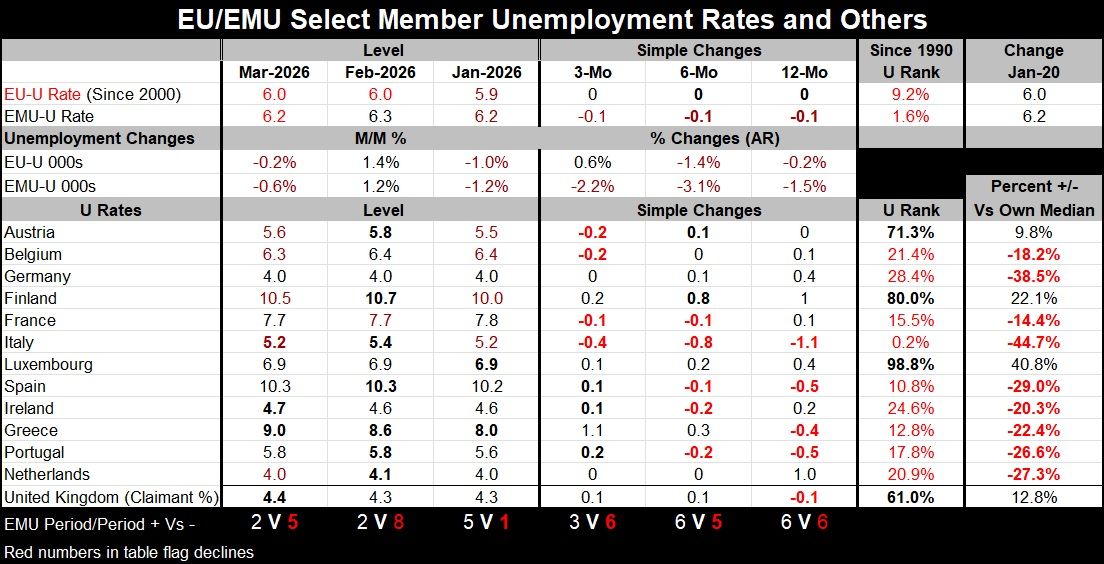

Low EMU Unemployment Rates Still Yield Monetary Restraint

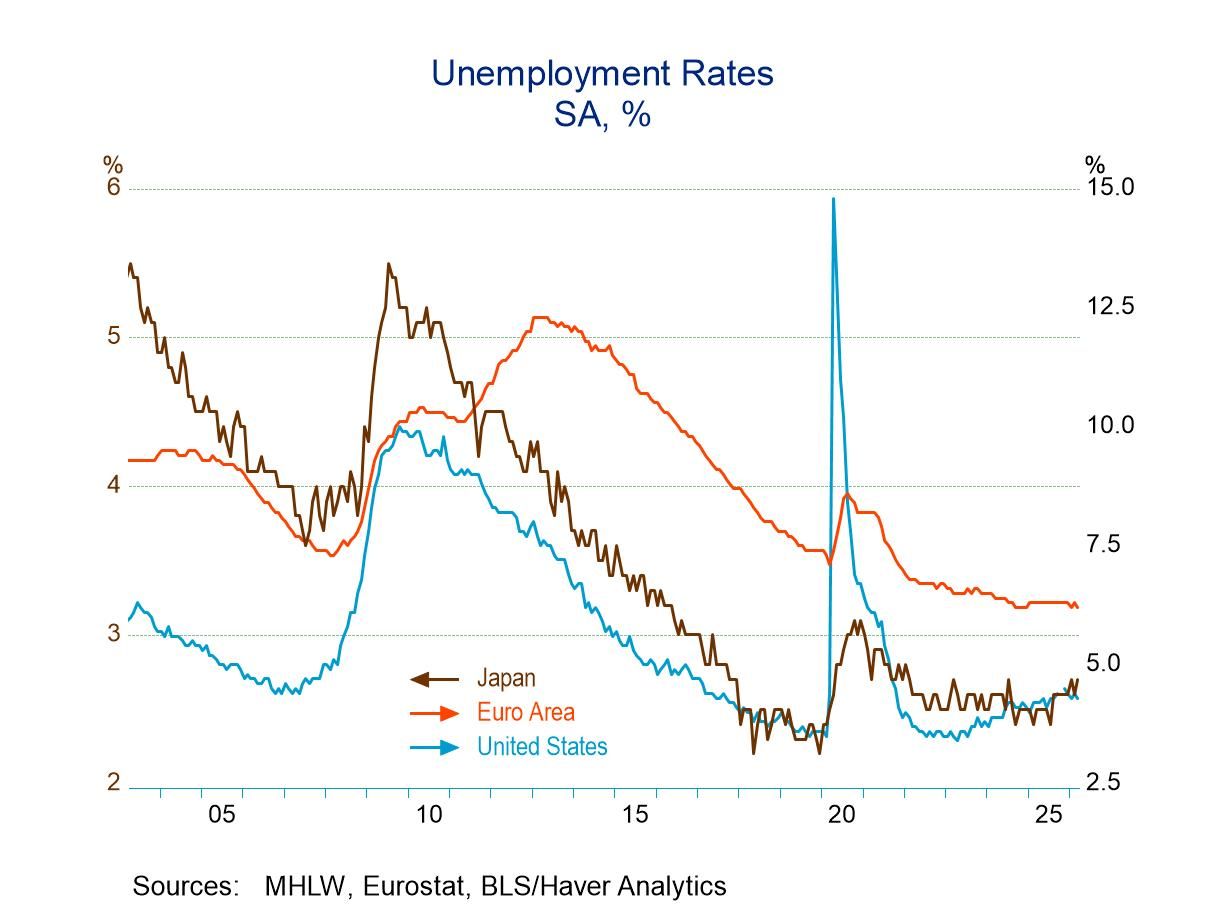

Unemployment rates are stable near all-time lows for EMU Unemployment rates in the European Monetary Union (EMU) continued to hover at the lowest level. The EMU all-time low unemployment rate is 6.2%, and that’s the number reported for March. There have been five of these 6.2% unemployment rates monthly in the history of the monetary union.

Unemployment rates in March saw declines in five of the 12 early reporting countries: the Netherlands, Italy, Finland, Belgium, and Austria. Over the last three months, there were net declines in the unemployment rates in four countries, while year-over-year once again four countries—though a different four—showed declines in the unemployment rate.

Unemployment rates, evaluated relative to their historic standings, have a median rank standing in their 33.6 percentile. That is the median unemployment rank among these 12 countries; it shows that the unemployment rate is in the lower one-third of its historic rank. Among the 12 early reporting countries, only three failed to have unemployment rate rankings below their 30th percentile; those three are Austria with a 71.3 percentile ranking, Finland with an 80th percentile ranking, and Luxembourg with a 98.8 percentile ranking. So, there are three countries among these 12 that have relatively high unemployment rates compared to their histories, whereas the rest of the reporters have unemployment rates below their respective 30th percentiles.

Good, but not great, labor markets Clearly, the labor situation is in good hands; however, at the same time, inflation runs over the top of the ECB target, and with war in the Middle East and flurrying oil prices, inflation is going to climb higher. The ECB, like the Federal Reserve, finds itself in the awkward position of not wanting to raise rates because the economy is generating growth; on the other hand, growth seems somewhat fragile. The unemployment rate is low, and inflation has been overshooting, so the central bank is in a difficult position.

Are central banks awakening from their slumber? Despite the good news on the unemployment front, central banks have been wary not to raise interest rates to fend off inflation. Inflation can really be described as having been moved around by financial crises and shocks going back to the great financial crisis. That shock, coupled with the losses that it created, left a legacy of inflation discipline for a very long run, basically, right into the COVID-created recession. COVID weakened economies globally as they were shut down by government policies and then inflation spurted as result of stimulative monetary action and fiscal excess. After that experience, central banks kept stimulative policies on the books and tried to coax growth out of a wounded economy and maintain low unemployment rates, while tolerating inflation that was excessive relative to their targets, but that did not accelerate and did decline slowly—at least for a while. As a result, there's now a legacy of overshooting inflation and more question marks about central banks and their backbone than central bankers want to admit as inflation rises, and as they continue to watch and postpone acting.

ECB met and declared watchful waiting—not policy action At the recent meeting, the ECB policy statement admitted that “Longer-term inflation expectations remain well anchored, although inflation expectations over shorter horizons have moved up significantly.” They are following the model used in the U.S. to contend that long-term inflation expectations are still firmly anchored while they are only slipping away for the short term—a year ahead or so. However, to its credit, the ECB does refer to expectations having moved up significantly in the near term. This is something policy must be wary of, and it also must be wary that long-term expectations may have been damaged as well.

In her press conference, Christine Lagarde noted that the forward guidance from the ECB has several different elements: “There are sort of three anchors of what our reaction function is. So first of all, to remind you: target is 2% medium term, number one. Number two: symmetry. We discussed that today and we reaffirmed it. Number three: our reaction will depend on the type of deviation from target that we observe. Is it large and sustainable?”

"The increase in energy prices will keep inflation well above 2% in the near term. As the period of high energy prices extends, the likely impact on broader inflation through indirect and second-round effects intensifies. We will therefore closely monitor the size and persistence of the energy price surge, and how it feeds through to price and wage setting, inflation expectations and overall economic dynamics." (Source here).

The road they kick the can down is getting narrower So, we are in store for more watchful waiting. Central bankers can feel that the flexibility is closing in on them. There's been a long period in which post financial crisis and post-COVID events helped to keep inflation under control, but now we're getting into a situation where it may be harder to keep control of inflation, especially since central bank credibility has been eroded by a long period of target misses. Two wars are in progress, and fiscal excess is the order of the day. So why not wait longer?

No eager-beaver rate hikers No central bank seems eager to undertake this new challenge; however, they seem to be circling around the policy change and preparing to do something they haven't done in a long time, which would be to raise interest rates. Last time, in the wake of COVID, the central banks raised interest rates they waited too long to hike them, calling the situation of inflation temporary or transitory. Once again, the central banks see the oil price shock as something that is temporary; however, it's also severe, and while it's temporary, it could turn out to be ‘temporary’ but fairly long-lasting, making it harder to ignore or for a central bank that plans to ‘look through.’

Some act, some talk, some just look... As I noted in the report on money supplies yesterday, the current practice of trying to look through this supply shock is creating an overshoot of money supply as we have money supply accelerations brewing in the U.S., the U.K., and the European Monetary Union. However, one of the rules from the 1970s was to not accommodate an oil price shock. Unfortunately, the practice of ‘looking through’ a supply shock—which means holding interest rates steady—is at the same time encouraging acceleration in the money supply, which looks accommodative to me. I don't see any evidence that central bankers have recognized the contradiction implied by these policies; it's something we should keep an eye on.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia