German PPI Takes Partial Flight

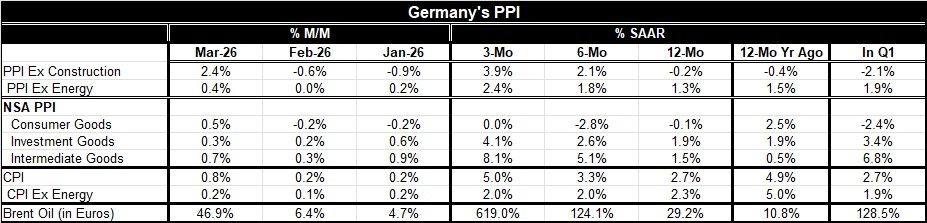

The German PPI rose by 2.4% month-to-month in March. That was, of course, boosted by oil prices as Brent crude soared, gaining 46.9% month-over-month (yikes!). However, very little of that got into German ex-energy prices, which did rise, but by only 0.4%. Still, do not be fooled by that ‘only.’ That 0.4% rise is the largest rise of that magnitude since February 2023—a period of about 2¼ years. So be wary of what might be in train here; 0.4% does not seem so large, but it annualizes to about a 5% pace.

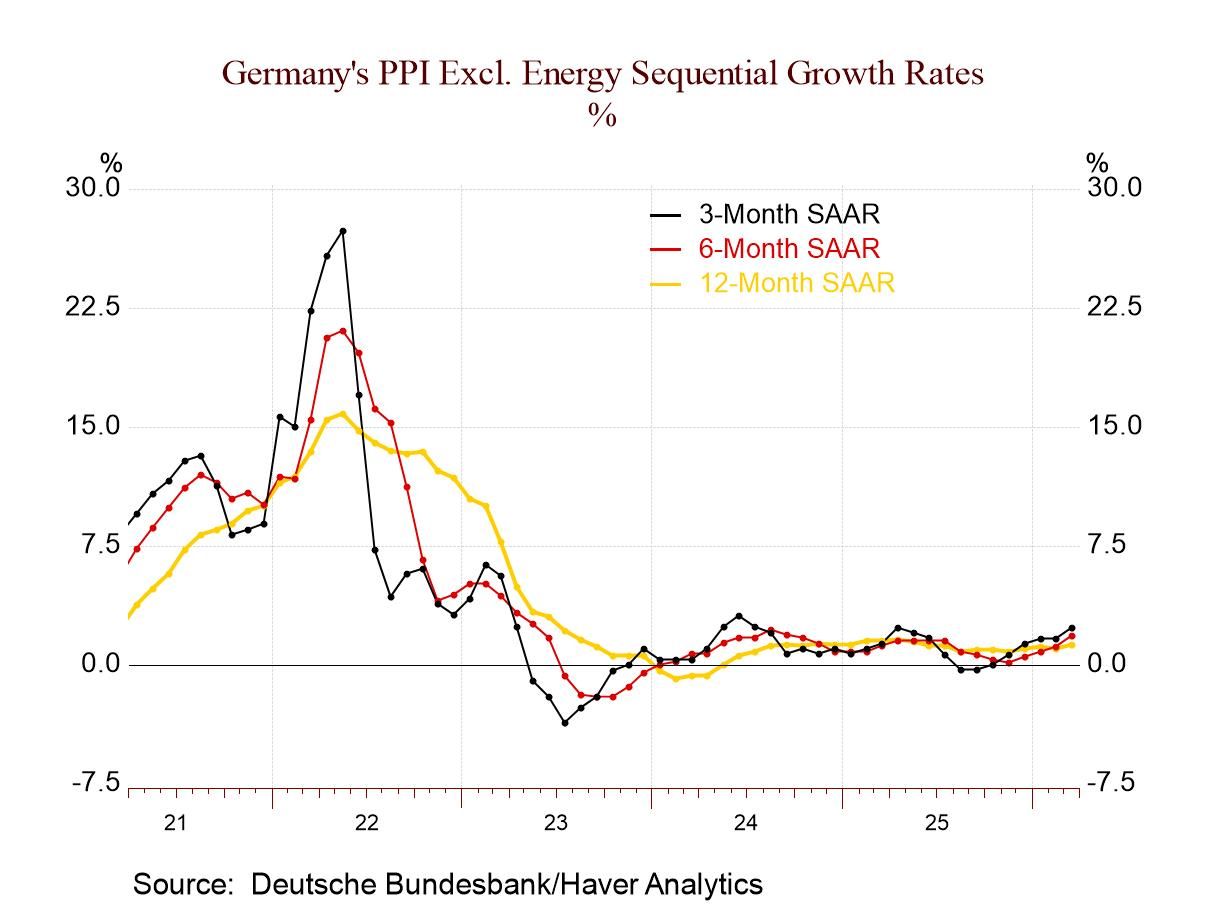

In addition, 12 months to six months to three months, the headline PPI is accelerating—from a 12-month drop, to a well-behaved 2.1% pace of expansion over six months, and then to an elevated 3.9% annual rate over three months.

The core PPI is a bit more copacetic, but it shows clear acceleration, rising from a 12-month pace of 1.3%, to a 1.8% pace over six months, and to 2.4% annualized over three months.

Consumer prices in Germany The sky is not falling. So far, there is no evidence of inflation in consumer goods: the consumer goods index does not even rise over 12 months, six months, or three months—though it is flat over three months. Investment goods, by contrast, show clear price acceleration, rising from 1.9% over 12 months, to 2.6% over six months, and to 4.1% over three months. Intermediate goods show the inflation wallop as prices rise by 1.5% over 12 months, to a 5.1% pace over six months, and at an 8.1% annual rate pace over three months. That annualized intermediate goods gain is something to watch. It is driven by oil, but other commodities and goods are caught up in supply chain woes as well.

For reference, the headline CPI shows acceleration, rising from a 12-month pace of 2.7% to a 5% annualized rate over three months. The ex-energy CPI, however, remains subdued, rising 2.3% over 12 month and at a more modest 2% annualized pace over three months.

Global conditions will call the tune The Strait of Hormuz, once shut, was opened. Then, once open, it was again shut. So, we are back at square one with the Trump deadline on Tuesday fast approaching. Soon something will have to give, and that something will affect oil, oil prices, and inflation. Conditions in the Strait and in the oil market globally are distorted by warfare and the threat of it.

Oil is an extremely important commodity and that is doubly so in Europe where nations have still not fully adjusted to the loss of the Russian pipelines.

But fertilizer and helium are two other commodities reported to be put in short supply because of the closing of the Strait. Iran is trying to gain a toehold here for leverage and survival—and to be able to claim victory; meanwhile, they have lost nearly all their military prowess, but they retain the means to enforce their policies on the domestic population—at least for now.

Trump has been declaring that they gave him everything he asked for, but then they close the strait and the U.S. kept its blockage of Iran’s ports in place. There is still a lot going on here. Despite the rhetoric, there is a lot that is unsettled and not agreed to, and a lot that could still go wrong or escalate. This puts both inflation and growth outlooks in jeopardy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia