Inflation Tamed in France’s ‘Too-Early’ January Inflation Report

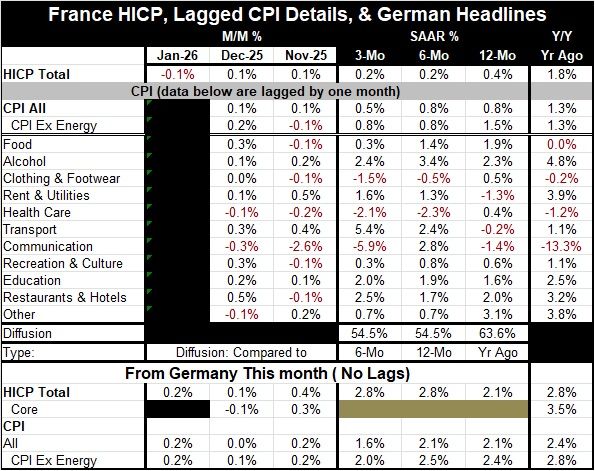

I have offered the table (below) as a presentation of French inflation statistics that is ‘too early’ largely because the report comes with a headline and without supporting detail. But the headline is too intriguing to wait for the details to emerge. To try to bridge that gap, I present the French detailed data for the CPI with the trends calculated based on a one-month lag. I also supplement that with the current report from Germany where the topical HICP reading for January is available, as it is for France. But Germany has also issued its domestic CPI data with detail. So, I present the domestic CPI trends without lag for Germany as a way to gain some better understanding about what's going on with inflation in the euro area and to gain perspective on France.

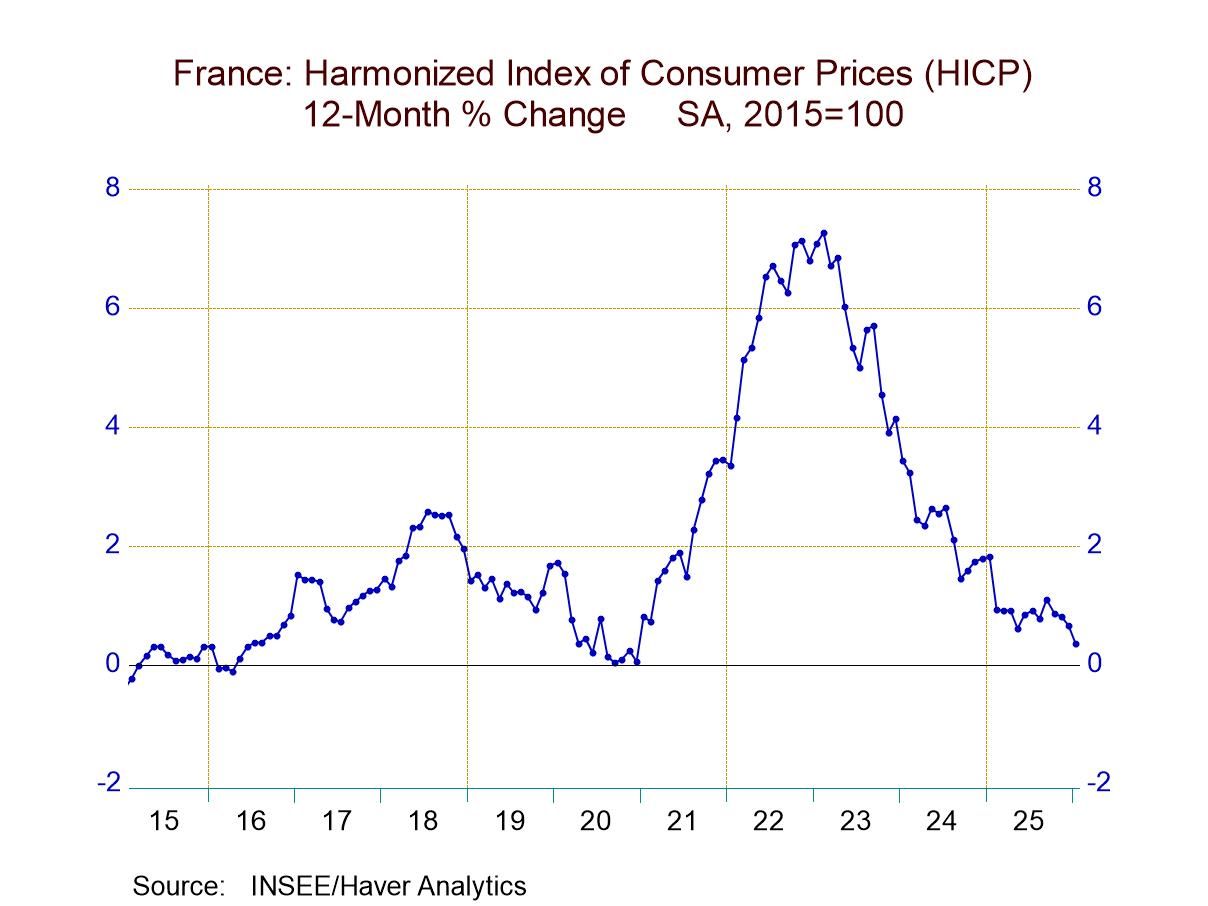

French-German comparisons; French results Of course, Germany is not France. We can't simply assume that the trends that we're seeing in Germany in January will translate through to France. But what we can do is notice what similarity/difference is there and point out that the sharp lowering of inflation in France is a French phenomenon and not a phenomenon that is shared by Germany. Therefore, the trend is not likely broadly applicable to the European Monetary Union. French inflation is running at only 0.4% over 12 months (!), annual rates of 0.2% over six months and three months; these are exceptionally low rates of inflation. In January, the French HICP index fell month-to-month by 0.1%.

German trends The German behavior is not really similar to this with the HICP at 2.1% over 12 months and then rising to annual rates of 2.8% over three months and six months, substantially similar to the sorts of numbers reported for headline inflation in the United States. The German domestic CPI reports slightly improving trends with annual inflation at 2.1%, six-month inflation at 2.1% at an annual rate, and at 1.6% over three months, inflation is tucked inside of the ECB 2% target over three months. The German CPI excluding energy - the early proxy that we have for the core rate - is at 2.4% over 12 months, 2.5% over six months and then drops to 2% annualized over three months. The month-to-month German data have been well behaved but not as weak as the monthly inflation numbers for the HICP headline monthly in France.

Different inflation in France and Germany; but a similar trend? So we have two bits of evidence here: one is that French inflation has really been behaving and it's quite weak. The other is that while German inflation is running at a higher pace and generally above the ECB target, there are also signs that German inflation is starting to come down over more recent periods.

An unusual macroeconomic event… in progress These observations, in some sense, clash with the early PMI data that show widespread improving breadth in January across global manufacturing PMI reporters. Manufacturing is showing signs of firming while the inflation picture is showing signs of coming under control at least in the European Monetary Area. While we tend to think of growth and inflation as going hand-in-hand, that is of inflation as being pro-cyclical, that's not a rule, and we see a departure from that usual pattern in these unfolding data. Will they continue to unfold that way?

What do you believe? All of this raises questions as to whether the inflation portion is real, whether the manufacturing growth portion is real, or whether they are both real and that monetary policy has been able to, because of its careful implementation, support growth and help to bring inflation lower at the same time.

Conventional trend unfolding in the U.S. These are intriguing questions and we're going to continue to ask them and watch trends in the months ahead. The U.S., early in the year, has reported out a very strong manufacturing ISM value that also has shown some pressure in its pricing gauge, a more conventional hint that growth is picking up and inflation might be picking up along with it.

The tariff stick Of course, there's a lot to consider here, a lot of irons are in the fire, a lot of contrary policies being run. There is a big change in U.S. tariff policy with the U.S. using the big stick and geopolitical relationships are resetting as well, with the two effects having some interaction with one another creating some difficulty for analysis.

Growth warming up in the U.S., and a new Fed chair… in waiting U.S. economy is showing signs of some significant pickup in growth in a recent ISM report on manufacturing. Inflation, that has not showed much tendency to decline recently, continues to run over the top of the Fed's target; however, there's been a new Federal Reserve Chairman nominated and there's a great deal of talk and discussion in the U.S. about what that means. What will he bring to the table? Everyone knows full-well that the President has been looking to get interest rates reduced! Nonetheless he has promoted for Federal Reserve chairmanship a former FOMC member with the known voting record who has tended to lean to the hawkish side of policy. This is a person who also supports shrinking the Fed’s balance sheet. As a result of these contrary pieces of analysis, there's a good deal of uncertainty in the U.S. about what the nomination of the new Fed chair, Kevin Warsh, is going to mean for policy. Once he has been approved, and Mr. Powell has departed in May, what then? It is indeed starting out to be an interesting year. Interesting trends and interesting unanswered questions.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global