Global| Mar 26 2026

Global| Mar 26 2026Globally Money Supplies Retain Hot Growth

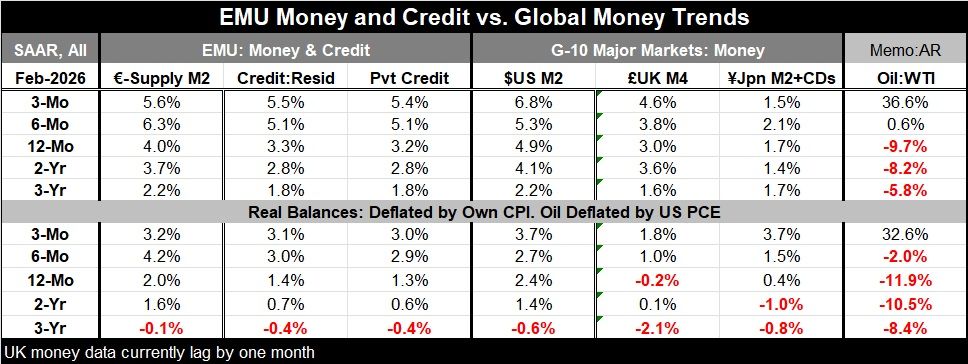

Current global money and credit trends Money supply growth accelerated in February over three months compared to six months in the United States and the United Kingdom. In the EMU, money growth backed down from a 6.3% growth rate over six months to a still hot 5.6% over three months. Japan, as always, was the exception, with money growth sinking to a weak 1.5% over three months from 2.1% over six months. And the Bank of Japan still has its sights on raising rates further and bringing the level of interest rates eventually to a normalized level. In the EMU, credit growth accelerated as private credit grew at a 5.4% pace over three months, up from 5.1% over six months.

Excessive money growth: Money and credit growth are excessive compared to what would seem to be equilibrium conditions. Those conditions right now have economic growth weak, in the region of 1% to 2%, and monetary targets are 2% all around. All of them are being exceeded—at least in terms of core inflation rates.

And yet the policy tilt had been toward more ease: Central banks had been making ready to cut rates again in their perceived long march back to normalcy for their key benchmark rates. But inflation has been over target since the wake of COVID either for headline inflation, core inflation, or both, depending on the country. Yet, central bankers have been looking to reduce interest rates to perceived long-run equilibrium norms even in the face of excessive inflation. This has been a remarkable and frustrating period for anyone who thought that 2% meant 2%. Central bankers have been engaged in a strange new calculus we could call Wimpy-nomics (in honor of Popeye’s friend) because they would gladly promise you 2% in the future for something excessive today—accompanied by rate cuts.

Bit-in-the-teeth-onomics: Even the Trump tariffs did not untrack this train of thought. It spawned more excuses about how it was temporary and could be ignored. The Iran war brought more of that until oil prices hit triple digits; that seems have sobered up some central bankers. Still, in recent central bank meetings the Fed gave us no clues on policy, while both the ECB and the BOE talked of likely hikes if the war was still engaged at the time of their next meetings. And some central bankers try to disabuse us of the notion that policy is not on a preconceived course and is data dependent.

Growth rules: Money growth is and has been excessive, and money growth rates have progressed to excessive norms over three months, six months, and even 12 months (in the U.S.). Full employment growth plus 2% should max out money growth; those metrics would put max money growth at 3% or 4%, depending on the country. Maybe U.S. productivity is in gear, and the U.S. can step that up. But so far, the demonstrable excess is inflation, soaking up the extra nominal GDP growth.

Back from the brink: The Iran war has brought policymakers back from the brink even if some won’t tell us what they think. ‘Data dependent’ does not begin to cut it because the question is about oil prices—how long they will stay elevated and how high they will go. The rear-view mirror will not answer that question, nor will it set out a reliable trend. So, the concept of data-dependency does not work here. Meanwhile, oil prices are surging, and Iran is refusing to roll over and play dead, even though its leaders have very few options—and none of them are good. The country has no cohesive military left, just a few pockets of some military capability and a population that, if it could, would overrun the leadership over the way it has been abused and steamrolled. Leadership has refused to give in, but if the regime falls, none of its leaders would survive a rebellion by the locals after the way they were treated.

The operative ‘model’: The ‘model’ for Iran is catastrophe theory. It will look like the regime is in power until its repressive dam breaks, and then it will be all over. Will the regime hold? That is hard to predict—it’s hard to know—because the regime might even survive. What markets need to know especially about is control of the Strait of Hormuz. Securing that strait is now the policy and military focus. Can the strait be secured if the regime holds on? That may be the critical question we need answered about Iran. The economics are not about money or inflation anymore. The future is about oil more than money, and that is why the future is so uncertain. War is simply not predictable. Money supply is. But even then, central banks may choose to not control it as they should, and as they have promised, as we have seen. Whenever a policymaker has a choice to make, one option is always the wrong one. Let’s hope that is not the one they pick.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief