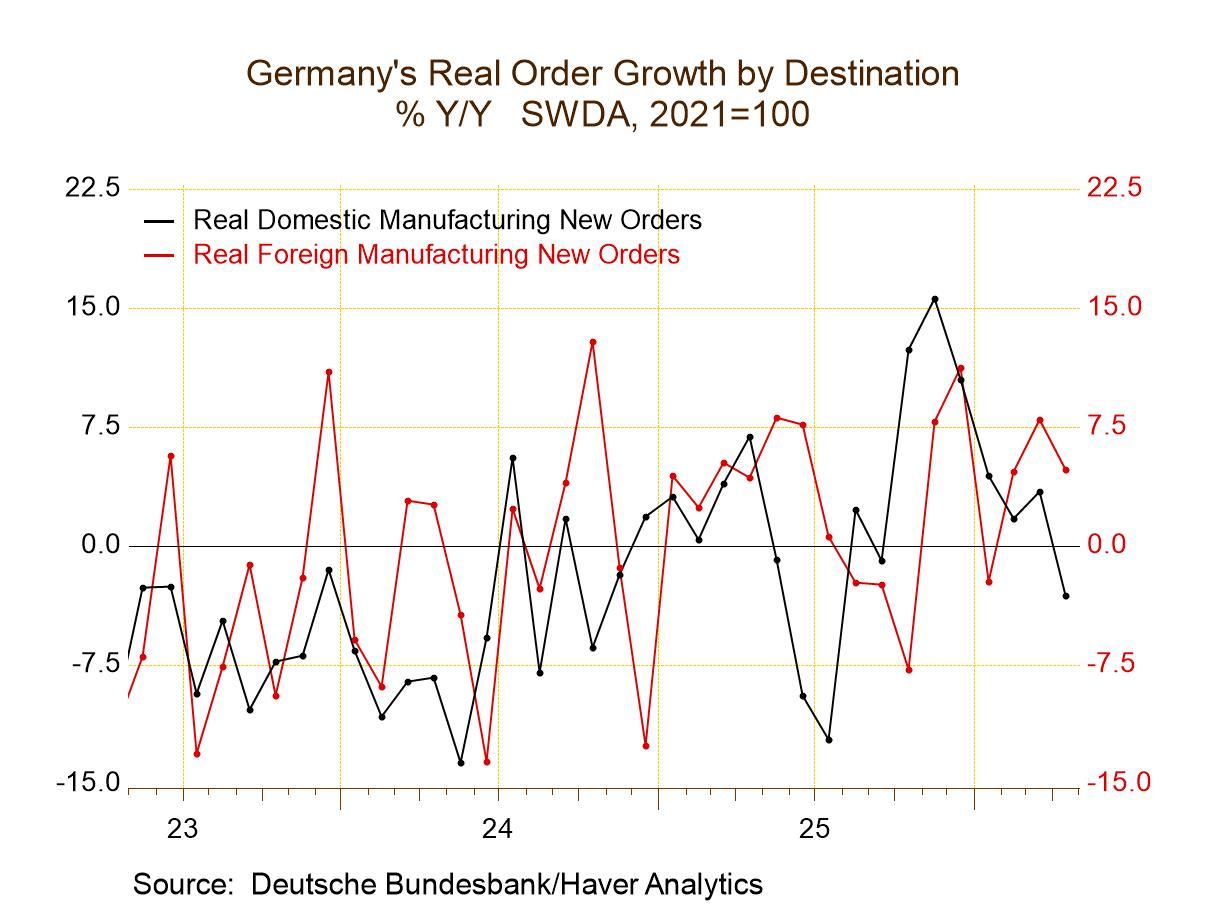

German Orders Drop, But Trend Offers Hope

German orders, now available for April, show both domestic and foreign orders are sketching a herky-jerky path higher. The volatility is such that we can't be sure the momentum will remain higher, but for the time being, the present orders are oscillating around an upward trend. There is a particularly striking downward movement in domestic orders, with three sizeable month-to-month drops in the last four months. The drop in foreign orders, at 4.2% month-to-month, is sharp, but that follows two months of very strong gains—although they follow one month of a substantial drop. German orders are simply sketching out a very dissonant path—very hard to discern a trend.

German orders show systemic sequential declines in domestic orders, an event that is offset by systematic sequential acceleration in foreign orders. The net result of total orders is an order slowdown over six months and four months that gives way to a sharp rise over three months.

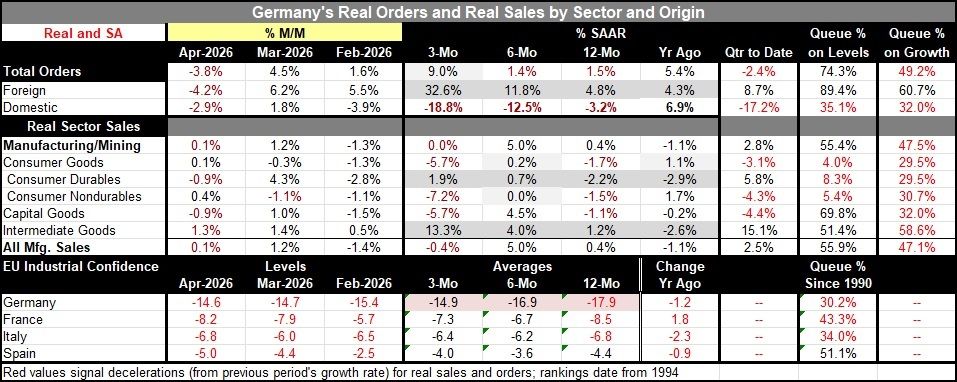

Sector sales, expressed also in real trend, show consumer durable goods sales and intermediate good sales both engaged in alternating behavior.

Early in Q2, German orders show declines overall an in domestic orders that are only partly blunted by a sizeable rise in foreign orders. Sector sales show a real gain in manufacturing, pushed ahead by consumer durables and intermediate goods, against weakness in nondurables and in capital goods. The broad ranking of annual growth rates for sales and orders show abject ranking weakness for orders and all sales, with the sole exception of orders by foreigners—that series has a ranking above its median at the 60.7 percentile mark.

To compare German industry with other key European sectors, we use the EU industrial confidence gauges. This shows Spain as the only country among Spain, Italy, Germany, and France, with an industrial sector ranking above the 50th percentile mark (above its median reading). All of the manufacturing readings have negative values in April; however, only Germany shows an advance in progression from 12 months to six months to three months.

The industrial order report for April is weak, but there are undercurrents of uptrends embedded in the report. The month’s results and trends may be better than the current month’s topical readings suggest.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global