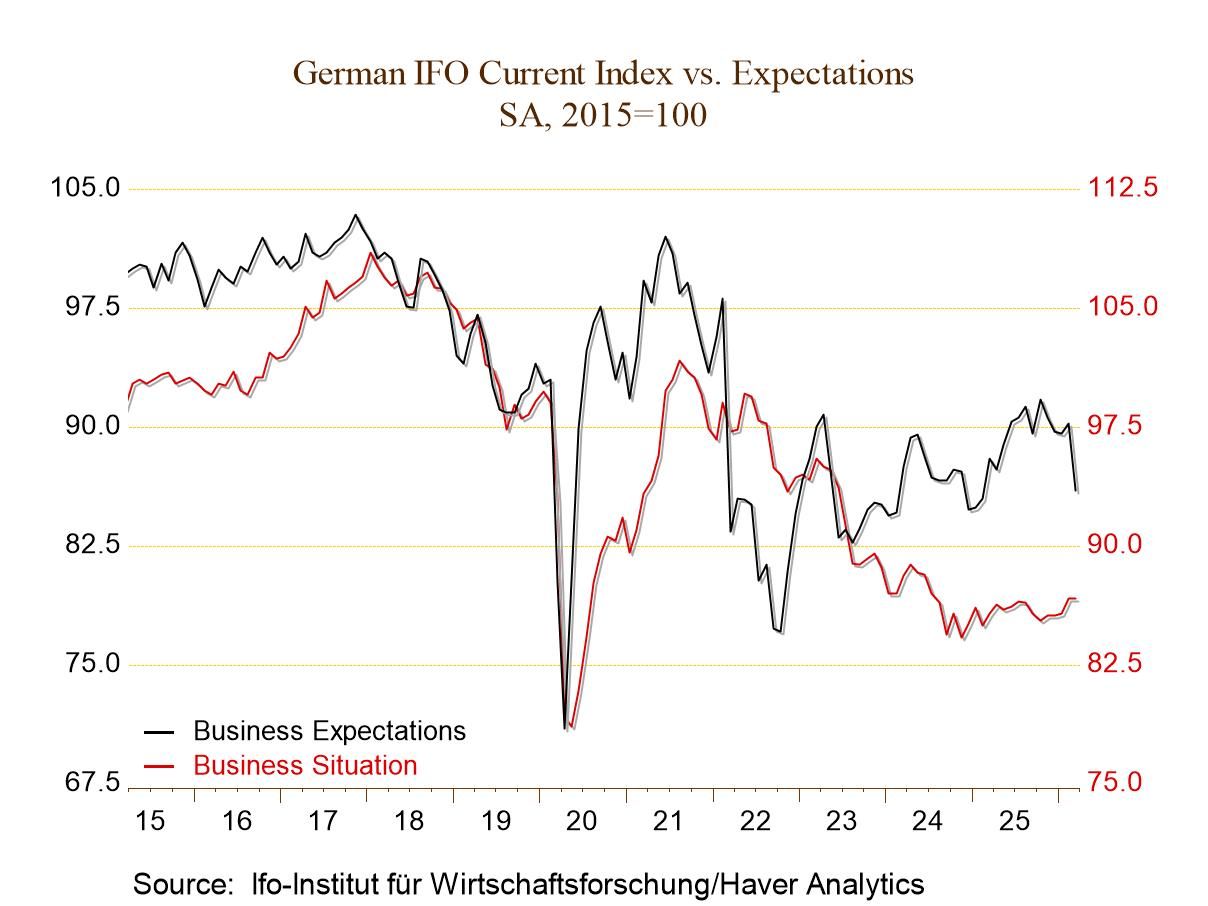

German IFO Sinks Even as the Current Reading Improves

The IFO readings for March 2026 show that the all-sector climate fell to -17.9 from -14.9 in February. The current conditions index improved by the smallest amount possible, rising to -2.4 after reaching -2.5 in February. Expectations, however, were clobbered, with the index in March falling to -19.7 after posting a -10.8 reading in February.

This expectations module for businesses in March registers a month-to-month drop of nearly 9 points; it ranks 246th out of 252 monthly changes, marking it as an occurrence that is this bad or worse, only 2.4% of the time (only 7 worse readings in the last 21 years). It's a stunning one-month backtrack in expectations for Germany.

Early reactions and developments We are currently in late March, so the reading reflects some reaction to the Iran war, and the reaction that we see certainly suggests that there is a relatively severe reaction by the business community to this war. Of course, the initial phase went extremely well from the standpoint of the United States and Israel, not from the standpoint of Iran. As the war has gone on, the U.S. and Israel have continued to register extremely successful military operations with very few of their own losses. However, it has also become clear that Iran intends to fight back on the ground and has tried to spread the conflict regionally using its missile capabilities—which appear to be more far-reaching than previously thought. We are left with the impression that Iran is prepared to engage in guerrilla warfare, which would be very difficult for conventional military operation to completely stamp out. The U.S. has resisted a call for boots on the ground although Donald Trump appears to be sending some paratroopers into the region. The U.S. has threatened to take control of Iran’s crown jewel of oil operations, Kharg Island. This threat has been made to counter Iran’s efforts to try to close the Strait of Hormuz, probably its only trump card. The U.S. has issued additional threats against Iran if it doesn't reopen the strait and allow oil traffic to pass again.

These conditions are, in many ways, a worst-case scenario for Europe and certainly a worst-case scenario for China and Japan that are so incredibly dependent on oil imports. Europe gets its oil imports substantially from the Middle East, meaning that those imports have to flow through the Strait of Hormuz. And then there's the embargoed Russian oil. There has been Iranian oil that has been on the market, having slipped through embargoes using clandestine tankers. U.S. actions in Venezuela have shut down the Venezuelan shipments that were substantially to China. All of these moves create a great impact, an impasse from oil scarcity, which has led to rising oil prices even though the U.S. has uncorked its strategic petroleum reserve and has promised to make more supplies available from that source. Unlike during 1973-75, the U.S. sits in the catbird seat.

The oil weapon has been broken out, and at the same time, turnabout has become fair play as the U.S. now has the upper hand on oil as Iran crimped the supply through the Strait of Hormuz. Strangely, much of Europe had said it would opt out of the U.S. plan to reopen the strait, but after a short period of time, 22 countries have now signed on to help unplug this strait.

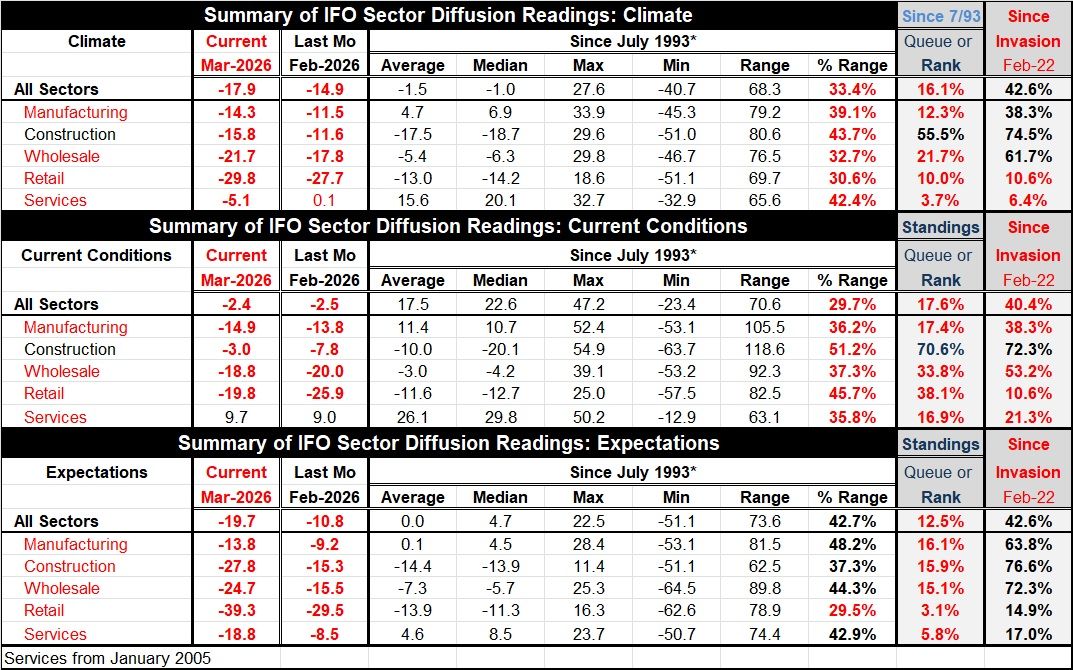

Beyond oil (...sort of) The IFO survey shows expectations have dropped exceedingly hard in response to these events, with the expectation standings by industry ranging from a high of 16.1% in manufacturing to a low of 3.1% in retailing and 5.8% for services in general. The net diffusion readings for March range from a negative reading of -39.3 in retailing to a negative reading of -13.8 in manufacturing.

The current conditions rankings range from a high percentile standing in its 70.6 percentile for construction to a low standing in its 16.9 percentile for services.

And this is a report that has not given survey respondents a lot of time to see and react to events.

The future is...unknown-gasp! As always (in fact!), no one knows where this goes or how long it is going to take to stabilize oil prices. Iranian leaders are in a very tough position, having run roughshod over their own people. If they lose their grip domestically, the U.S. and Israel will not need boots on the ground to do what Iran’s own people will do if they gain that capability through freedom. The question here is whether there is enough left of the secret police and its vast, nearly 50-year-old organization, to continue to suppress the people. The calculus for Iran fits in the category of a slippery slope—or perhaps what catastrophe theory describes—in which everything will remain under control unless the dam of control breaks, in which case everything will change.

Precedents? Not really... For those looking for historic precedents, let’s remember that in the U.S. oil prices began around $3/barrel in 1973 and rose to about $12/barrel—a rise of some 300%. Today’s ‘painful’ increase from about $80 to over $100 is child’s play by comparison. In the 1970s, effectively it was worse, and oil price increases hit hard. There were homes being built with electric heat where people experienced heating bills larger than their mortgage payments in the U.S. Also, because of the Yom Kippur War and the U.S. siding with Israel, there was an Arab oil embargo in the U.S. and Europe that resulted in fuel rationing. These circumstances spawned the phenomenon known as stagflation. The oil impact was so much worse then, compared to now. I would be quick to say this unfolding episode has little in common with the 1973-75 recession experience with oil and oil prices. The U.S. is especially well-insulated from any potential worsening.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global