Asia| Jul 06 2026

Asia| Jul 06 2026Economic Letter from Asia: Woah, We’re Halfway There

In this week's Letter, we trace how an energy shock and a resilient AI upcycle shaped Asia through the first half of 2026 and weigh the risks that may define the second. The year opened hopeful on AI, though some feared stretched valuations, before the US-Iran conflict and a closed Strait of Hormuz shook the mood (chart 1). A later MoU eased energy prices and inflation fears, yet valuations largely held on AI optimism, despite bouts of reassessment. The oil surge hit import-reliant emerging Asia hardest, leaving India, Thailand and the Philippines doubly exposed through their Middle East sourcing (chart 2). Pass-through inflation, subsidies that some governments later pared back, and currency pressure followed, though resuming Strait traffic should ease these strains. Rising inflation then boxed in policymakers, straining already-stretched fiscal positions and limiting more pro-growth monetary policy stances in some economies (chart 3). Our latest Blue Chip survey found a slim majority reassessed the risk balance after oil fell, though the shifts stayed mild versus the June survey (chart 4). Most still rank upside inflation risk above downside employment risk, even as a slightly larger share now see the balance as more even. AI remains the region's key offset, with Taiwan and South Korea riding a sharp rise in memory and chip exports (chart 5). Malaysia and Thailand instead draw data centre FDI, so Asia gains from the buildout phase rather than the West's hoped-for productivity gains. We close on an uncertain second half, where a possible Super El Niño could revive food-driven inflation even as energy pressures fade (chart 6). Beyond that, an AI reassessment, fresh geopolitical flashpoints, trade tensions and the US midterms could each reshape the outlook.

The year thus far We began the year on a relatively hopeful note, buoyed by AI optimism and market valuations that reflected it, although some investors worried that valuations had become overstretched. The geopolitical mood shifted quickly in early January, however, when US military forces captured former Venezuelan leader Maduro, though the event did little to move markets (chart 1). A far greater shock came when the US-Iran conflict erupted in late February, closing the Strait of Hormuz and dealing a negative blow to global energy supplies. More recently, the US and Iran have reached a Memorandum of Understanding (MoU) aimed at ceasing hostilities and resuming trade flows through the Strait. This has allowed energy prices to ease, softening policymakers' concerns about energy-driven inflation. Even so, equity valuations have largely remained underpinned by AI optimism, albeit with interim bouts of reassessment and price retracement. This drew on repeated reports of strong growth along the AI supply chain, and on signs that supply could not keep pace with demand. This continued even as AI models with leapfrogging capabilities reached the public. At several points, the US government stepped in to rein in public access to some models, given security concerns about such immense capabilities falling into the wrong hands.

Chart 1: The US NASDAQ composite and world geopolitical risk

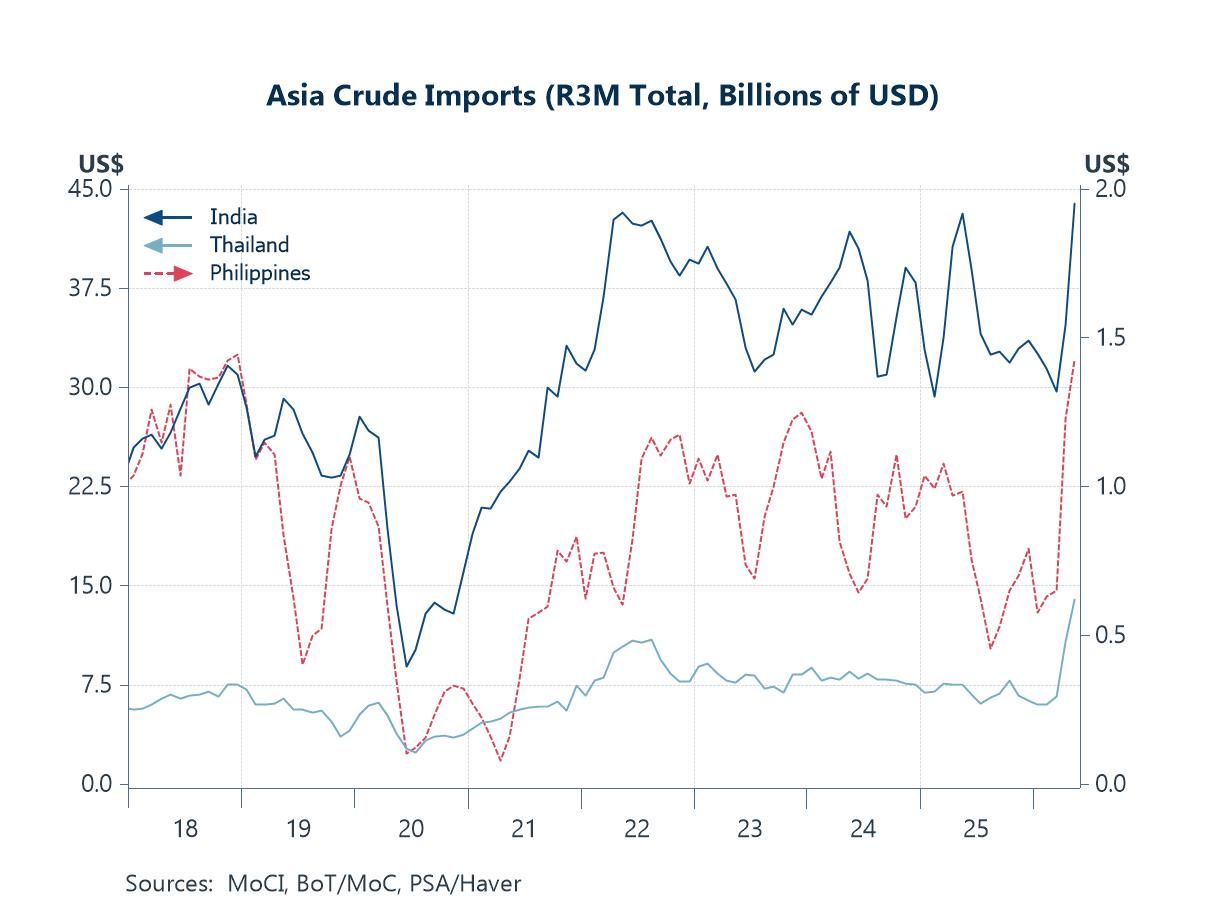

Oil impact on Asia Within emerging Asia, among the hardest hit by the oil surge are India, Thailand and the Philippines. These are relatively heavy net importers of crude oil, and they source most of that crude from the Middle East. That combination left them doubly exposed when the Strait of Hormuz closed (chart 2). The surge in oil prices also carries multiple, wider impacts. First, the higher cost of imported crude passes through to consumer inflation, leaving households with a heavier energy bill. Several governments have stepped in with energy subsidies to ease the consumer burden. That support has not proved indefinitely sustainable, as some governments eventually pared it back given the immense costs. In effect, subsidies shift some of the burden from consumers to the state, straining public finances. There is also a currency effect, since higher crude prices require more domestic currency to buy the same volume, weighing on the exchange rate. That said, other drivers of currency depreciation may also have been at play over the period. Trade flows through the Strait have recently picked up, with traffic gradually resuming. If the current truce and its conditions hold, these effects may ease before long. On the growth front, higher oil prices would not appear in volume-based measures. Their second-order effects on output would still come through, such as demand dampened by higher energy costs.

Chart 2: Asia crude imports

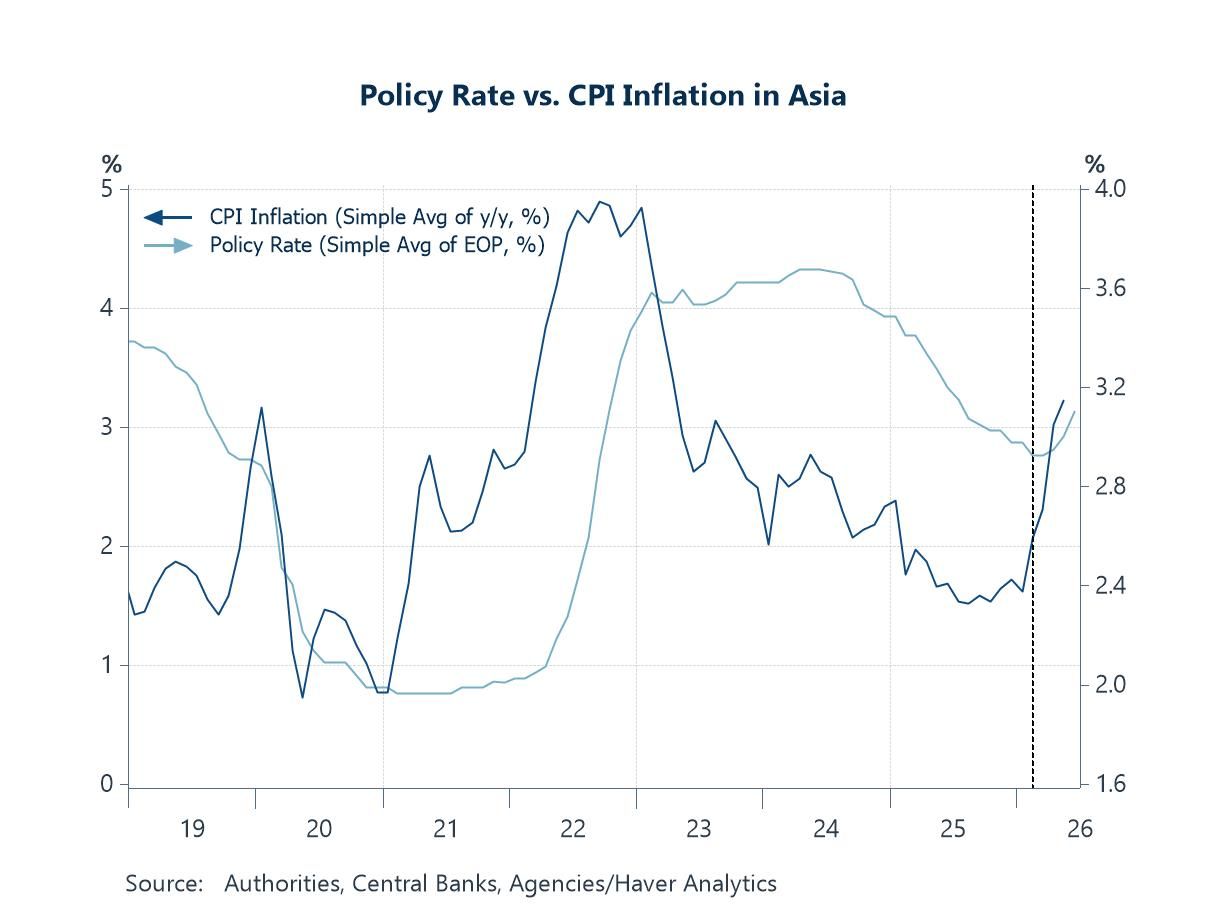

Inflation and monetary policy Higher crude oil prices drove inflation sharply higher across Asia and much of the world. That greatly complicated policymakers' task on both the fiscal and monetary fronts. On the fiscal side, several Asian governments were already facing pressures before the oil shock. These ranged from grand, fiscally costly policy pushes in Indonesia to calls for greater fiscal sustainability in Japan. Higher oil prices added a need for more support, further complicating their position. On the monetary side, previously pro-growth moves, such as rate cuts in India, looked riskier, as they threatened to stoke already-surging inflation (chart 3). That made further easing, or even holding current pro-growth settings, hard to sustain. The danger is sharper still if inflation expectations become unanchored, raising the risk of runaway inflation. The recent US-Iran de-escalation, and the crude price slump that followed, certainly help to ease the situation. One would expect so material a shift in the geopolitical backdrop to prompt a reassessment among policymakers and investors alike. Yet that was not entirely the case, based on our latest Blue Chip Financial Forecast survey, whose results we discuss in the next section.

Chart 3: Average CPI inflation and monetary policy rate in Asia

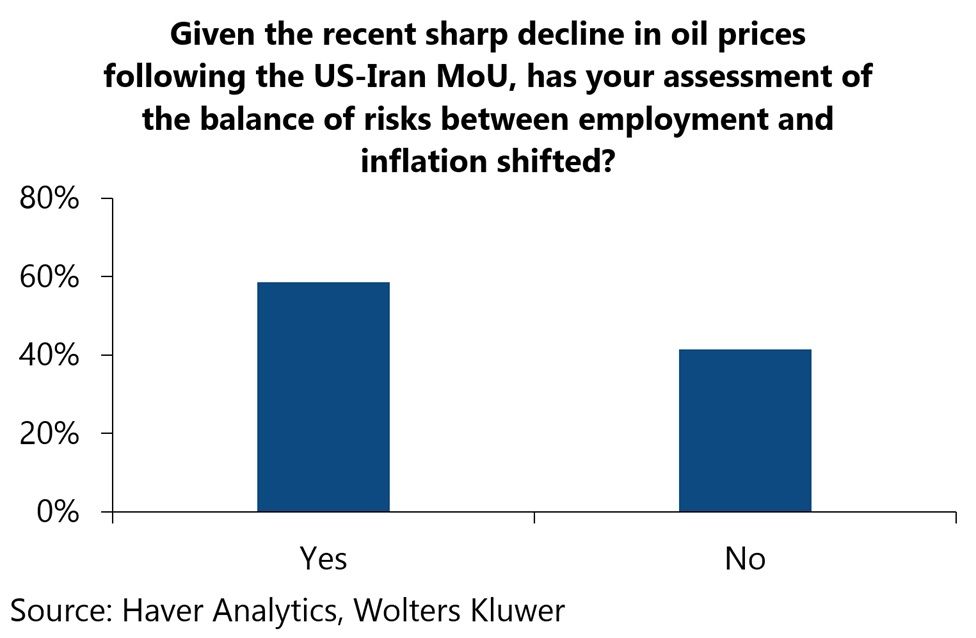

The latest Blue Chip survey results The recent US-Iran MoU has largely held, despite occasional flare-ups. Against that backdrop, and the sharp fall in oil prices that followed, we asked panellists to assess the balance of risks between employment and inflation. A slim majority (59%) said their assessment had shifted, while a non-trivial minority said it had not. Looking specifically at how US risk expectations moved, we find the shifts have been quite mild. That is relative to the June survey, which was conducted before the MoU. Even so, most panellists (65%) still see upside risks to inflation as the key risk, rather than downside risks to employment. Meanwhile, a slightly larger share than in June (23%) now see the risks as more balanced.

Chart 4: Blue Chip Financial Forecasts special question on US-Iran MoU

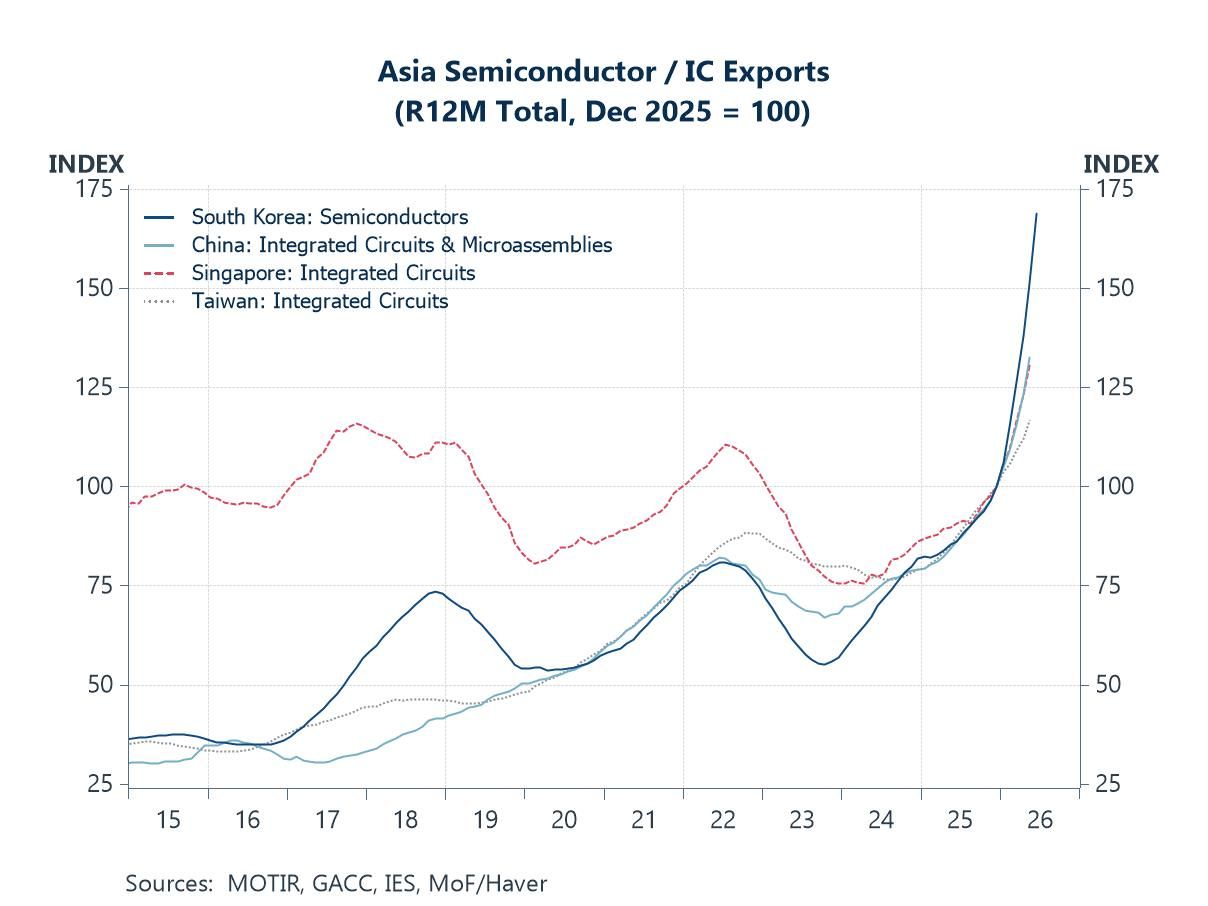

The AI upcycle and Asia We turn next to a key offset to the growth dampeners facing much of Asia. It stems from parts of the region being well positioned to capture the current AI upcycle. Advanced economies such as Taiwan and South Korea have benefited from strong demand for AI and related memory chips. This has driven a sharp rise in exports of such goods (chart 5). Those exports have propelled growth in these economies this year, at a pace faster than in previous years. Other economies, such as Malaysia and Thailand, are going through a data centre boom. They benefit through an additional channel beyond AI-related goods exports: robust FDI inflows. Foreign firms are driving these inflows as they expand their data centre footprint in the region. Other economies, including those in the West, hope to reap large productivity gains from the current jump in AI capabilities. By contrast, much of Asia's benefit comes from the ongoing buildout of the parts and infrastructure that the upcycle requires.

Chart 5: Semiconductor / integrated circuit exports in Asia

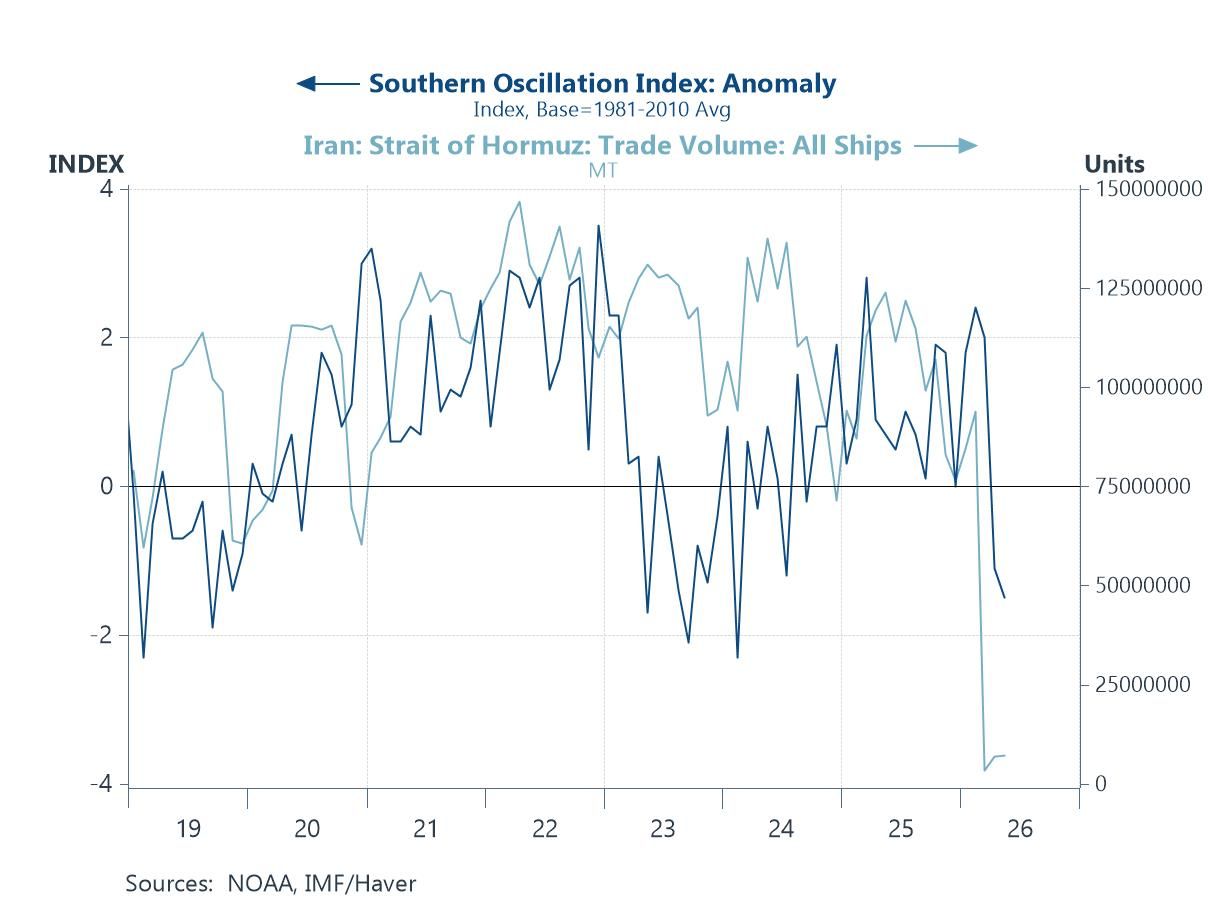

Watching H2 2026 Bringing it all together, the first half of the year has been shaped by two main drivers: the US-Iran conflict and the ongoing AI upcycle. What the overarching themes for Asia will be in the second half remains anyone's guess. For one, the threat of an imminent "Super El Niño" event (chart 6) could trigger a crop supply shock. That may reintroduce inflationary pressure, albeit through the food channel. On another front, market optimism around AI-related companies' revenues and spending still persists. Yet disruptions or new discoveries could emerge down the line, including some that sharply reduce the compute needed for a given output. Such developments may in time prompt investors to reassess their views. In addition, pockets of geopolitical pressure are still brimming in parts of the world, including the Middle East. These threaten to upend supply flows of oil, and of other crucial goods too. The trade front, though faded from focus in recent months, could become another flashpoint. It bears on growth and on bilateral relationships, especially those with the US. Finally, other events, such as the US midterm elections later this year, may also skew the global backdrop.

Chart 6: Southern Oscillation Index and Strait of Hormuz traffic

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief