Global| May 29 2026

Global| May 29 2026EMU Early Inflation Readings Rise in Large Countries

In the post-COVID cycle, inflation in Italy hit its low point early in 2023 and then again late in 2024. However, for the other large monetary union economies, France, for example, inflation hit its low point early in 2026 at a pace of about 1.1%. Germany, the traditional low-inflation country in the monetary union, has had more difficult times with inflation post-COVID. For this reason, the low point for German inflation came early in 2026 (and in mid-2025 at 1.9%). For France and Italy, headline inflation began escalating very early in 2026. For Germany, the escalation was a little later, and the spiky part of inflation was blunted on the early side; inflation has actually tipped slightly lower now, in May. However, despite these differences in timing, the overpowering sense is that inflation in the large countries has turned higher early in the year, and the European Central Bank will have some decisions to make.

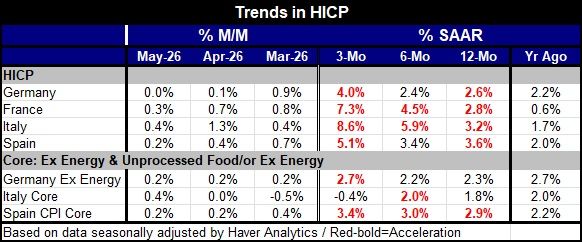

Month-to-month price changes In May, inflation decelerated in Germany, with the month-to-month observation going unchanged. Headline prices in Spain rose by 0.2%, in France by 0.3%, and in Italy by 0.4%. German prices excluding energy have been making steady gains for the last several months, rising by 0.2% in May; Italian core prices rose by 0.4% after being flat in April and declining sharply in March; in Spain, the core CPI rose by 0.2% for the second month in a row.

The monthly statistics on inflation from the headlines and core rates for these countries are not off-the-charts or particularly troublesome. However, when put in context in terms of 3-month, 6-month, and 12-month inflation rates, the headlines and the cores trace more disturbing patterns.

Sequential trends in the HICPs Headline inflation for these countries shows over three months that inflation has a rate excessive relative to the ECB's target for the European Monetary Union as a whole. There are no country-by-country targets from the ECB, only an objective for the union-wide result. German inflation over three months is the weakest, as it logs a 4% annual rate. Italian inflation is the strongest, rising at an 8.6% annual rate. Over six months, inflation is excessive in all four of these countries. The weakest gain is in Germany at 2.4% at an annual rate; the strongest is in Italy at a 5.9% annual rate. Over 12 months, inflation is also excessive across the board relative to the ECB's overall monetary union target of 2%. The weakest gain in 12-month inflation is Germany at 2.6%, while the strongest is Spain at 3.6%. Additionally, inflation is accelerating from 12-months to six-months to three-months in both France and Italy. Although inflation is not accelerating in that three-period sequence for Germany and Spain, it is not far from doing so. All of these are going to be uncomfortable metrics for the European Central Bank to navigate. These are the headline rates for the large EMU countries, and they are clearly being pushed up by energy prices on the constriction of traffic through the Strait of Hormuz.

Core and ex-energy inflation trends Three of the four largest EMU economies give us either core inflation or inflation excluding energy metrics. On that basis, two of three economies, Germany and Spain, show excessive inflation over three months annualized, at 2.7% for Germany and 3.4%, for Spain. We compare them to the target set by the ECB for the European Union overall. Italy is the exception, with core inflation falling 0.4% at an annual rate over three months. Over six months, Germany, Italy, and Spain all have core inflation rates at or above 2%. Italy's rate comes in at 2%, Germany's ex-energy rate is at 2.2% annualized, while Spain’s CPI core checks in at 3% inflation. Over 12 months, inflation in Germany excluding energy is 2.3%, in Spain the CPI core runs 2.9%, while in Italy, inflation is still restrained for the core measure at a 1.8% annual rate.

Headline inflation and rising energy prices clearly are generating pressures such that even the core conditions aren't looking good. Core inflation rates above 3%, as we see in Spain across nearly all three timelines, are disturbing to the monetary authority. German inflation is moderate at 2.2% over six months and 2.3% over 12 months, but then it rises to a more disturbing 2.7% over three months. So far, Italian inflation is not an issue, at 1.8% over 12 months, 2% over six months, and even declining at a 0.4% annual rate over three months.

Summing up The ECB, of course, makes policy for the whole of the area, so these individual country results are inputs that the ECB will look at, but it is much more concerned with what happens to inflation for the euro area as a whole. We can see from these large countries that there is a considerable amount of inflation percolating and that the energy price increases have not been confined to impacting the headline. Also, since the ECB has been overshooting its inflation target, it has to be careful about cutting any slack for dealing with inflation when it becomes excessive. Inflation has started to accelerate in France and in Italy, at least at the headline level; the core shows accelerating inflation only for Spain. These are conditions the ECB is going to have to be sensitive to.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief