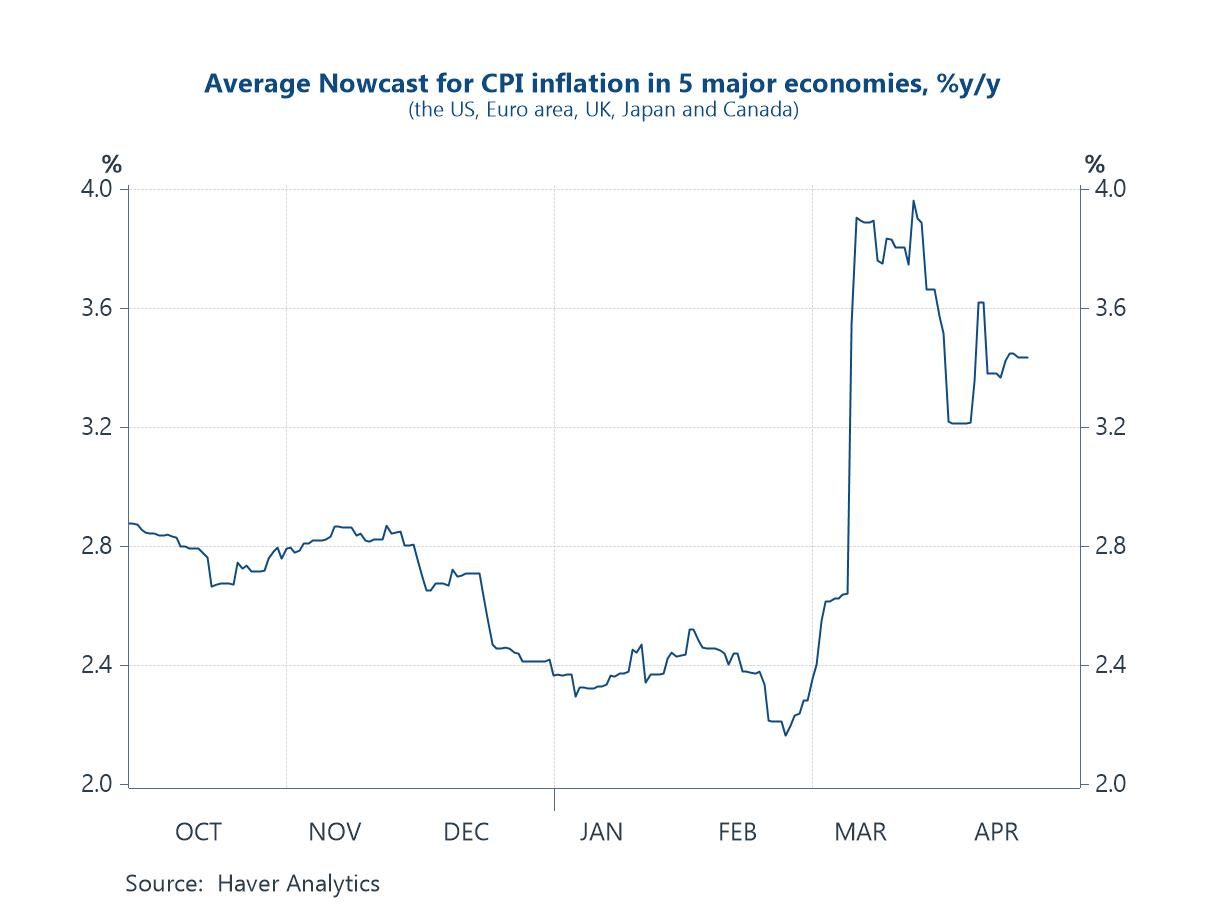

Inflation Nowcasts Have Jumped Incoming data suggest that headline inflation has moved higher in recent weeks, broadly in line with expectations given the rise in energy prices following the Middle East shock. Nowcasts for CPI across the major economies show a clear rebound in March and April from the lows seen at the start of 2026, with the move occurring in a relatively synchronised fashion. This reinforces the view that the recent pickup in inflation is being driven primarily by a common external factor—energy.

Chart 4: Headline inflation rises across major economies

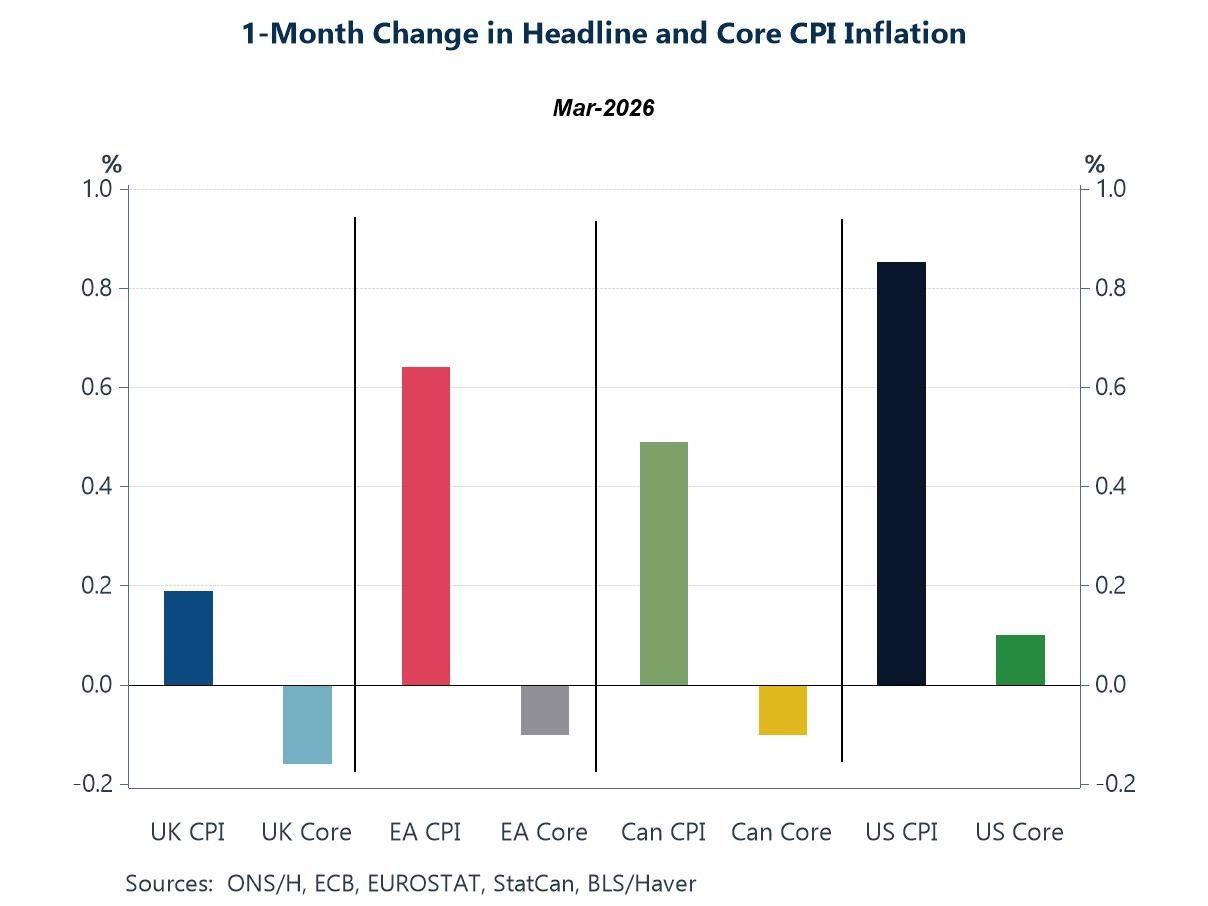

Energy shock not yet feeding into underlying inflation However, the detailed breakdown of March inflation outcomes suggests that this remains, for now, a largely headline-driven phenomenon. While headline CPI prints were firm across most economies, core inflation—stripping out energy and food—was more subdued and in some cases weaker. This indicates that there has been very limited pass-through from higher energy prices into broader goods and services inflation at this early stage. In other words, the shock is still being absorbed rather than propagated. That distinction is critical for policy and markets alike: as long as second-round effects remain contained, central banks may be able to look through the near-term rise in inflation, even as headline rates move higher.

Chart 5: Limited Core Pass-Through—For Now

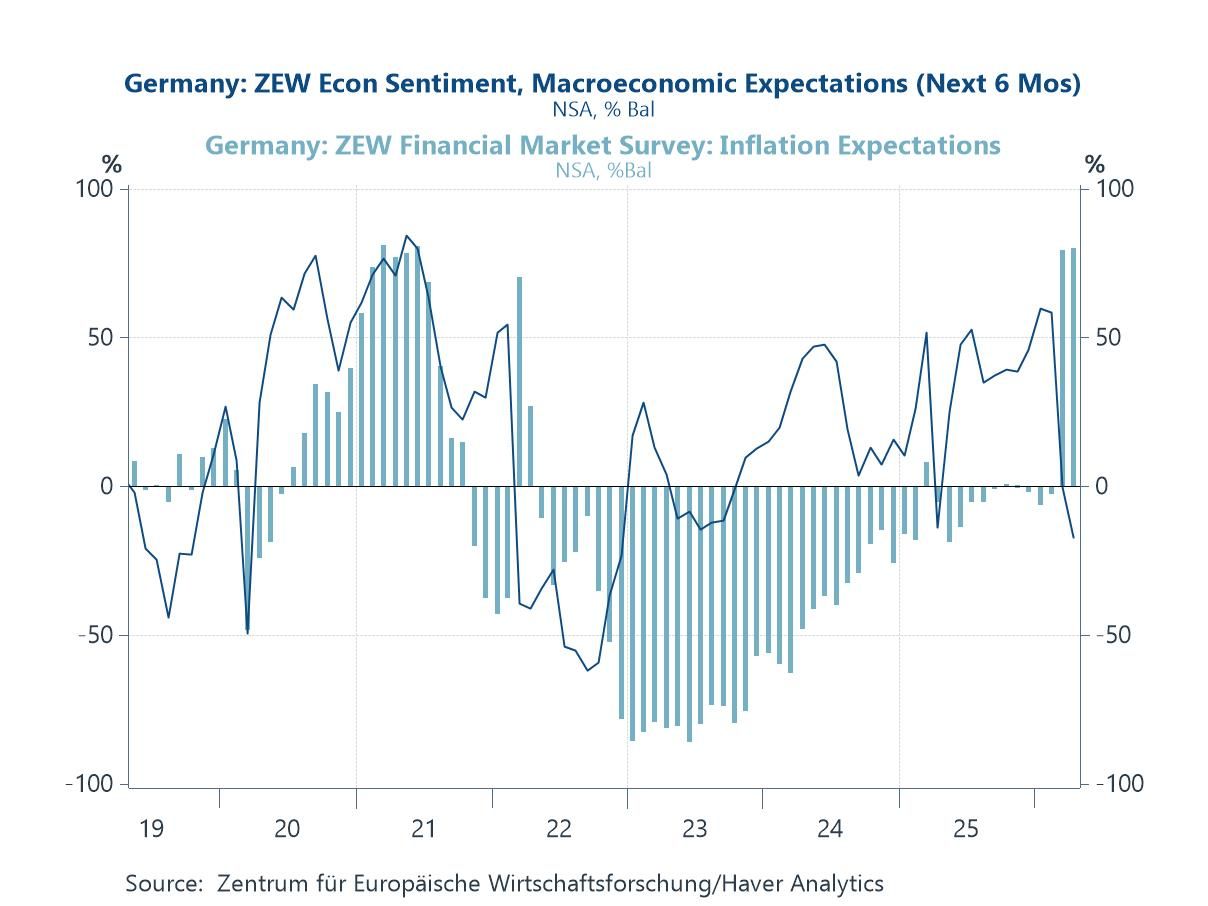

Inflation Expectations Rising as Growth Sentiment Falters It remains early days, and much will hinge on how inflation expectations evolve from here. The latest ZEW survey for Germany already conveys the hallmarks of a classic stagflationary shock, with macroeconomic expectations weakening even as inflation expectations have ratcheted sharply higher. This shift is important: while the recent rise in headline inflation has so far shown limited pass-through into core, a sustained increase in expectations would raise the risk of second-round effects and make the inflation process more persistent. In that sense, the ZEW data highlight the key fault line in the current environment—whether the energy-driven shock remains contained, or begins to embed itself more broadly through expectations and pricing behaviour.

Chart 6: ZEW survey signals a classic stagflationary shift

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief