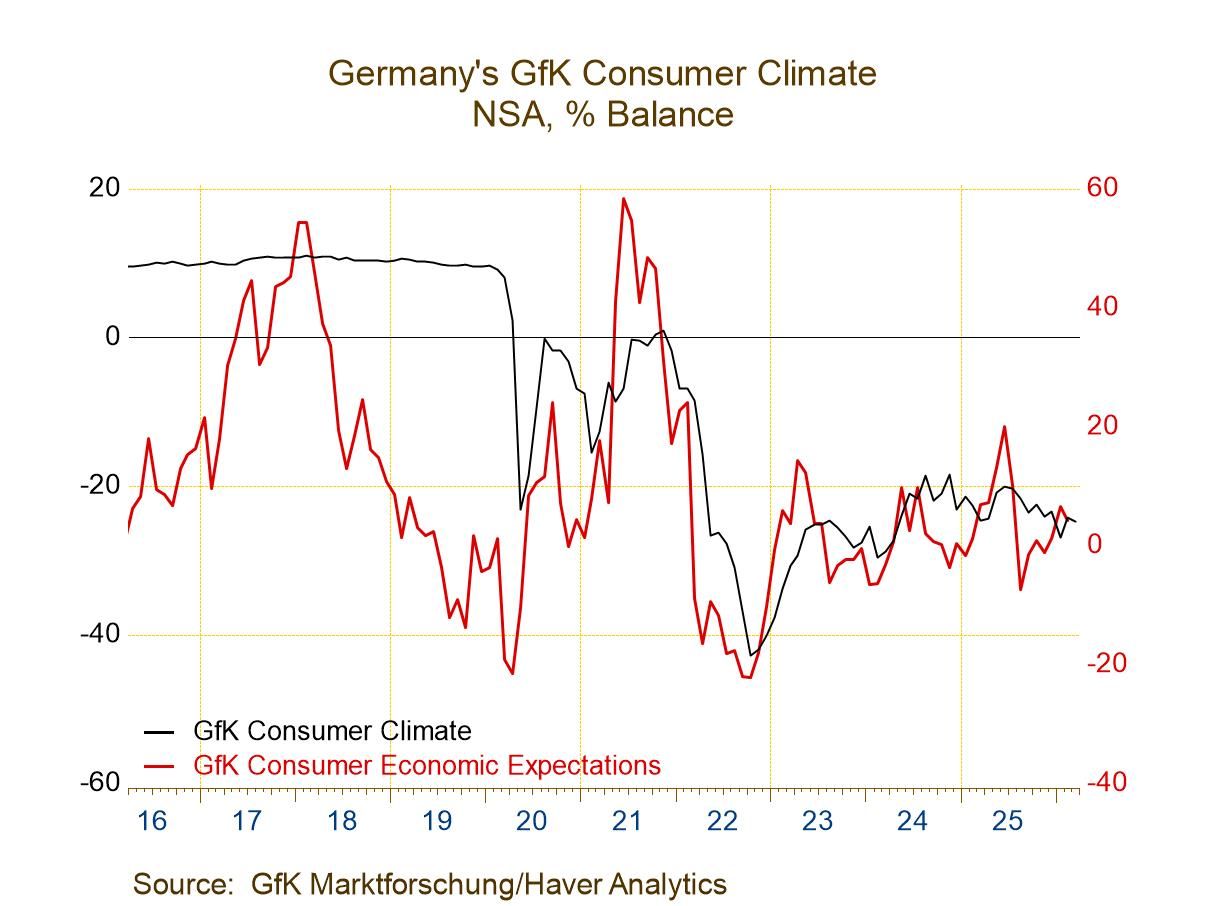

German Confidence: GfK Consumer Climate Erodes

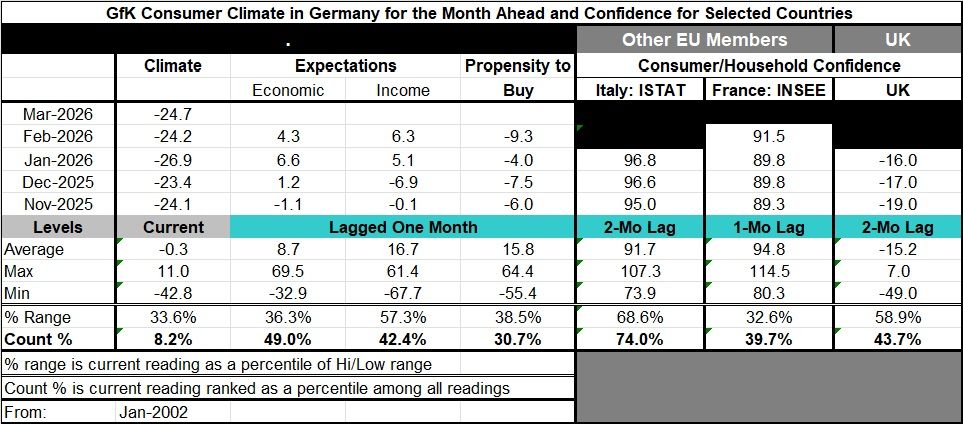

Climate eased in March after improving in February. There still is a net improvement compared to January, but we must turn the calendar back to April 2024 to find a climate reading lower than the current level in March. In sum, there is no sense of ongoing improvement for climate in this report. The economic expectations and income expectations readings, which lag by one month, do show some improvement on a longer timeline. But the propensity-to-buy index is still quite weak.

Climate at -24.7 in March has an 8.2 percentile standing on data back to 2002. The economic expectations, reading, fell back to 4.3 in February from 6.6 in January to set a 49-percentile standing. Income expectations rose to 6.3 in February from 5.1 in January. Income expectations have a 42.4 percentile standing. The propensity to buy weakened sharply to -9.3 in February from -4 in January. Its percentile standing is at a 30.7 percentile level, a bottom one-third standing.

The table also presents consumer confidence readings for three other European economies. Among them, Italy has the strongest ranking at a 74-percentiel standing. The Italian reading is up-to-date through January and has been showing improvement. The United Kingdom and France have similar standings. The U.K. standing is at its 43.7 percentile mark, below its median on this timeline. The U.K. reading is up-to-date through January and has been showing a tendency to improve. France has a rank standing at a 39.7 percentile; it is up-to-date through February. The index has been very slowly improving.

The bottom line is that confidence has mostly stabilized in Germany and across Europe. But most of that is done at relatively weak levels of confidence. Italy is the exception, with an above median nearly top one-quarter standing—but it has no upward momentum. Stabilization sure beats deterioration, but the readings are weak and have been weak, and it is really time for Europe to be mounting a drive to better conditions. The sense of upward momentum across these confidence readings is extremely weak—mostly lacking. The never-ending war between Russia and Ukraine is one reason for this performance. Another has been the ongoing battle to reduce inflation, but that battle now seems to be nearly won. Still, it is not clear how much space exists to cut rates further. The Bank of England has to make more progress on inflation, and when it does, rates there can come down. But in the EMU, there may not be much more left in the way of monetary stimulus. Meanwhile, fiscal policy has been employed nearly to the max in France and in the United Kingdom. A good chunk of fiscal policy is being used to rebuild armaments as Euro-NATO has realized it must do more to protect itself. There continues to be a lot in play as 2026 unfolds.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia