Asia| Apr 13 2026

Asia| Apr 13 2026Economic Letter from Asia: A Shifting Consensus

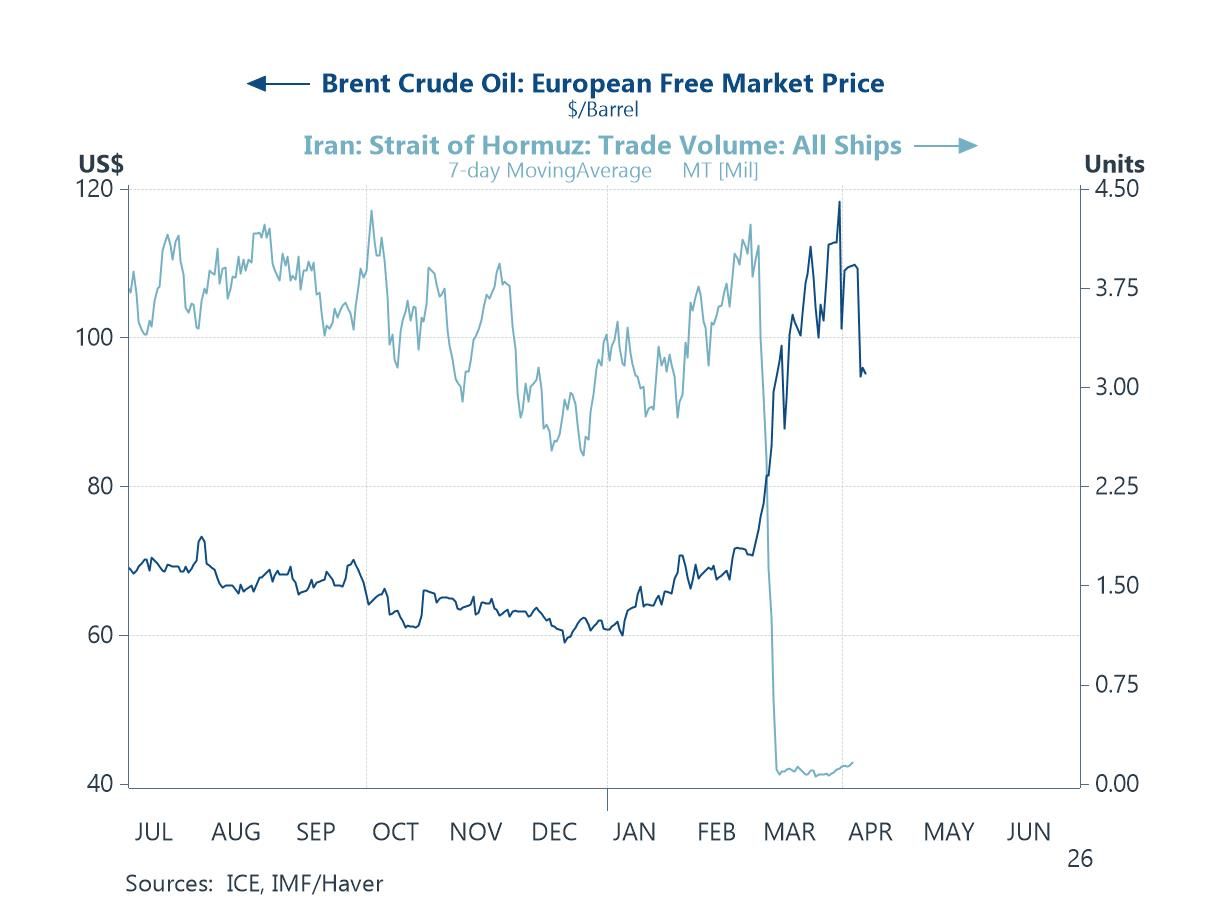

In this week’s Letter, we continue to track developments in the Middle East and their implications for Asia. While the recent US–Iran ceasefire initially provided some relief to markets, subsequent complications have kept uncertainty elevated, with no conclusive resumption of trade flows yet through the Strait of Hormuz (chart 1)—flows that are critical to restoring the global energy system to more normal conditions.

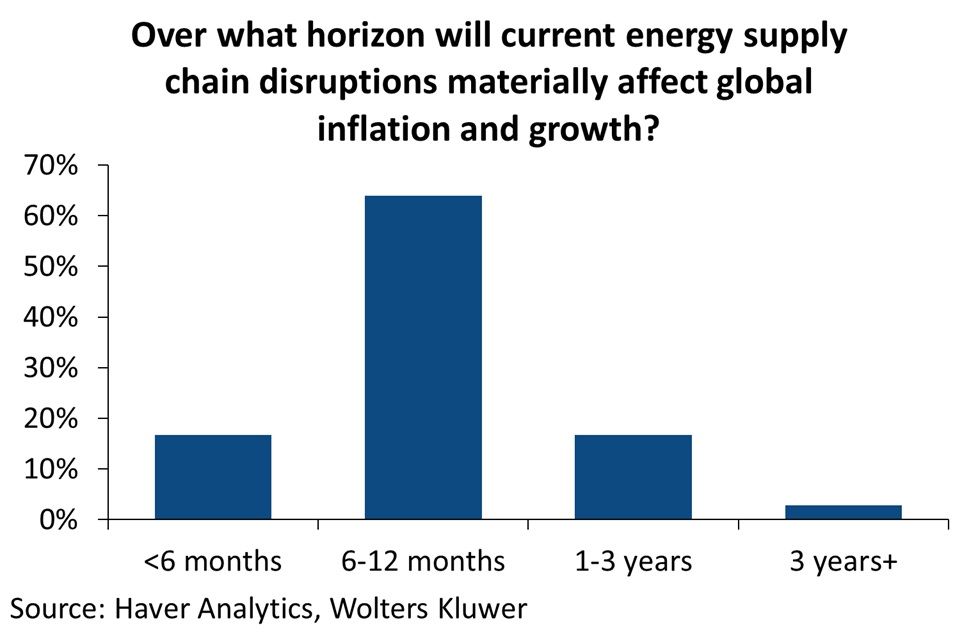

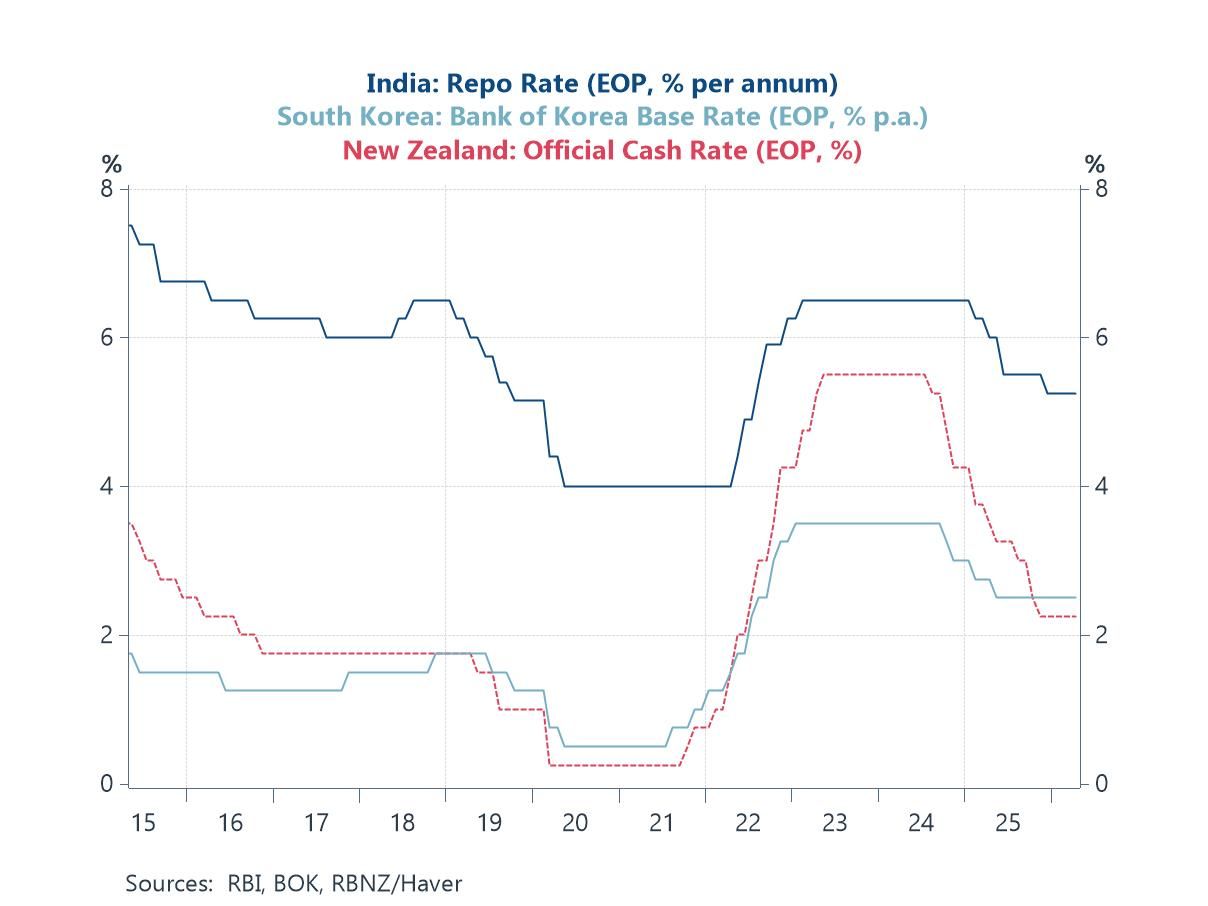

Overall, our Blue Chip Economic Indicators panellists have broadly downgraded growth expectations for Asia this year, with the exceptions of China and Taiwan, while inflation forecasts have been revised higher across the board (chart 2). That said, the growth and inflation impact from the conflict are largely viewed as transitory, with most panellists expecting them to last between six and twelve months (chart 3). Nonetheless, central banks in the region appear increasingly reluctant to ease policy further. This is evident in the latest round of decisions, where India, South Korea, and New Zealand all held policy rates steady (chart 4), citing heightened uncertainty stemming from the ongoing conflict.

While inflationary pressures are beginning to build more broadly across the region, China had already been experiencing a pickup in recent months (chart 5). This has been supported by easing producer price deflation and improving industrial profits, alongside policy efforts to curb excessive price competition among producers. Attention now turns to China’s upcoming Q1 GDP release and the full slate of monthly data due later this week (chart 6).

Middle east conflict developments Crude oil prices fell sharply earlier last week following news of a temporary US–Iran ceasefire. That said, the geopolitical backdrop remains highly fragile, as reflected in continued rhetoric from both sides, alongside the US announcement of a naval blockade over the strait after talks failed to yield an agreement. Compounding this, Iran has indicated that it cannot fully reopen the strait, citing uncertainty over the location of sea mines it had previously laid—further complicating any swift normalization of oil flows. Even prior to these latest developments, IMF-tracked shipping volumes had only begun to show tentative signs of recovery and remain well below pre-escalation levels. As such, while the ceasefire provides a welcome reprieve, meaningful economic relief will hinge on a sustained restoration of oil flows—crucially without additional frictions or costs that could impair global trade. Until then, crude prices are likely to remain elevated, albeit possibly off recent highs, weighing on growth while sustaining inflationary pressures. In Asia, where many economies are heavily reliant on oil imports, the region is likely to bear a disproportionate share of these effects.

Chart 1: Brent crude oil price and Strait of Hormuz shipping volume

The latest Blue Chip Economic Indicators survey In light of recent developments, our latest Blue Chip Economic Indicators (BCEI) survey provides a timely update. It is a monthly poll of forecasters covering key economic indicators across a wide range of economies. As shown in chart 2, panellists have generally trimmed their 2026 growth forecasts across most Asian economies. Taiwan is a notable exception, with growth expectations revised higher, likely continuing to be supported by the ongoing AI-driven expansion. Meanwhile, forecasts for China’s 2026 growth were left unchanged. On the inflation front, expectations for 2026 have been revised higher across all Asian economies, consistent with the pass-through from the recent surge in oil prices. The largest upward revision was seen in Australia (+0.7 ppts), while increases were more modest in economies such as Japan and China (+0.3 ppts each).

Chart 2: Blue Chip Economic Indicators 1-month change in panellist forecasts

Digging deeper into this month’s BCEI survey, the special questions provide additional insight into panellists’ views. In particular, one question asked about the time horizon over which current energy supply chain disruptions are expected to materially affect global inflation and growth. Panellists largely view the impact as short term (chart 3), with most clustering around a six- to twelve-month window. Smaller shares see effects lasting either less than six months or extending between one and three years, while only a very small minority expect disruptions to persist beyond three years. Overall, while the recent oil price surge represents a clear shock to the global economy, it is widely seen as transitory—temporarily lifting inflation and weighing modestly on growth, but unlikely to drive a fundamental shift in the broader macroeconomic outlook.

Chart 3: Blue Chip Economic Indicators special survey question on energy price impacts

The week’s central bank decisions Turning to last week’s key monetary policy decisions in the region, the central banks of India (RBI), South Korea (BoK), and New Zealand (RBNZ) all kept policy rates unchanged, with several common threads across their communications. Notably, each highlighted the considerable uncertainty stemming from the Middle East conflict, which has already begun to feed into global inflation via higher oil prices. This aligns with broader investor sentiment: the bar for further policy easing has risen given renewed inflationary pressures, while the threshold for a shift toward tightening remains high, as most economies are still far from overheating. On central bank–specific nuances, the RBI emphasized the delicate trade-off between anchoring inflation expectations and minimizing growth sacrifices. The BoK noted that its policy rate is around the neutral level, while flagging potential additional pressure on the won from elevated oil prices. Meanwhile, the RBNZ signalled that near-term inflation is likely to rise even as the economic recovery softens, citing significant supply chain disruptions linked to the Middle East conflict.

Chart 4: India, South Korea, and New Zealand policy rates

China and the week ahead Lastly, we turn to China and the week ahead. As shown in chart 5, even prior to the Middle East conflict, China had already begun to see a pickup in inflation—an early indication that it may be moving out of its prolonged period of chronically low, or even negative, price pressures. This recent firming in CPI inflation has been accompanied by more sustained growth in industrial profits and a steady improvement in producer price pressures, with PPI inflation recently turning positive after a multi-year stretch of deflation. Together, these trends point to gradually strengthening price dynamics. The shift in inflation also reflects underlying policy efforts to curb excessive price competition among producers, which had weighed on prices for an extended period. Looking ahead, the recent oil price shock could provide an additional boost to inflation, as higher energy costs begin to feed through into future readings.

Chart 5: China inflation and industrial profits

Looking ahead to the coming week, Asia faces a packed data calendar, with the spotlight firmly on China as its Q1 GDP release and the usual slate of monthly indicators are due (chart 6). A key focus will be how March data shapes overall Q1 growth, particularly given that activity in the first two months of the year largely surprised to the upside. Investors will also be watching for any early signs of spillovers from the Middle East conflict in the March prints. Retail sales will be closely monitored as a gauge of the effectiveness of policy support for consumption, while developments in house prices will remain in focus as the property downturn continues to unfold gradually.

Chart 6: China’s GDP growth and monthly economic indicators

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief