National Bank of Belgium Consumer Survey for April

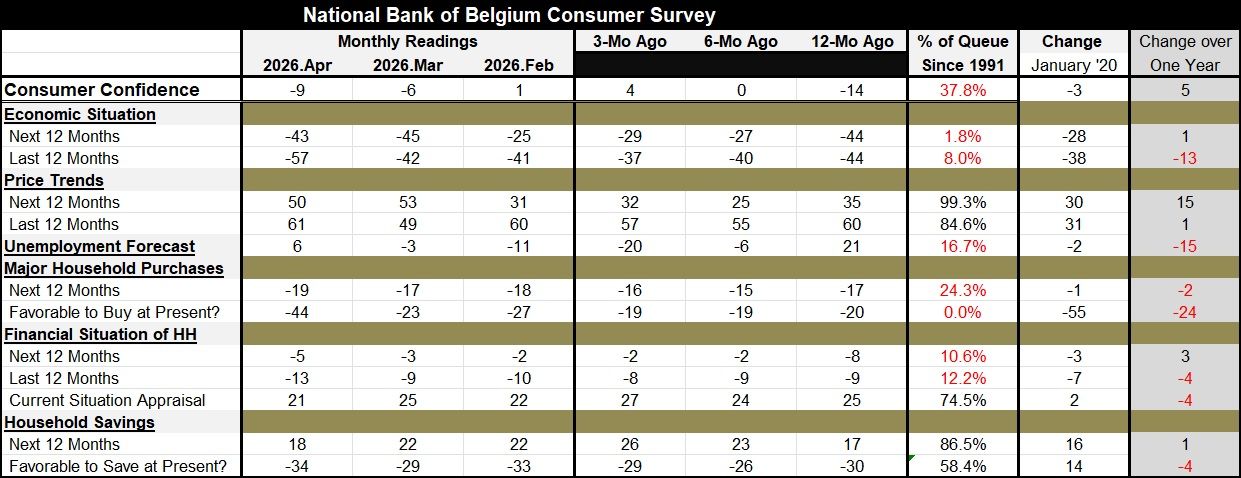

The National Bank of Belgium consumer survey for April registered -9, compared to a reading of -6 in March and +1 in February. Since the war in the Middle East began, confidence readings have declined steadily. However, the April consumer confidence reading of -9 still shows improvement from its level of -14 recorded 2 months ago. The index has a 37.8 percentile standing based on data back to 1991, which places it below its historic median: the median ranking occurs at a percentile standing of 50.

The responses to the survey are mixed and some of them are quite negative; however, a few also are quite upbeat. For now, the main message is that the survey is mixed. While most confidence readings tend to the weak side, there are a few that are actually quite encouraging.

Economic Situation A survey on the economic situation shows improvement for the next 12 months; its April reading rose to -43 in April from -45 in March. However, with the onset of war, the March reading had fallen to -45 from -25 in February, so the month-to-month uptick in April is really small potatoes. The 12-month change in the outlook for the economic situation over the next 12 months is a tick better in April 2026 than it was in April 2025. Continuing the back and forth on its “bad but not that bad” swing, the queue reading of the index on data back to 1991 has only a 1.8 percentile standing, marking it as weaker than its current level less than 2% of the time and ending the back-and-forth on whether the reading is poor or not. It is very weak.

The assessment of the economic situation over the last 12 months deteriorated to -57 in April from -42 in March, and it also worsened compared to its level of a year ago. In addition, its standing is in the bottom 8% of its historic queue data.

Prices Price trends give us some of the clearest and most negative views. Prices over the next 12 months improved slightly from March, moving to a reading of 50 in April from 53 in March. Still, the April reading of 50 is higher than its reading of 35 one year ago, and its standing is in the top 1% of all observations on data back to 1991. Those are dismal statistics. Price trends for the last 12 months are shown to have been slightly more stable but still with readings that had been historically worse, only about 15% of the time, marking the past inflation environment as having been poor as well.

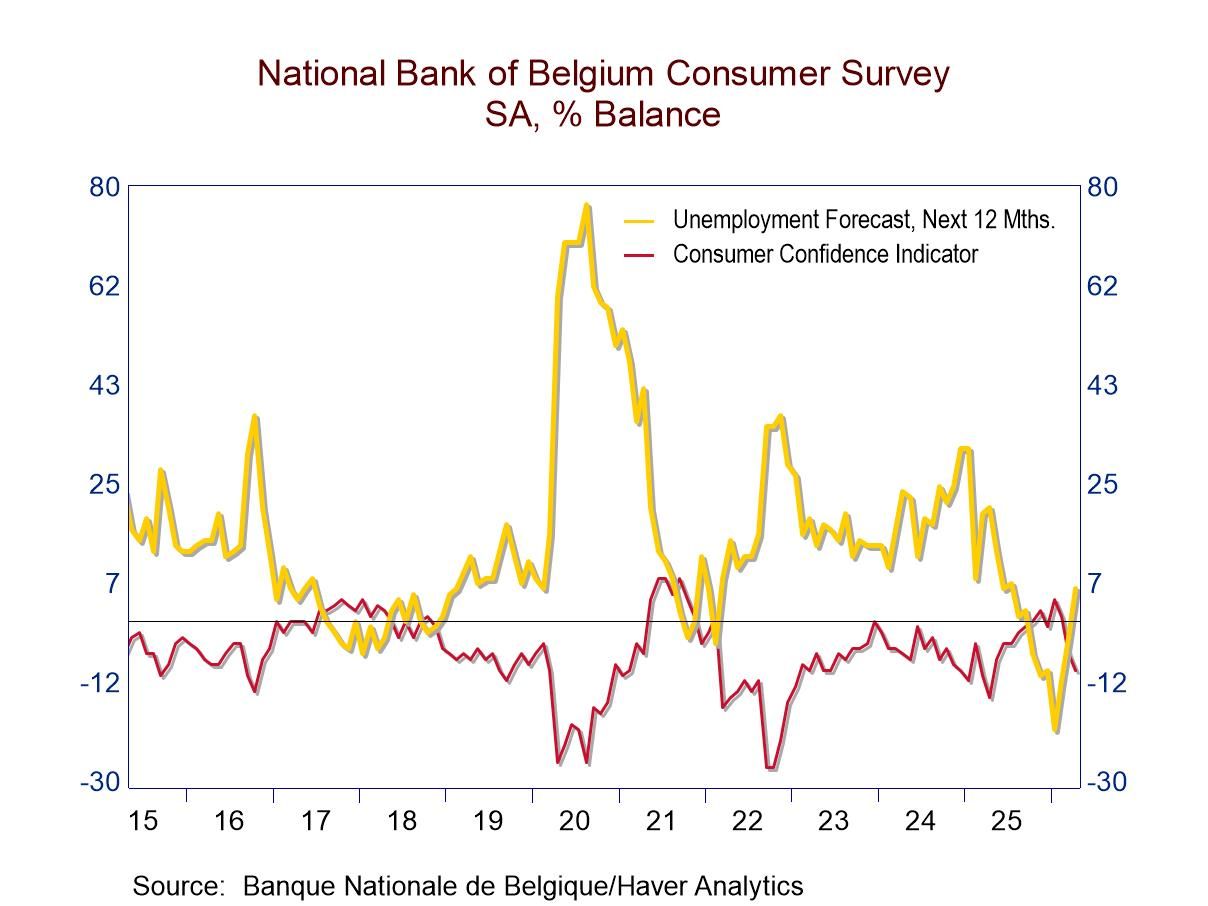

Unemployment The consumers’ unemployment forecast went up in April to a reading of +6 from -3 in March; it had deteriorated to -3 in March from -11 in February. A rising unemployment response reflects deterioration. People are assessing the possibility of unemployment as getting higher, although at +6 the April reading is substantially reduced compared to what it was a year ago at +21. The standing for the unemployment forecast is only in its 16.7 percentile of its historic queue of data, meaning that the likelihood of unemployment has been lower than this, only about 16% to 17% of the time.

Major Household Purchases If you look at the environment to make major household purchases, the responses of consumers become slightly more convoluted since the question as to whether it's favorable to buy at present deteriorated sharply in April to -44 from -23 in March; that was a sharp deterioration from -20 a year ago. Ranking the current -44 reading on data back to 1991, this is the weakest or the worst favorability for spending on this timeline. So that particular sequence of data doesn't fit really well with the unemployment responses, although being unemployed and finding it's a favorable time to buy goods are different things; both do speak to the economic environment which we can see is somewhat touch and go.

The outlook for making major purchases over the next 12 months deteriorated slightly over the last few months, with a reading of -19 compared to -17 a year ago. That current reading has a 24.3 percentile standing, placing it in the lower quartile of its historic queue of data. This underlines that the spending environment has been poor throughout the last year compared to historic experience since the 1990s.

The Financial Situation of Households The financial situation of households over the next 12 months deteriorated slightly in April to -5 from -3, and it had deteriorated in March to -3 from -2 in February. Even so, the April reading of 5 was stronger than -8 recorded one year ago. Still, if we let the ranking on data back to 1991 be the arbiter of whether the assessment of conditions is weak, the 10.6 percentile standing for the financial situation ahead and the 12.2 percentile standing for the financial situation of households over the last 12 months both indicate decisive weakness.

The Current Situation The next reading is a bit of a surprise given the drumbeat of weakness that we see from the data above. The current situation appraisal did backtrack in April to 21 from 25 in March, but it's only slightly weaker than a reading of 22 in February. The April 2026 reading of 21 is slightly weaker than a reading of 25 one year ago. However, the April reading has a percentile standing on data back to 1991 at its 74.5 percentile, putting it right at the border of its top 25th percentile.

So, the current situation is appraised as a top 25-percentile standing, but the environment for making purchases over the next 12 months has a lower 24-percentile standing; and the current situation has a favorability for buying which is the worst that we've seen in the entire period. However, expectations of unemployment remain low. To round out this situation, the favorability to save over the next 12 months has a ranking in its 86-percentile, making it a top 15-percentile reading. The favorability to save at present has a 58-percentile standing, placing it above its historic median and slightly better than average. What we have are crosscurrents.

On balance, you see the consumers view their situation as having a lot of crosscurrents. In terms of the thing they fear the most, unemployment conditions are not considered to be at risk and the economic situation is appraised to be in the upper tier of where it has been since the 1990s even though the favorability of spending is the worst experience for consumers on that same timeline. But the inflation readings are unambiguously bad—and worsening.

It would appear from these crosscurrents that the Belgian consumer is ripe for being pushed one way or the other if events were to markedly either improve or to deteriorate.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia