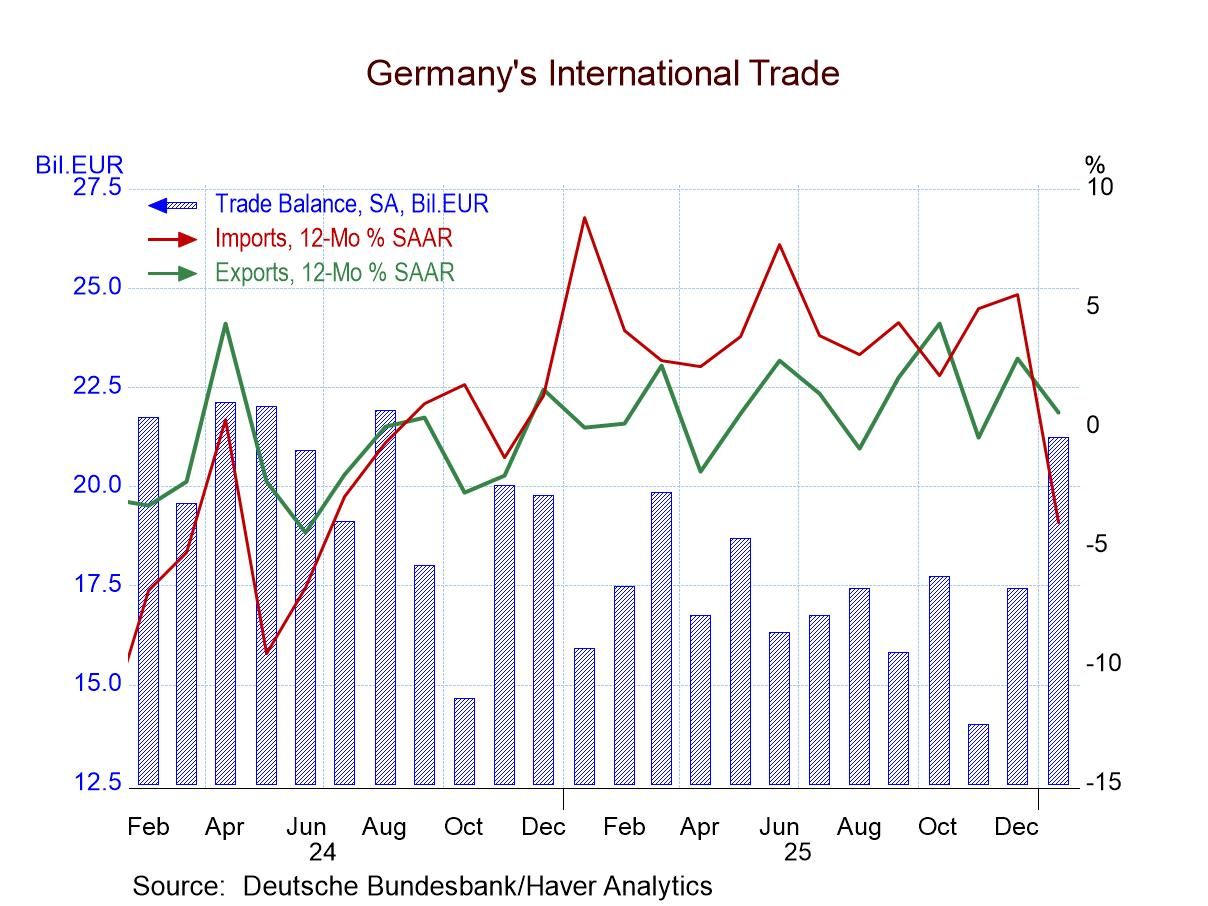

German Exports and Imports Slide in January; Sharp Import Drop Boosts Surplus

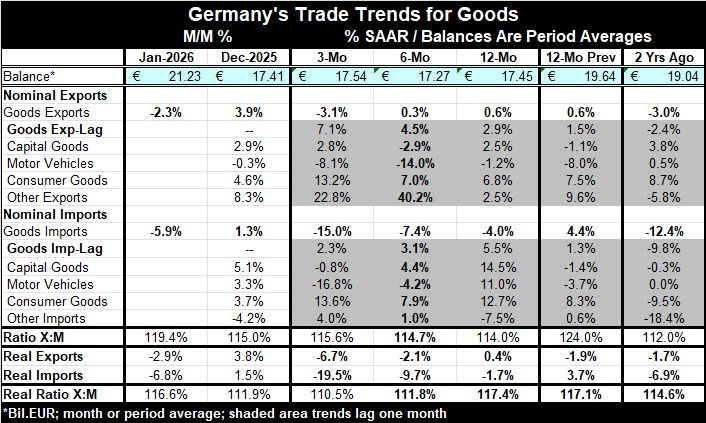

German trade flows weakened in January, with imports dropping 5.9% month to month and exports falling 2.3%. With both flows falling sharply and imports dropping at more than twice the rate of exports, the trade surplus in the month ballooned to €21.2 billion from €17.4 billion in December.

The progression of nominal growth rates for exports shows the slowing from 0.6% over 12 months to 0.3% over six months to -3.1% at an annual rate over three months. The import decline is weaker and is gathering even more downward momentum, with imports falling 4% over 12 months, dropping at a 7.4% annual rate over six months, and reaching a 15% annualized decline over three months.

Measured in real terms, exports fell by 2.9% in January as imports fell by 6.8%. The sequential growth rates for German exports and imports both show progressive deterioration, with imports weakening faster than exports. This trend is worrisome because it says that the nominal weakness is not just because of what prices are doing. Weak imports usually indicate weak domestic demand; for Germany, that could be a really bad signal. In addition, because Germany exports so much to other EMU nations, German export weakness raises questions about demand strength among fellow EMU members - and about global demand in general.

Lagged trends Lagged results give us a look into export and import trends with a one-month lag. As of December, both exports and imports still rose month-to-month. Sequential export growth was steadily accelerating, while sequential import growth rates were already decaying. German consumer goods exports were accelerating sequentially, and the ‘other exports’ category is not on its own acceleration path, but the category remains strong.

For imports, the overall nominal flows were decelerating from 12-months to 6-months to 3-months. Capital goods and motor vehicle imports both showed sequential weakening. Consumer goods imports were oscillating but still generally strong. Other imports were on a recent accelerating path, switching from negative 12-months growth to a 1% gain over six months and a 4% pace of increase over three months.

Summing up On balance, German trade trends show a lot of weakness. Much of it seems to have welled up in January ahead of the new Middle East conflict. Right now, German economic data and diagnostic trade data are not sending out good signals about the German economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global