German Ifo Plunges Everywhere

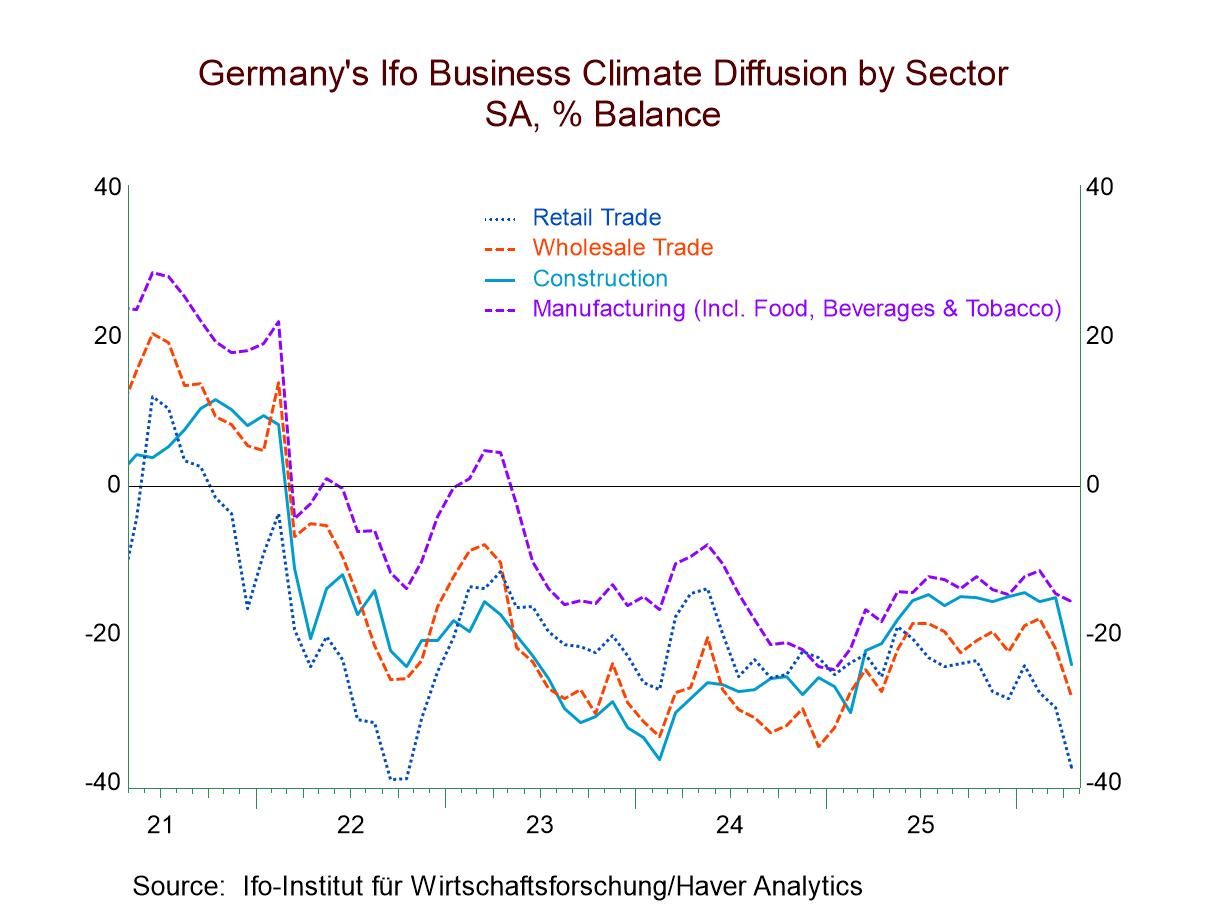

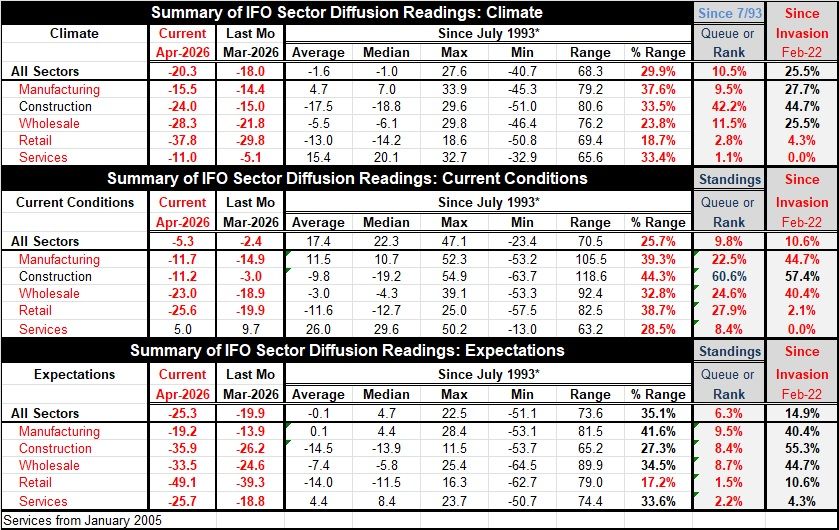

The onset of the war in Iran appears to have hit the German economy extremely hard as the Ifo survey shows very substantial and broad-based decline across its survey in April. The Ifo survey features readings for five sectors as well as an aggregate reading, and it surveys them for climate, current conditions, and expectations. The decline in the Ifo survey is present for all three concepts and across all five sectors, marking the weakening in April as a highly significant and extremely disturbing development. Only manufacturing in the current conditions survey escapes a month-to-month decline.

The Ifo sequences: The climate reading fell both overall and across each of the five sectors. Current conditions declined for the overall and for four of the five sectors, with manufacturing the sole exception. Expectations declined for the overall and for all sectors. Several of the sector declines were for a very substantial magnitude, especially when compared to historic changes in these indexes.

Monthly changes in readings—severe broad deterioration The month-to-month change in the climate reading has weakened more month-to-month 19% of the time. That overall result, however, is boosted by manufacturing where the monthly change has been weaker 35% of the time (on data back to 2011). However, all other sectors have seen climate weaker m/m only 2.3% to 6.3% of the time! The current situation readings weakened, with the headline weakening more m/m 11% of the time. This was boosted by manufacturing, the only sector that improved on the month; its ranking on change was in its 85th percentile—quite good and truly stand-alone good news. The other current changes by sector ranged from construction being weaker 1.7% of the time, to retailing that has been weaker about 30% of the time in terms of m/m changes. Expectation changes were uniformly terrible, with the headline drop weaker only 6.3% of the time and sector change month-to-month weaker between 9% and 1.7% of the time. The monthly weakening was uniform and substantial. I document it with these calculations, but you can also see it on the chart above.

Climate: The bottom line is that the all-sector index for climate fell to -20.3 in April from -18 in March, placing it at a 10.5 percentile standing on data since 1993. The sector ranking is the highest for construction with a 42.2 percentile standing and the weakness for services at a 1.1 percentile standing—weaker than the table reading nearly 99% of the time. In terms of percentile standing levels or monthly changes, conditions are closing in on grim.

Current conditions: Current conditions saw the all-sector index slip to -5.3 in April from -2.4 in March. The headline ranking stands at a 9.8 percentile mark, making it—like the climate reading—weaker than its current reading only about 10% of the time. The strongest reading under current conditions is for construction which has a 60.6 percentile standing; it is the only ranking in the table above its historic median. Manufacturing, the only sector in the survey that improved month-to-month, has a 22.5 percentile standing, while services record the weakest percentile standing under current conditions, at an 8.4 percentile standing.

Expectations: The all-sector index for expectations fell to -25.3 in April from -19.9 in March, placing it at a 6.3 percentile standing. The percentile standings across sectors range from a high of 9.5% for manufacturing to a low of 1.5% for retailing. Up until earlier this year, the Ifo was showing signs of improvement; however, all of that has simply collapsed in the last month. Weakness is across economic concepts and sectors, as documented above. For reference, the table also gives a separate set of rankings on where the various indexes stand since the invasion of Ukraine, since that was another marked event that drove the index, that had been improving after Covid, down to lower levels. Ranked even on this reduced scale looking at conditions only since the invasion of Ukraine, when conditions have generally been weaker, the current rankings across the Ifo survey remained extremely weak. This is a very disturbing survey for the German economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia