Global| Apr 23 2026

Global| Apr 23 2026S&P PMIs Show Mixed Fortunes

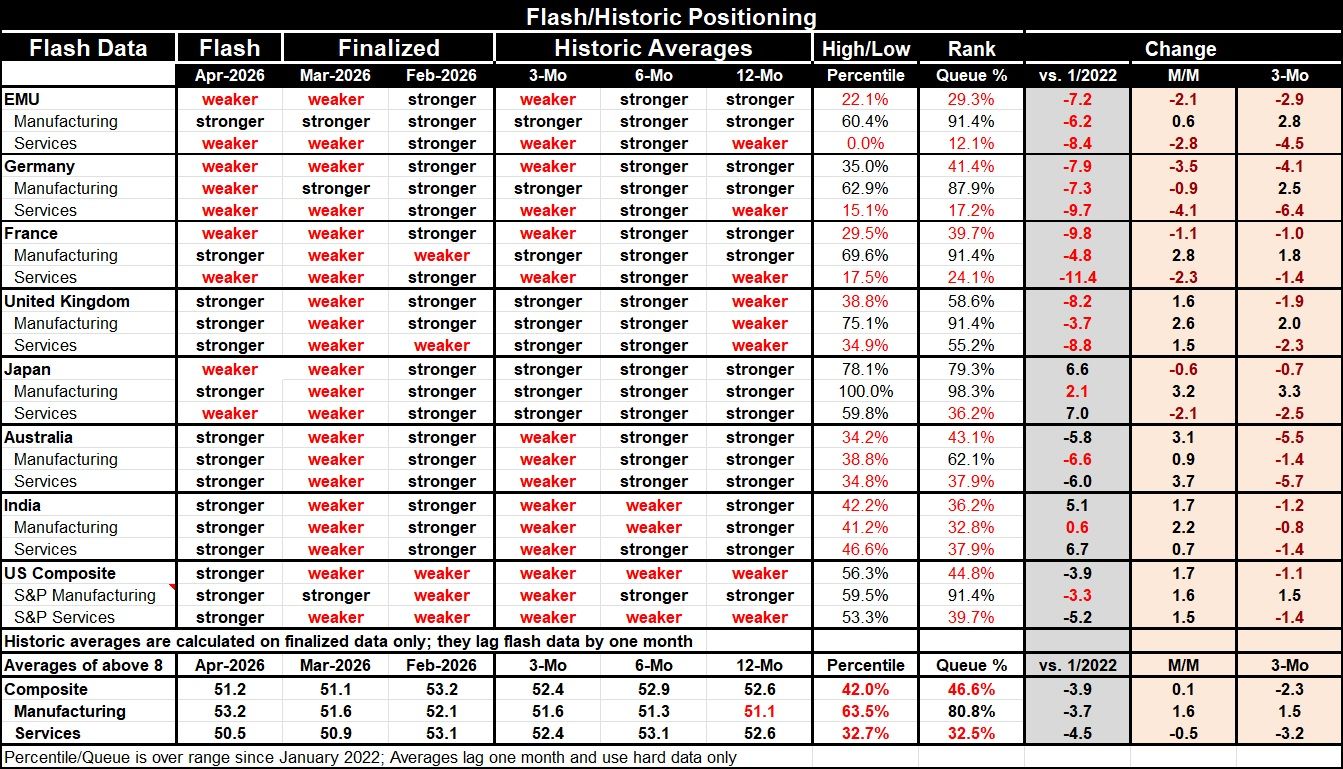

Manufacturing looks strong while service sectors weaken S&P's April flash PMI readings show some very mixed results. For the United States, India, Australia, and the United Kingdom, there is a strengthening in the readings month-to-month for services, manufacturing, and the composite.

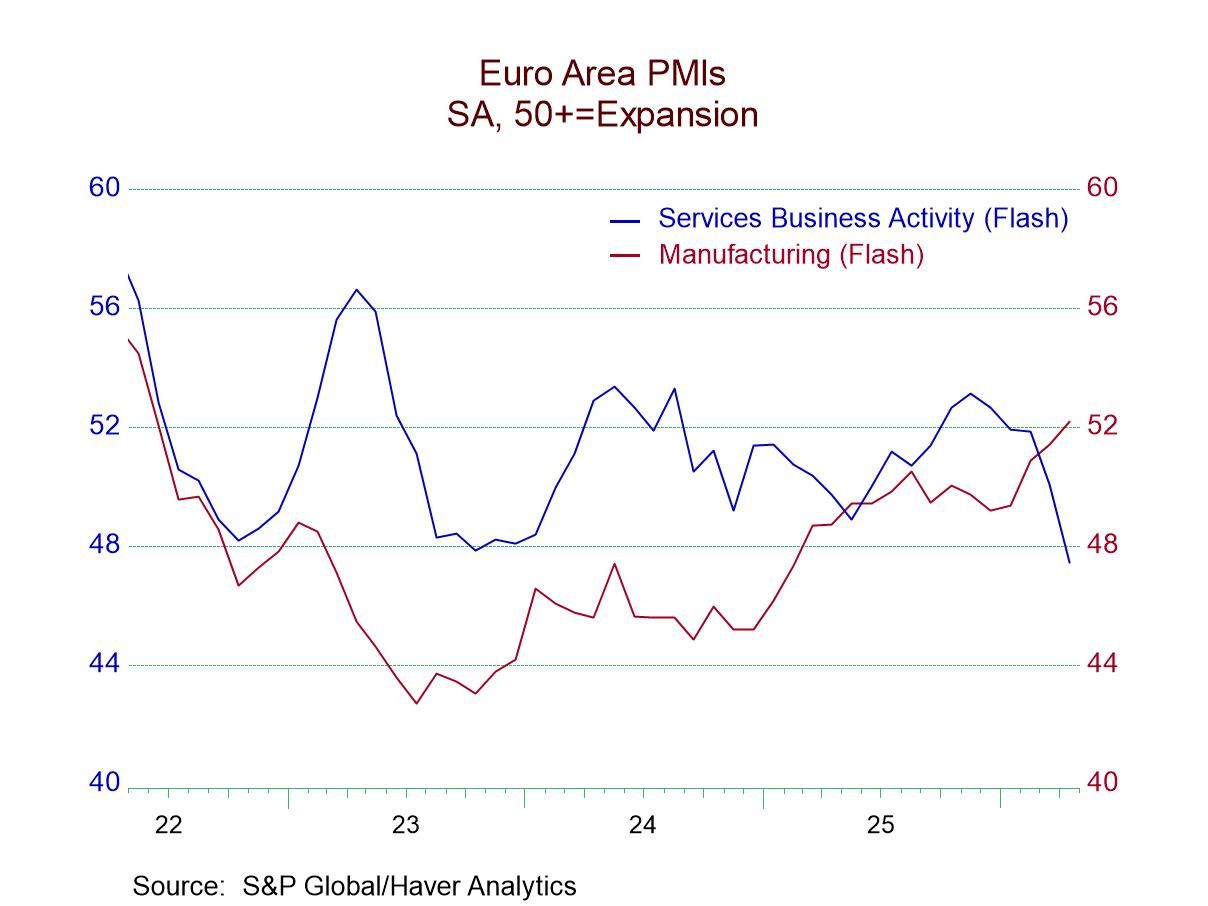

For Japan, France, and the European Monetary Union as a whole, there is improvement in the manufacturing sector on the month but a weaker services reading and a weaker composite overall.

Germany is the only responding area in the table showing weakness all around—in all three sectors—a weaker composite, a weaker manufacturing sector, and a weaker services sector in April. For Germany, this follows a weaker composite and service sector in March as well.

Most reporters—France, the United Kingdom, Japan, Australia, and India—had weaker readings for all three metrics in March: the composite, services, and manufacturing. The March exceptions were the United States, Germany, and the European Monetary Union; in each case, the exception was that the manufacturing sector improved month-to-month, while the composite and services both weakened.

This has been a period of weakening—in March and April—since the war in Iran began. The 48 separate sector readings produced 30 readings that were weaker month-to-month in March and April. Among the 16 composite readings, 12 reported weaker conditions month-to-month. In March, the immediate aftermath of the outbreak of war brought instantaneous step backs across the PMI readings, while April, responding to at least a military success in the area, has shown a significant bounce back that is now more common than further weakness.

The sequential data over three months, six months, and 12 months are based only on completed data; therefore, they're up to date through March. On that basis, we have triple sector weakness in the U.S., India, and Australia, with only Japan and the United Kingdom showing triple-sector improvement over three months. However, if we look at six months compared to 12 months, we have triple sector strength in the Monetary Union, Germany, France, the United Kingdom, Japan, and Australia. India and the U.S. each show only one stronger sector over that comparison—services in India’s case and manufacturing in the U.S. case.

Ranking Peculiarity The ranking data take the current flash data and compare them to the history of observations back to January 2022. What is quite surprising is that, on that timeline, the manufacturing sectors of all the countries in the table—except for Australia and India—show manufacturing standings in their respective 80th to 90th percentiles. Meanwhile, services standings are typically in the 30th percentile or lower.

Odd Impact of War If the war in Iran has an impact on something, we would expect that to fall on the goods trade sector. We would expect this to have an impact on manufacturing although it's the opposite thing that's happening. Manufacturing is showing a revival, while services sectors are showing weaker performance across these countries generally. India is an interesting case, with manufacturing only in its 32nd percentile; however, India’s raw diffusion reading for manufacturing is the strongest raw diffusion reading in the table. What India's ranking is telling us is that India had been extremely strong over the period since 2022, and now compared to that past standard, it's relatively weaker. However, it's still strong in absolute terms, showing a great deal of strength based on its pure diffusion value, just not in comparison to historic performance.

Next? At this point, it's not clear to me at least what these PMI data are telling us since the strength in manufacturing is a curiosity as is the weakness in the services sector. You see these two phenomena displayed in the chart above, in the case of the European Monetary Union’s flash readings as well.

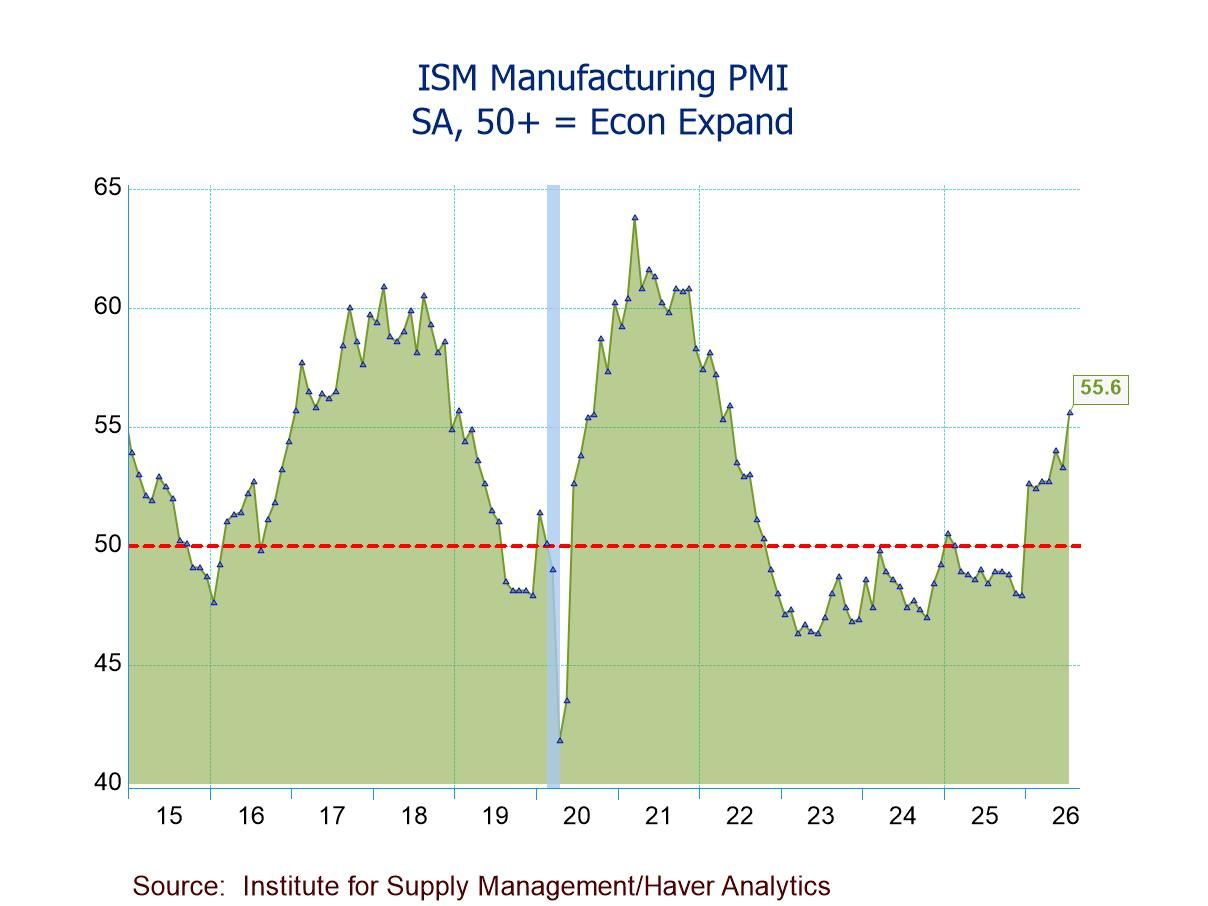

War breeds negative effects It's not a surprise that war would take some toll on consumer confidence or that it would be reflected in the services sector. However, seeing the kind of weakness being portrayed now in services against the strength in manufacturing is simply a bit hard to rationalize and understand. So, I think we're going to have to keep an eye on these readings as well as other readings in the months ahead to try to discern how global events, the war, conditions in the Strait of Hormuz, inflation currency shifts, and central bank policy are playing out across these various countries. None of what is happening is obvious to me. Japan clearly continues to benefit from a weak yen as its manufacturing sector is flying high, at its best reading since January 2022.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief