Import & Export Prices: Generally Modest Changes

Summary

- Import prices have changed little in the past three years.

- Export prices were stable in 2023-24, but moved higher in 2025.

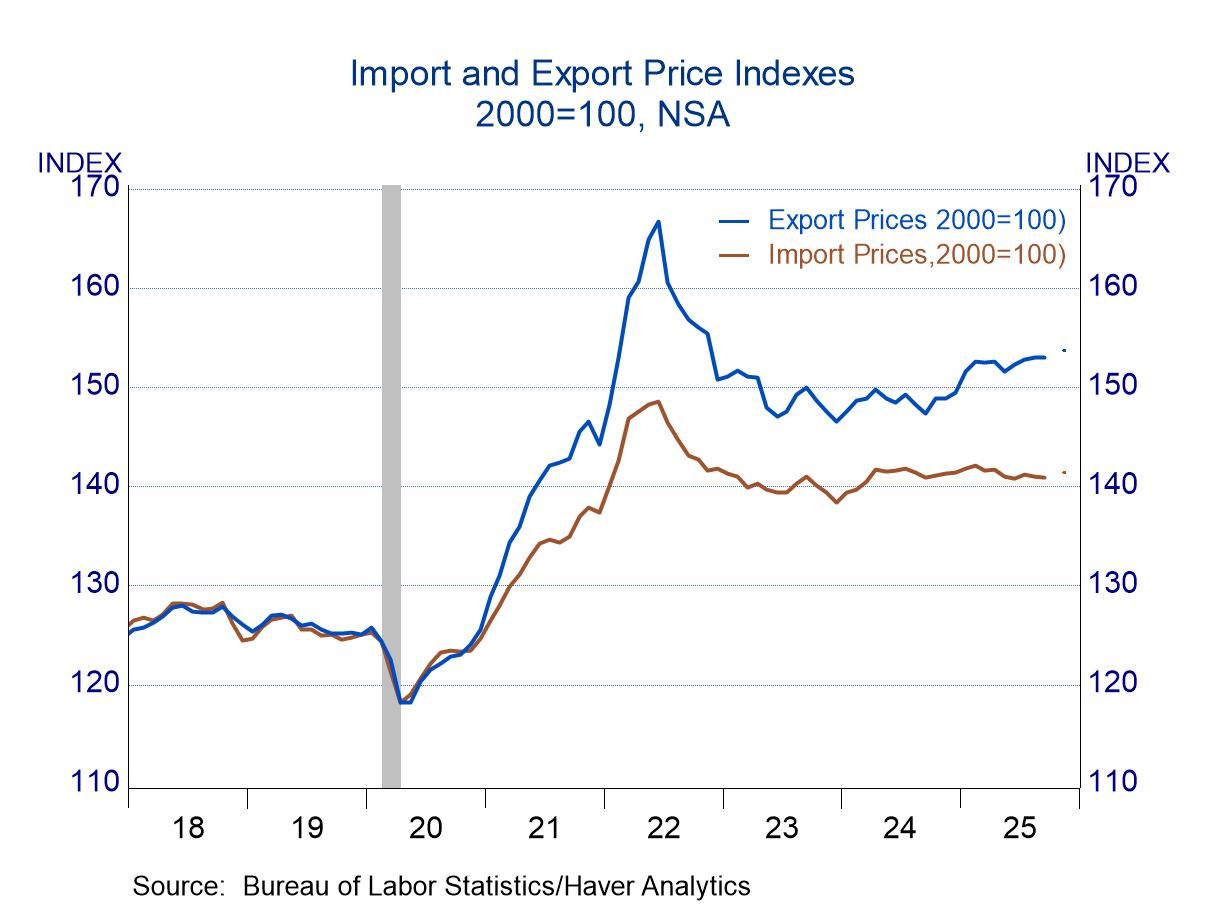

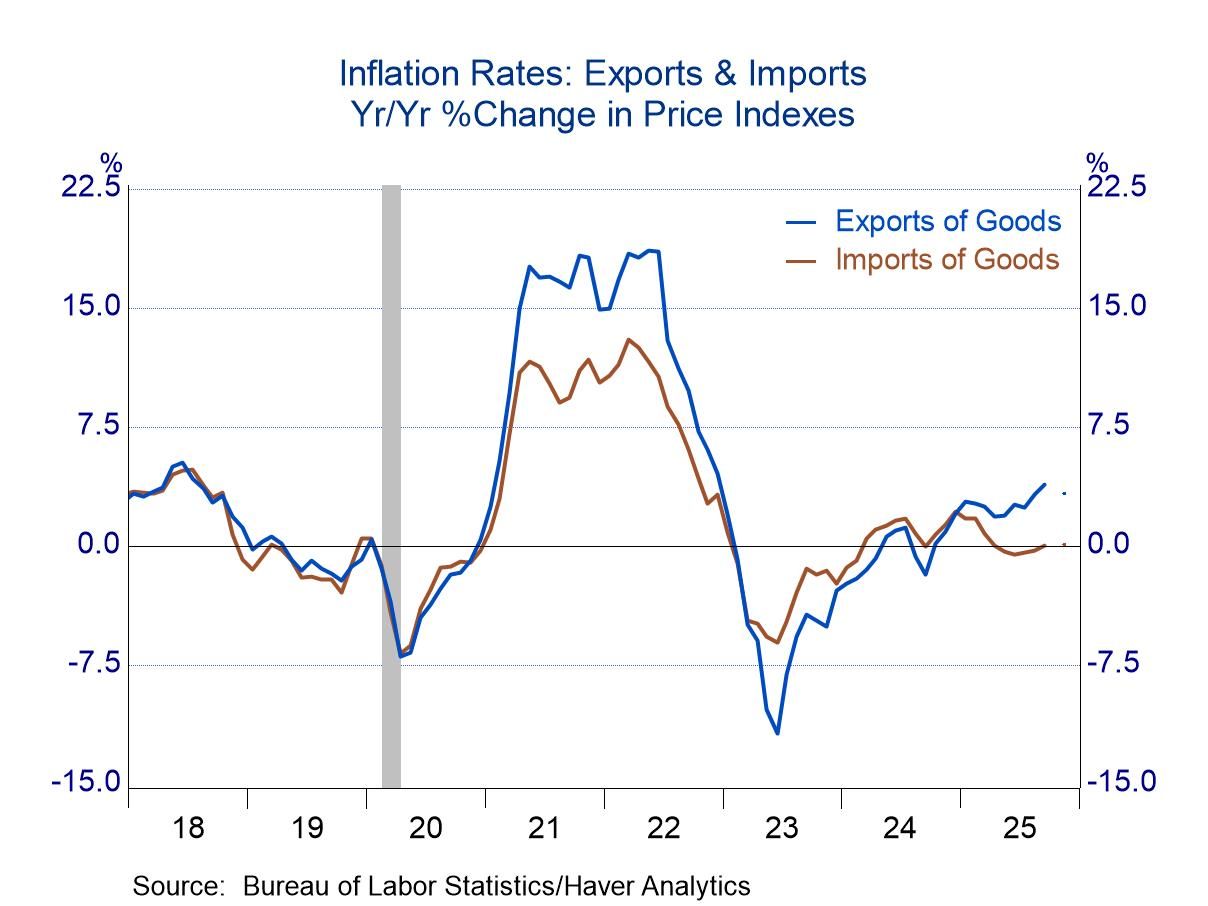

The Bureau of Labor Statistics did not publish a report on export and import prices for October because of the government shutdown, and BLS was unable to construct statistics for October to include with the November report. The charts above have a gap in October, and the November figures are represented by a small dot.

Import prices have been remarkably stable in the past three years, as shown by the sideways movement in the level of the import price index (left chart). Focusing on percent changes (i.e. inflation rates) rather than the level of the index shows deflation in 2023 and early 2024 followed by higher prices more recently (right chart). Still, the net change in the past 12 months has totaled only 0.1% and the cumulative change in the past three years amounted to a decline of 0.4%.

A calm environment in the energy sector has helped to restrain import prices, as the price of crude oil showed little change in 2023 and 2024 and declined in 2025. Import prices excluding petroleum products have increased in recent years, but the changes have been modest: 0.9 in the past 12 months and 1.3% in the past three years.

The non-oil components of import prices have traced various patterns in recent years, but shifts have been largely offsetting. Prices of food and autos increased noticeably in 2023 and 2024, but they gave back much of those increases in 2025. Prices of capital goods were stable in 2023 and 2024, but they started to increase in 2025. Prices of consumer goods have been volatile, showing bursts of higher prices followed by discounting, leaving a modest net increase in the past three years.

The calm energy environment also seemed to play a role on the export side, as the industrial supply category showed little net change in prices over 2023 and 2024 before jumping in early 2025. Food prices followed a similar pattern, showing two years of restraint before moving higher in 2025. These two categories account for much of the upward movement in overall export prices in 2025. Prices of consumer goods also started to move higher in 2025 after little net change in the prior two years. Prices of capital goods and automobiles have traced reasonably steady upward paths.

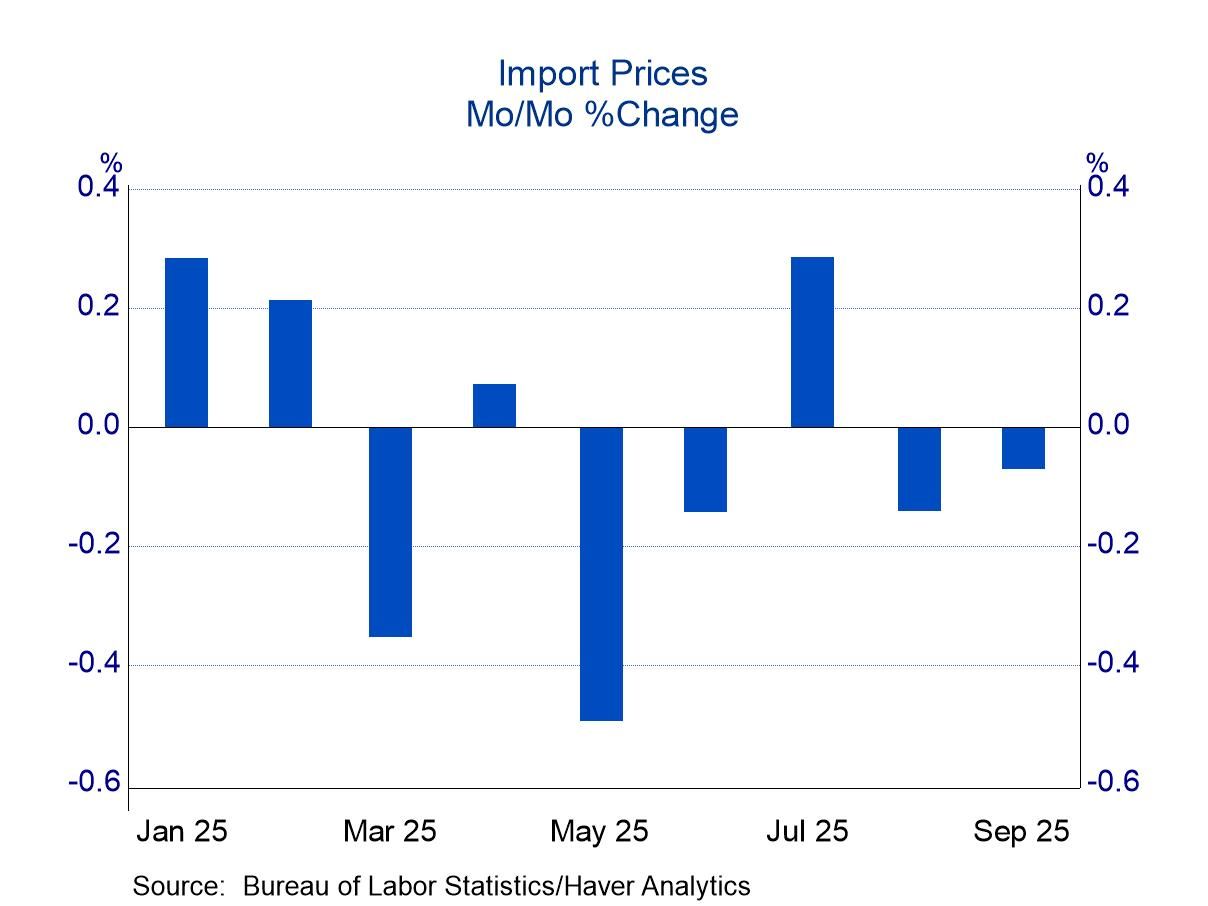

Many observers might try to use the import component of this report to gain insight into the effect of tariffs on prices. That will be difficult because the figures from this report are pre-tariff; there will be no independent upward pressure on prices in this report because of tariffs. In fact, one should look for lower import prices in searching for a tariff effect. That is, if a foreign exporter were to absorb the tariff burden, that would be accomplished by reducing the pre-tariff price in order to keep the after-tariff price steady.

Some exporters to the US may have made such efforts. The nearby chart shows the month-to-month change in import prices in 2025, and May and June both showed lower prices. These months were especially important because they followed the announcement by President Trump of marked increases in tariffs in April. Also, some of the downward pressure occurred in components that would be sensitive to price (autos and consumer goods). Of course, May and June might be too soon after the announcement of draconian tariffs for foreign exporters to assess and change their pricing strategy.

The chart on monthly changes ends in September because the absence of an October reading prevents the calculation of the month-to-month changes for October and November. However, the two-month change from September to November is easily calculated, and the increase of 0.4% suggests little or no effort to absorb the burden of tariffs.

These import and export price series are not seasonally adjusted; they can be found in Haver’s USECON database. Detailed figures are available in the USINT database. The expectations figure from the Action Economics Forecast Survey is in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global