Japan Indicators: Strong Economy—Still, Large Question Marks

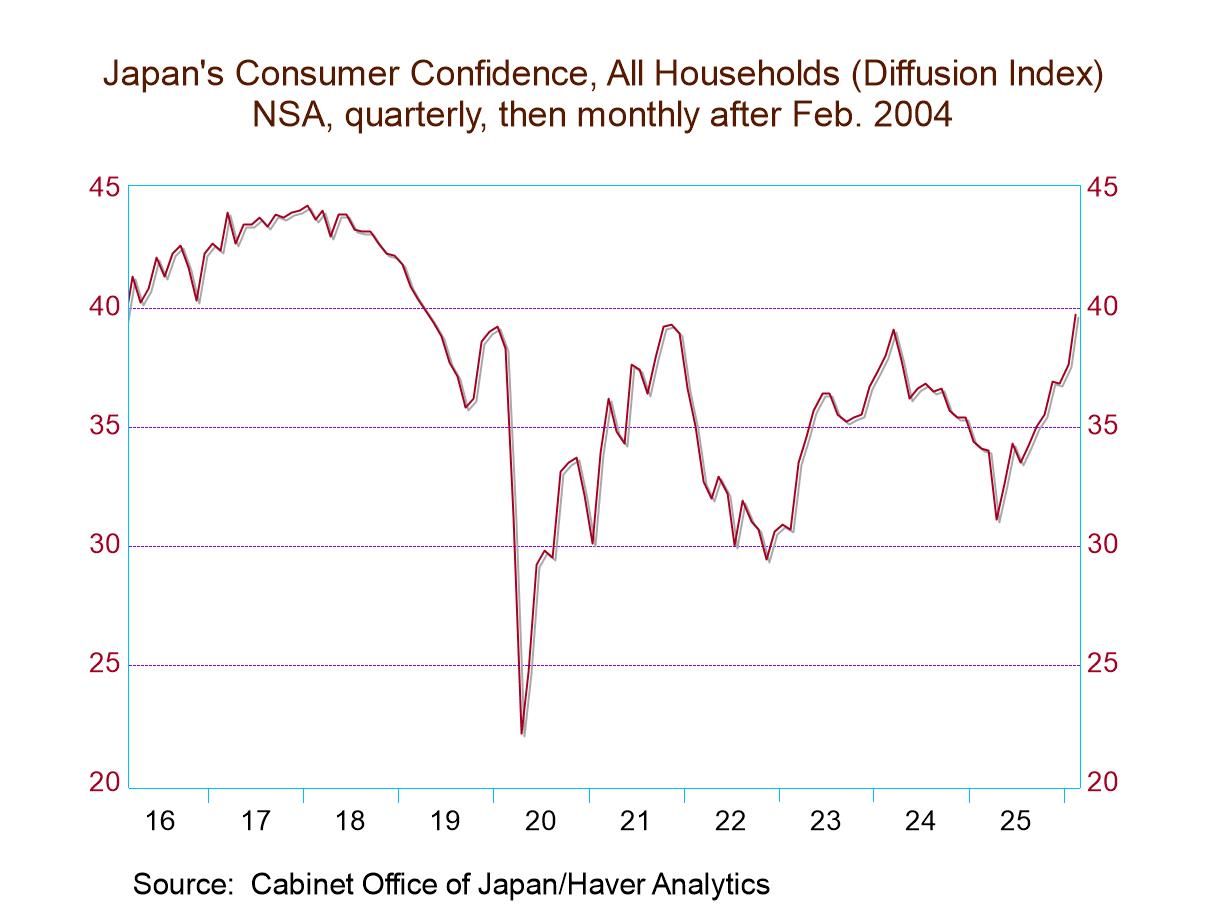

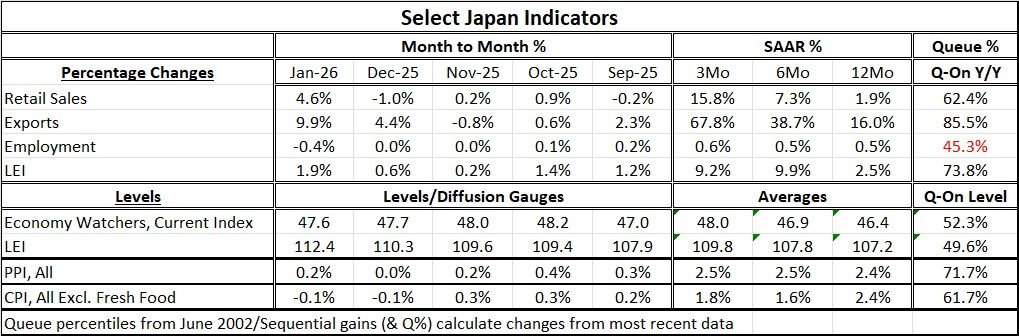

Japan's economy may not be firing on all cylinders, but the economy is looking pretty firm, and consumer confidence is just pushing up through an area that has defined several of its post-COVID peaks. Inflation in Japan is uncomfortable. The PPI index rose 0.2% in January and is running at 2.4% year-over-year. The headline CPI for January declined by 0.1% and is running at a 2.4% annual rate, above the Bank of Japan’s preferred target. However, it only has a 61.7 percentile standing compared to a 71.7 percentile standing for the PPI—above its median but not terribly high on data back to 2006.

Retail sales: Key Japan activity variables are showing sustained expansion. Retail sales in January rose by a sharp 4.6%. The sequential growth rate for retail sales mushrooms from a 1.9% pace over 12 months to a 7.3% pace over six months to 15.8% pace over three months. That’s very solid and extremely strong.

Exports: But with the yen weak on global exchange markets, Japan's exports rose by 9.9% in January. The sequential growth rate for exports is 16% over 12 months, which jumps to a 38.7% pace over six months and then jumps again to a 67.8% annual rate over three months. These are stunningly strong figures.

Jobs: Employment in Japan continues to show month-to-month gains, but the gains are not historically strong, even though the sequential performance is sound at 0.5% growth over 12 months and picking up to 0.6% at an annual rate over three months. That’s not bad for a country with fading demographics. However, the standing for employment is only at its 45th percentile, putting it below its median, which occurs at a ranking of 50%. On the other hand, the ranking is not far below its median, with its 45.3 percentile standing.

LEI: Japan's leading economic index rose by 1.9% in January, accelerating from its December increase of 0.6%. Again, the sequential growth rates for the LEI are strong and hint at acceleration, with a 2.5% gain over 12 months, a 9.9% annual rate gain over six months, a pace that is nearly maintained over three months, where the growth rate comes in at a nearly identical 9.2%.

Surveys: The LEI, viewed as a level, is showing ongoing gains and has a historic standing that is near its historic median. The economy watchers index has weakened in the past few months, but the sequential averages show ongoing upward momentum and a historic ranking above its median at a standing in its 52nd percentile.

Inflation: The inflation numbers are the ‘fly in the ointment’ for Japan, although neither the PPI nor the CPI headline (headline excluding fresh food) shows a tendency - a strong tendency - to accelerate. However, there's a war in the Middle East. Oil prices are going up, and that’s going to hit Japan hard — and it’s going to have an inflation effect.

What will central bankers do? One of the key questions moving forward is how central banks are going to deal with the inflation effects from oil, because while it clearly gives a supply shock, it's a relatively large one and nobody is sure how long-lived it's going to be and how much of this supply shock will get into the core inflation measures beyond just the headline.

Summing up The big argument up to this point in Japan has been about the Bank of Japan and whether it's going to raise rates, with inflation above its target and interest rates clearly below a level that would be considered normalization. That is still a goal, and as the economy gets stronger, the BOJ should try harder for normalization. Japan also has a new Prime Minister who just also won a snap election with a large majority. She is looking to engage fiscal policy, but fiscal policy in Japan's current economic and inflation conditions may not be the right tact for Japanese stability. Special industrial policy might work better, and the focus may actually shift there. Japan does have large fiscal deficits and massive accumulated fiscal debt, even though it owes most of the debt to itself—to its own people. Still, the possibility of something going wrong means the possibility of something going wrong that could have a massive impact on the economy, so playing the fiscal policy game carefully and running the proper monetary policy is going to be important in Japan. The prospect of doing that correctly has been made more complicated by the yen’s ongoing weakness and by surging oil prices. It's a global environment that has become more treacherous for policymakers and even those in Japan where the economy is performing quite well.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global