May CPI: Another Jump in Energy Prices; Core Contained

Summary

- Gasoline prices drove the energy component higher again, but June might bring some relief.

- Little apparent pass through from energy to core.

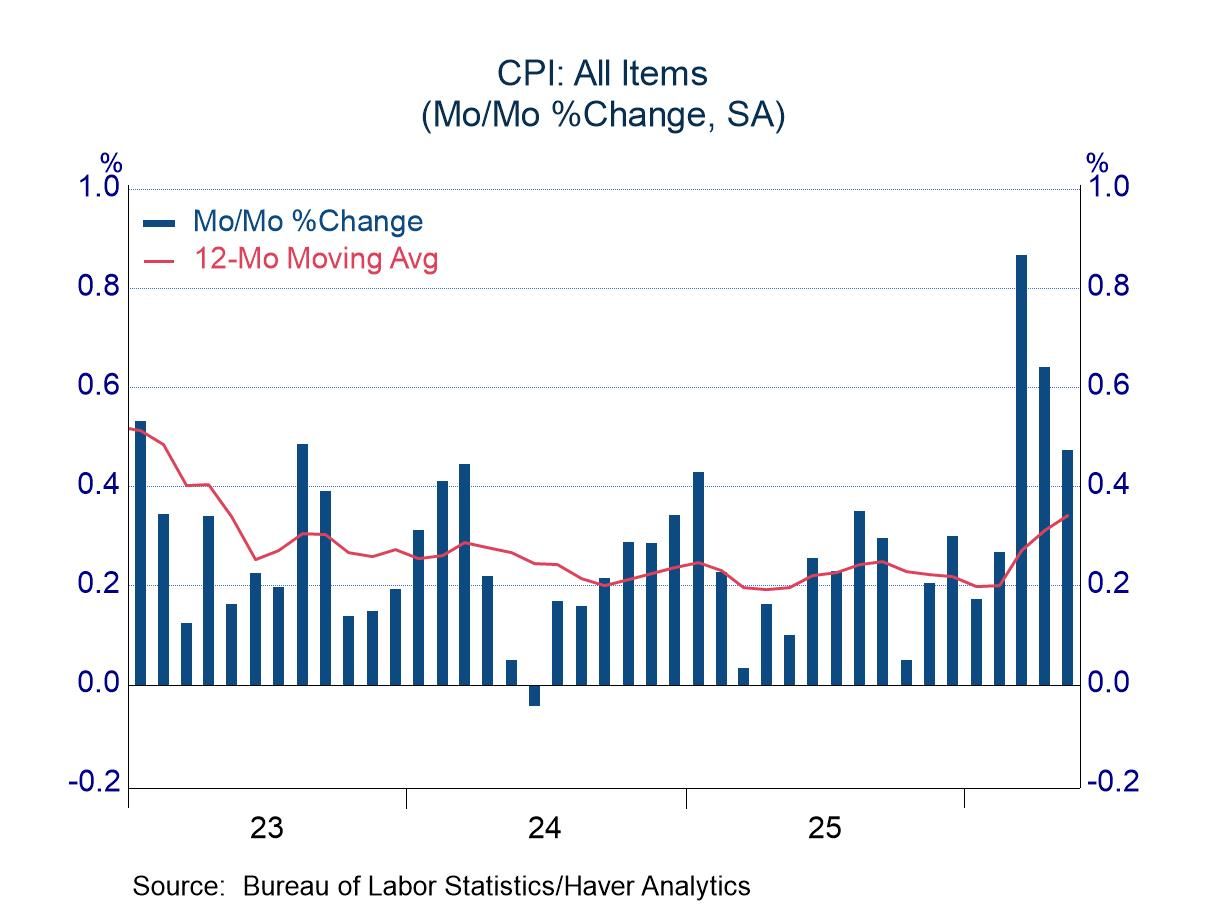

The headline Consumer Price Index rose 0.5% in May, matching expectations and slowing from increases of 0.9% and 0.6% in March and April, respectively. Although the month-to-month increase slowed in May, it still pulled the year-over-year change higher, now at 4.2% versus 3.8% in April. The year-over-year change totaled 2.4% in both January and February, before the conflict in the Middle East became a factor in the inflation setting.

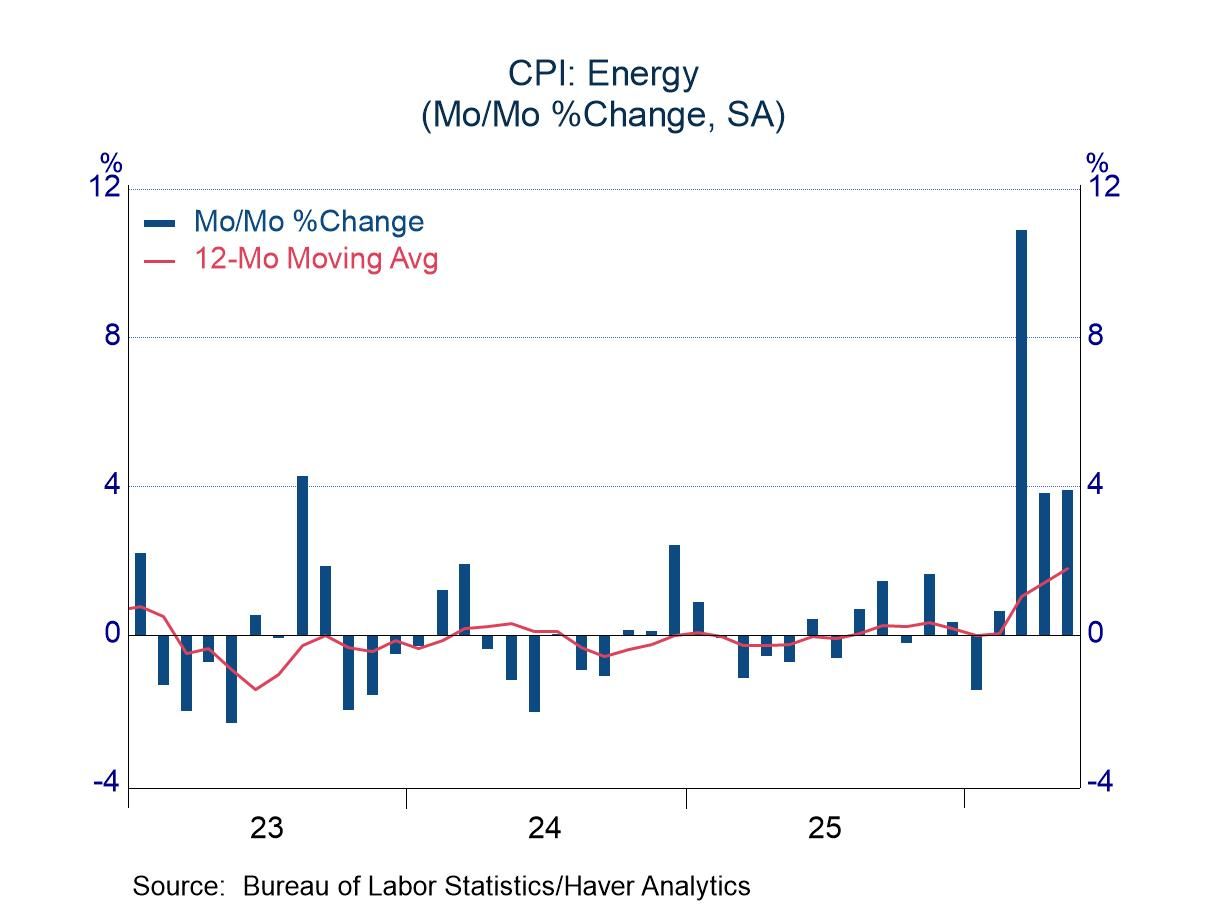

With the Middle East situation still unsettled, energy prices remained problematic, increasing 3.9% in May, slower than the blistering advance of 10.9% in March, but a touch firmer than the increase in April. Gasoline prices have been the driving force behind the increase in the energy component of the CPI. However, reported gasoline prices fell slightly in the first week of June. Perhaps next month’s report will bring some relief on the energy front.

Interestingly, energy pressure has been concentrated in petroleum-based products (fuel oil and gasoline). Charges for electricity have stirred a bit in the past three months, but the average increase of 1.2% is well shy of price changes in oil-related products. The price of natural gas services has declined for three consecutive months (average drop of 0.5%), which has left a year-over-year change of 3.0%.

Food prices posted a worrying increase in April (0.5%), but they were contained in May, rising 0.2%. Prices for food at home (i.e., grocery store prices), which are important for households facing affordability issues, rose less than 0.1%, although the year-over-year change of 2.7% will still pose a challenge for many. Prices for food away from home (i.e., prices at restaurants and bars) rose 0.3% in May, which left a year-over-year advance of 3.5%.

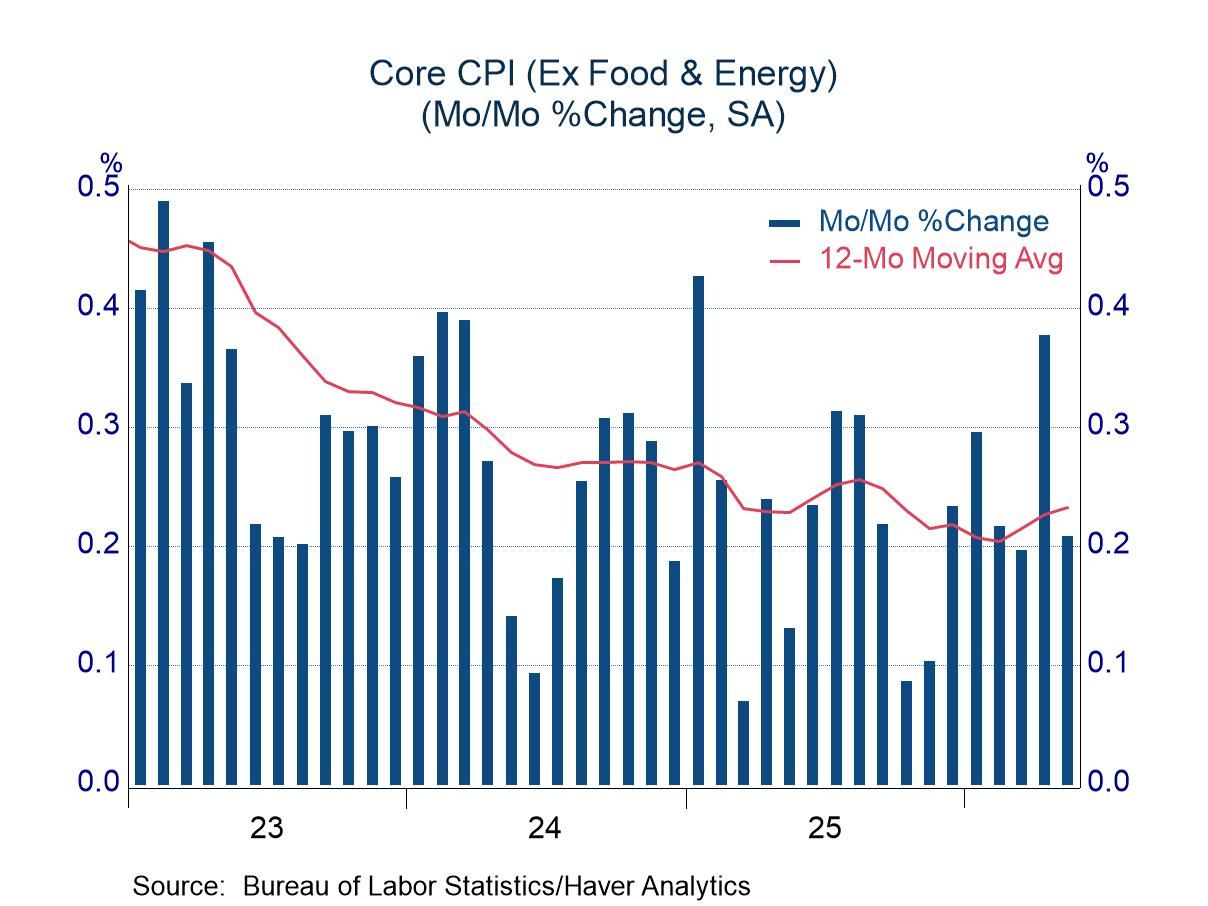

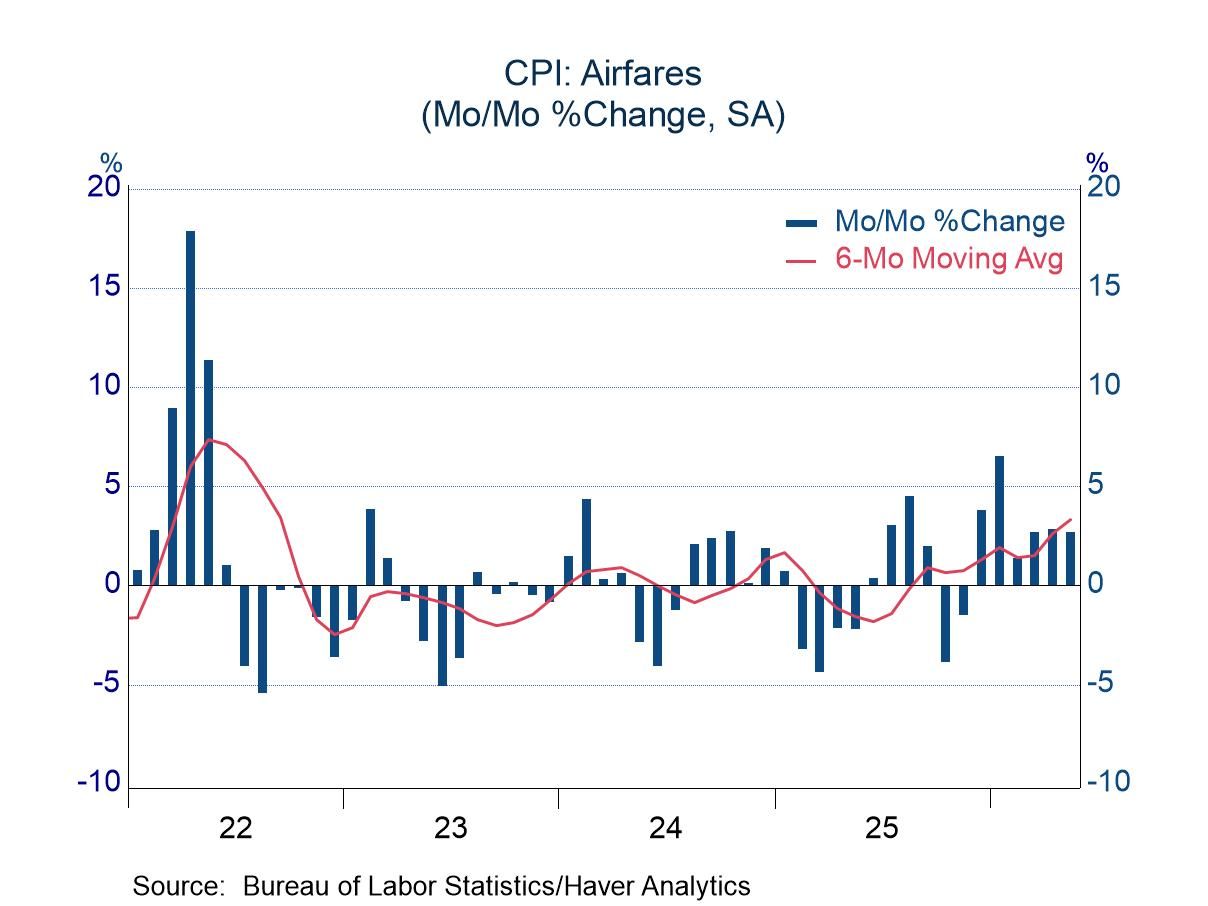

The core CPI (excluding food and energy) rose 0.2%, less than the expected increase of 0.3% and a reading in the middle of the recent range. A jump of 0.4% in the prior month raised the possibility that elevated energy prices might be feeding through to prices in other sectors. However, the subdued advance in May hints at little pass-through thus far. Airfares also provide encouragement on this issue. Airline tickets are highly sensitive to fuel charges, but fare increases in recent months have not shown a noticeable acceleration. The average increase of 2.7% in airline tickets, although hardly slow, was slower than the jump of 3.9% in the first two months of the year, before the surge in energy prices. Airfares tend to move in waves, showing periods of brisk increases followed by months of discounts.

Within the core component, goods prices were tame, posting a decline of 0.1%. Prices of medical goods contributed importantly to the soft reading, with a drop of 0.7%, marking the third consecutive decline after a soft trend in the year before this softness. The year-over-year change in medica-care goods totaled -1.8%. Prices of new motor vehicles fell 0.3% after a drop of 0.2% in the prior month, leaving a year-over-year change of only 0.5%.

Prices of core services rose 0.3% in May. The reading was not troubling when viewed in isolation, but it followed a jump of 0.5% in April and left the year-over-year increase at 3.4%, up from an average of 3.0% in the first three months of the year. Rent of primary residence has stirred in the past two months, increasing 0.5% in March and 0.4% in May, noticeably faster than the averages of 0.2% in the first three months of the year and in all of 2025. Not long ago, rents were an important factor behind elevated inflation readings. Results in April and May suggests that close monitoring is warranted.

The Consumer Price figures can be found in Haver's USECON database. The expectations figure is contained in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global