Global| Apr 29 2026

Global| Apr 29 2026Globally, Money Supplies Accelerate... No Problemo?

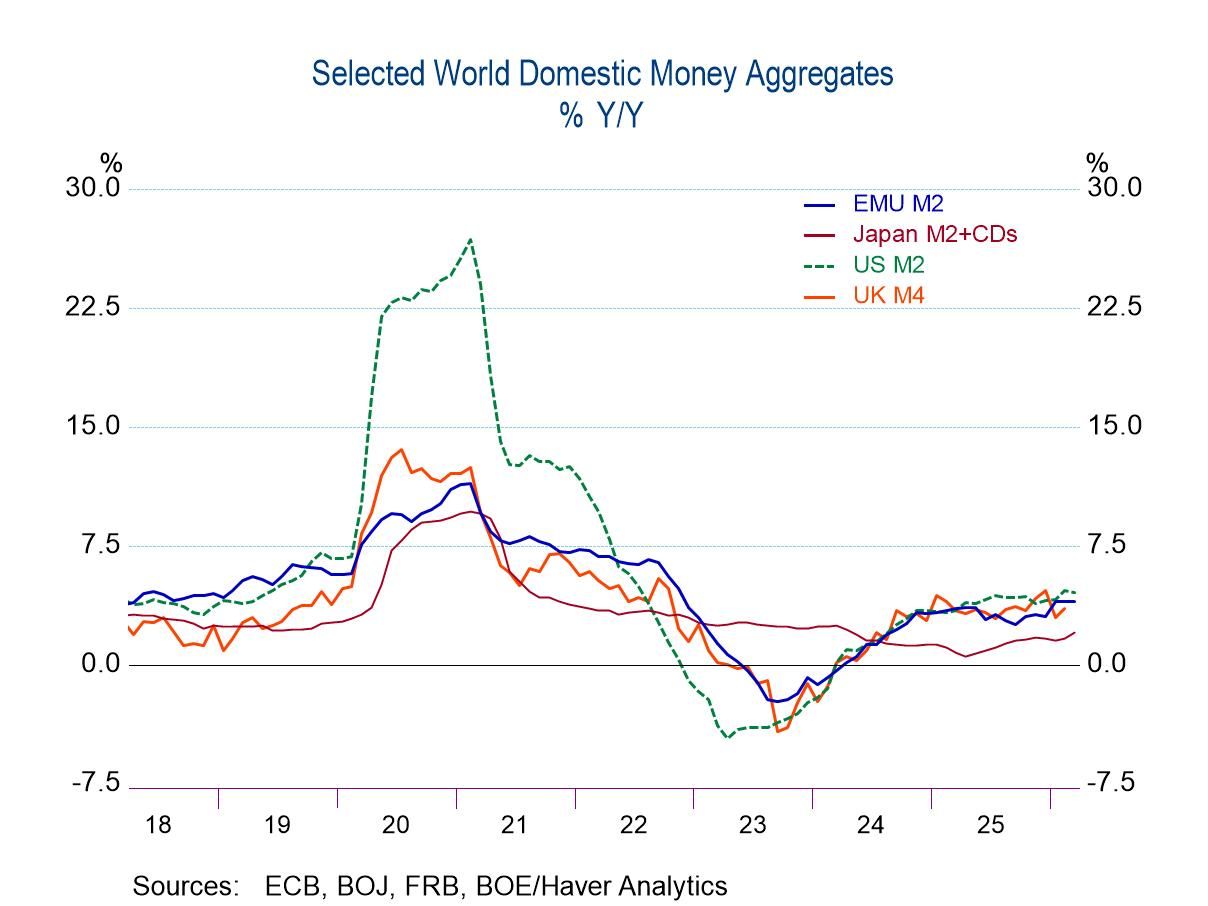

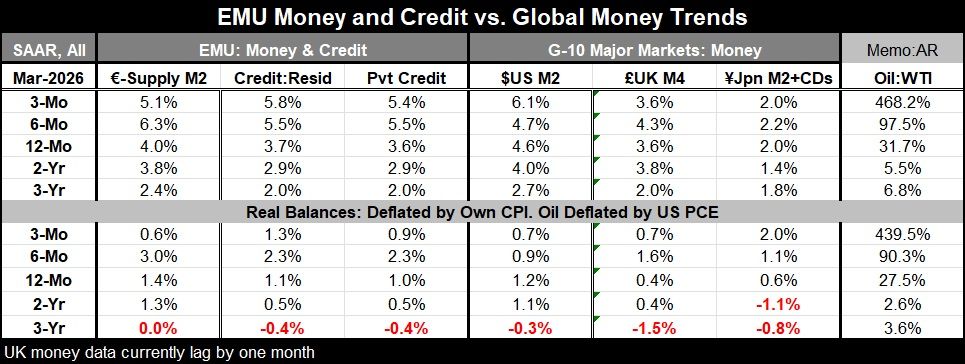

Globally, money supplies are accelerating. Three- and six-month money growth rates equal or exceed the year-on-year pace everywhere, and the 12-month growth rates accelerate over the recent 12 months compared to the 12-month pace of one year ago—except for the United Kingdom, where data lag by one month. This deviation may amount to the lack of topicality since money, credit, and inflation all are caught in an updraft prompted by rising oil prices. The oil price (Brent) is up at a 468% annual rate over three months, and over 12 months the oil price is up by 31.7%, compared to a 5.5% rise over 12 months one-year ago.

Rising oil prices do NOT create inflation Now we all know that rising oil prices do not create inflation. So, thankfully, the 468% rise in oil prices is not driving up the inflation rate. But unfortunately, it is helping to drive up the price level. So, we are drawing a distinction between the price level and the inflation rate.

The year-over-year change in a price metric, like the CPI, is just that: the year-on-year gain. We often refer to this as ‘THE’ inflation rate. But that is only if the price level was at—and continued to rise at (about)—that same pace. Inflation is an ongoing rise in the price level. No one in their right mind thinks oil prices are going to rise by 468% year-over-year persistently. But of course, oil is a cost to producers and a price to consumers. It is a price that must be paid and cost that must be borne. The question is how much this bump-up in oil prices will contribute to the prices of the items we track in our various national price indexes in the future. Here I will refer to the CPI as the price index. And then we ask if that one-time rise in the relative price of oil will continue to bump up prices by the same amount month-after-month in the future. If it is, it is creating inflation. If not, it is creating a realignment of relative prices. The rise in relative prices is real. It may be painful to some and remunerative to others. The effects are complex.

But the spike in oil prices is not inflation. Even though we are tracking an unknown price rise that is continuing to waffle, I will speak of it as though we know the ultimate rise and speak of that as a one-time surge.

Expressed in this way, you should be able to see the oil price spurt as painful and as something that may be a temporary boost to inflation. If the price stays high, it will boost the price level based on the pass-through by commodity. After the oil price spurt, prices may be higher, but inflation will go back to ‘where it was.’

But all that happens if and only if monetary policy does not accommodate—does not monetize—the rise in oil prices. Unfortunately, we see money supplies are accelerating. Central banks have stepped up their rate of printing money as oil prices have risen, in order to stabilize interest rates. Printing more money, or increasing the money stock faster, is inflationary.

A dilemma Everywhere central banks have taken the bait, and to cushion the impact on oil prices, they are letting money supplies accelerate. They do this because of a focus on interest rates, as monetary policy has a ‘rule’ that has been developed that monetary policy should not respond to supply shocks. Should money supply respond and accelerate? Well, the answer to that is clear: no. So, we have a dilemma.

Supply-demand argument Actually, the supply side edict is more complicated. Even those who note the monetary policy can’t solve supply problems realize that if a price spike is large enough or lasts long enough, it might, in the short run, impact prices with enough force to affect inflation expectations. Yet, for now we see no acknowledgement of this dilemma.

The expectations argument is the more sophisticated modern approach. Unfortunately, it refers to concepts we do not readily observe. Money supply growth, on the other hand we can measure. We see that money supply is accelerating, and that should make us worry about inflation. That in turn should, through one of several possible channels, get central banks to reign in money supply growth. To do that, they have to stop all this talk of ‘looking through’ the oil price increase, and they have to at least consider raising rates now. While the ECB and BOE have referred to this as a policy choice, the Federal Reserve in the U.S. has been far more circumspect and has just approved the election of a new chairman who thinks he can cut rates. I wonder whether, once he takes the helm at the Fed, he will continue to hold that view?

Economists are not watching money supply the way they used to. Central bankers need to have their eyes open as to the inflation risk, especially in the post Covid period, after which inflation targets had been consistently muddled by overshooting inflation.

Denial takes on many forms. The lesson learned is about money supply. The lesson is about not accommodating shocks to lessen their impact. But the focus on interest rates has muddied the meaning of that lesson in practice.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief