Global| Jul 06 2026

Global| Jul 06 2026Globally S&P PMIs Gain a Modicum of Traction

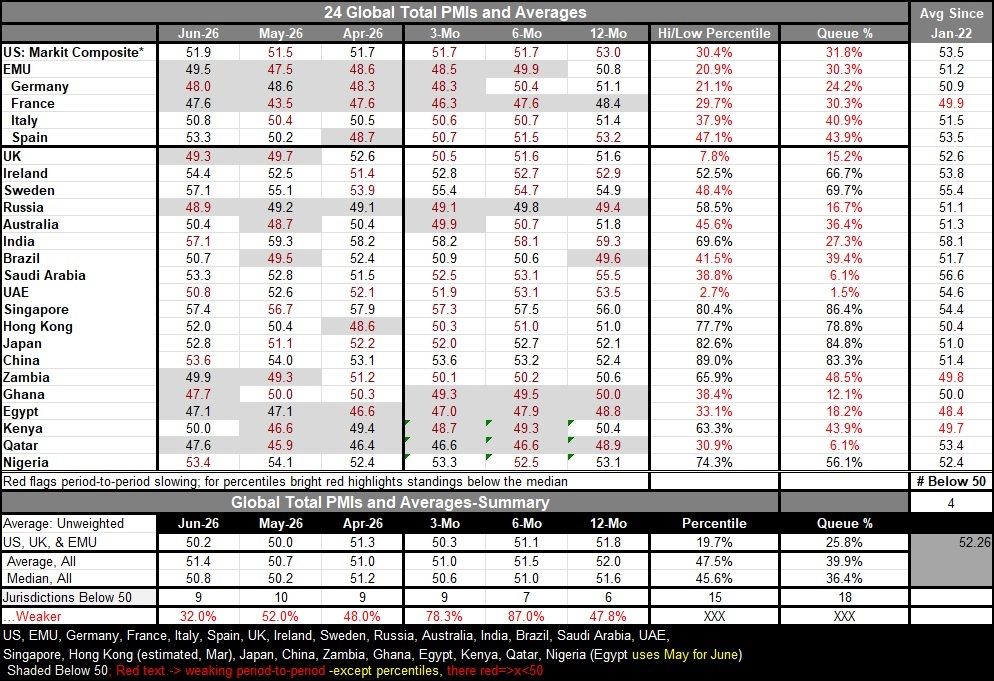

The global PMI data for a select group of 24 countries and their composites, provided on the graph, indicate a slight overall improvement for the total PMIs in June, with the service sector getting slightly stronger as the manufacturing sector is slightly weaker.

Conditions, however, remain uneven. The overall average for the PMI composite in June moved up to 51.4 from 50.7 in May, but the May reading had fallen from 51 in April. The median rose to 50.8 in June from 50.2 in May, but it had been at 51.2 in April. There continues to be a great deal of weakness and irregularity in the progression of the global economy—not surprisingly with the recent data coming during the period when oil prices had surged in the Strait of Hormuz had been closed. We now are seeing different conditions in force, and we'll see how much improvement occurs in July if the current global situation remains improved.

In June, nine of twenty-four reporters had PMI readings below 50, indicating contraction in economic activity. In May, there had been ten such reporters, while in April there had been nine. These readings, of course, are less than half of the reporters; however, it's still a very large proportion of the reporters where the total PMI gauges are indicating economic contraction. Over three months, there are nine reporters with average readings below 50; over six months, there are only seven; and over 12 months, there are six. This progression tells us that the situation has been getting worse rather than better.

Based on monthly data, the European Monetary Union, Germany, France, Russia, Egypt, and Qatar each recorded three consecutive months of readings below 50, indicating contraction in each of those months. Sequentially, over 12 months, six months, and three months, only France, Russia, Ghana, Egypt, and Qatar show consistent readings that average below 50 (based on raw data).

The queue standings of the levels reported by countries in June show only seven with standings above the 50th percentile; this means there are only seven countries whose PMIs in June are higher than their average back to January 2022. Not surprisingly with the recent events really focused on oil prices and the situation in the Middle East and the closure of the Strait of Hormuz, some of the weakest ranking readings are coming from oil producers in the Middle East such as Qatar (6.1%), the UAE (1.5%), Saudi Arabia (6.1%), and Egypt (18.2%). Clearly, the interruption of the oil flow and war damage has had an outsized impact on these data.

However, quite apart from the current situation and the closure of the Strait, if we calculate the average PMI standing rather than the ranking just the average of the PMI total sector ranking, there are four countries that have averaged readings below 50 based on monthly data back to January 2022. Those countries are France, Zambia, Egypt, and Kenya. The average readings across all countries back to January 2022 is a reading of 52.3. The highest ranking during this previous period is from India; its ranking is at 58.1. Ironically, some of the strongest readings in the earlier period come from oil producers whose current rankings are so low such as Saudi Arabia at 56.6, the UAE at 54.6, and Qatar at 53.4.

There has been upward momentum this month, particularly in services, while manufacturing backtracked. However, the trend to improve conditions is no longer so clear. What is clear is that the outlook is going to depend upon whatever peace agreement proves durable involving Iran and traffic through the Strait of Hormuz. This conclusion is not rocket-science; it is obvious. And it's going to take close-watching because there have been so many missteps around alleged ceasefires and treaty discussions that we can't be very sure about what's going to play out in the future and what will last.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief