Global| May 28 2026

Global| May 28 2026Charts of the Week: The AI Boom Meets Inflation Angst

by:Andrew Cates

|in:Economy in Brief

Summary

The global macro backdrop remains dominated by instability in the Middle East and the lingering inflation concerns associated with elevated energy prices. Yet recent days have at least offered some tentative relief. Oil prices have softened amid heightened hopes that negotiations between the US and Iran could eventually ease tensions and help stabilise energy markets, even if the broader geopolitical situation remains fragile and key shipping routes continue to face disruption. Against this backdrop, the latest survey data continue to highlight an uneven global economy, with Europe looking particularly vulnerable given its greater sensitivity to higher energy costs and its weaker links to the global AI investment boom (chart 1). At the same time, rising gasoline prices continue to weigh heavily on US household confidence (the Michigan measure), raising concerns about the resilience of consumer demand (chart 2). An important question confronting markets in the meantime is whether inflation fears are now becoming overstated. Unlike during the post-pandemic inflation shock, central bank balance sheets are now shrinking rather than expanding aggressively, while money supply growth remains relatively weak across many major economies (charts 3 and 4). Meanwhile, the extraordinary boom in AI-related infrastructure spending — spanning data centres, utilities, water systems and semiconductors — continues to provide a major offset to broader macroeconomic weakness and remains a key pillar supporting global equity markets despite elevated geopolitical and inflation concerns (charts 5 and 6).

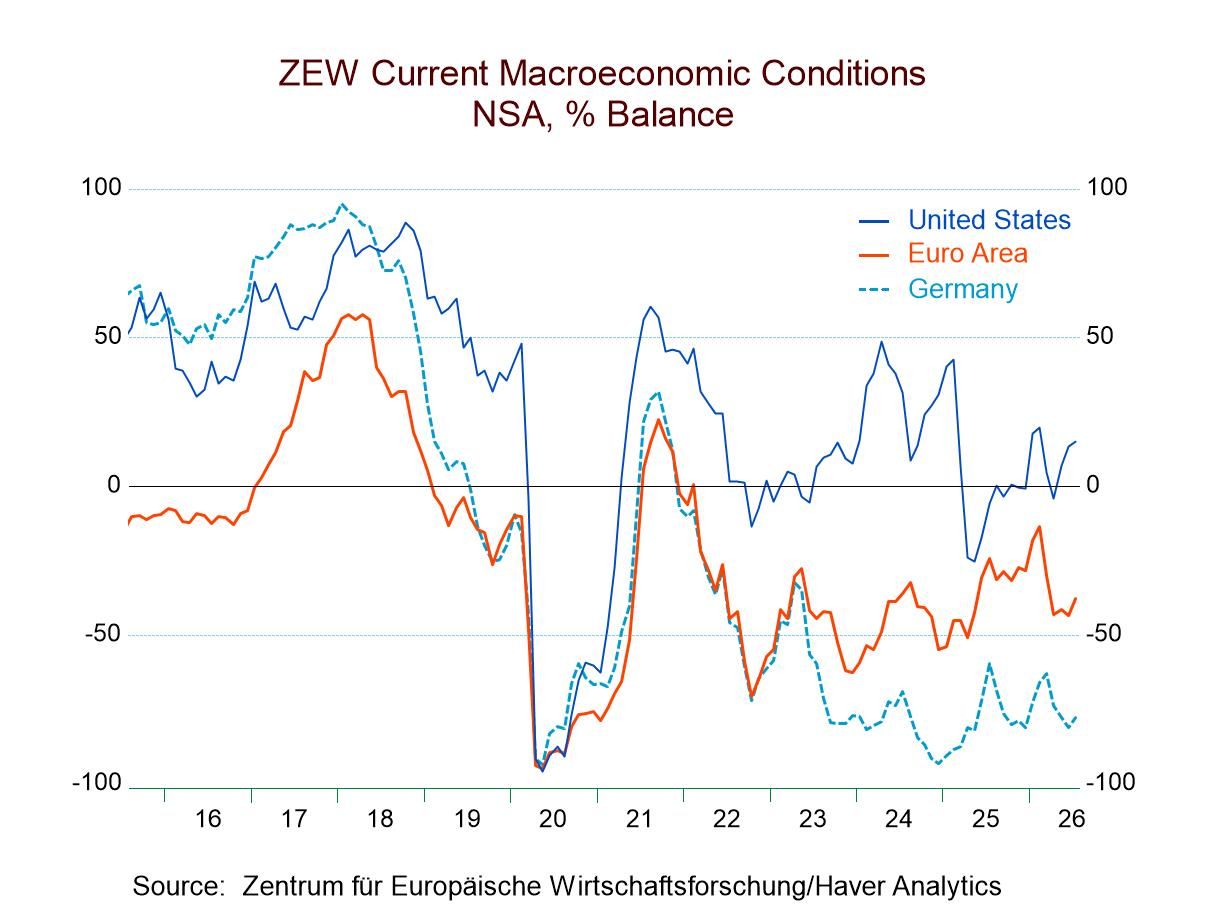

Europe’s vulnerability to high energy prices The latest flash PMI data continue to highlight a highly uneven global economy. India remains exceptionally strong, while the US and Japan continue to outperform most other advanced economies. By contrast, much of Europe remains considerably weaker, with France particularly soft and both Germany and the broader euro area struggling. In many respects, this divergence increasingly reflects Europe’s heightened sensitivity to elevated energy prices and, probably, its weaker exposure to the global AI investment boom currently supporting activity elsewhere. Europe remains far more vulnerable to higher imported energy costs, while the US and parts of Asia continue benefiting from stronger technology investment cycles, semiconductor demand and AI-related infrastructure spending.

Chart 1: Flash Composite PMI Surveys: Levels Versus Changes

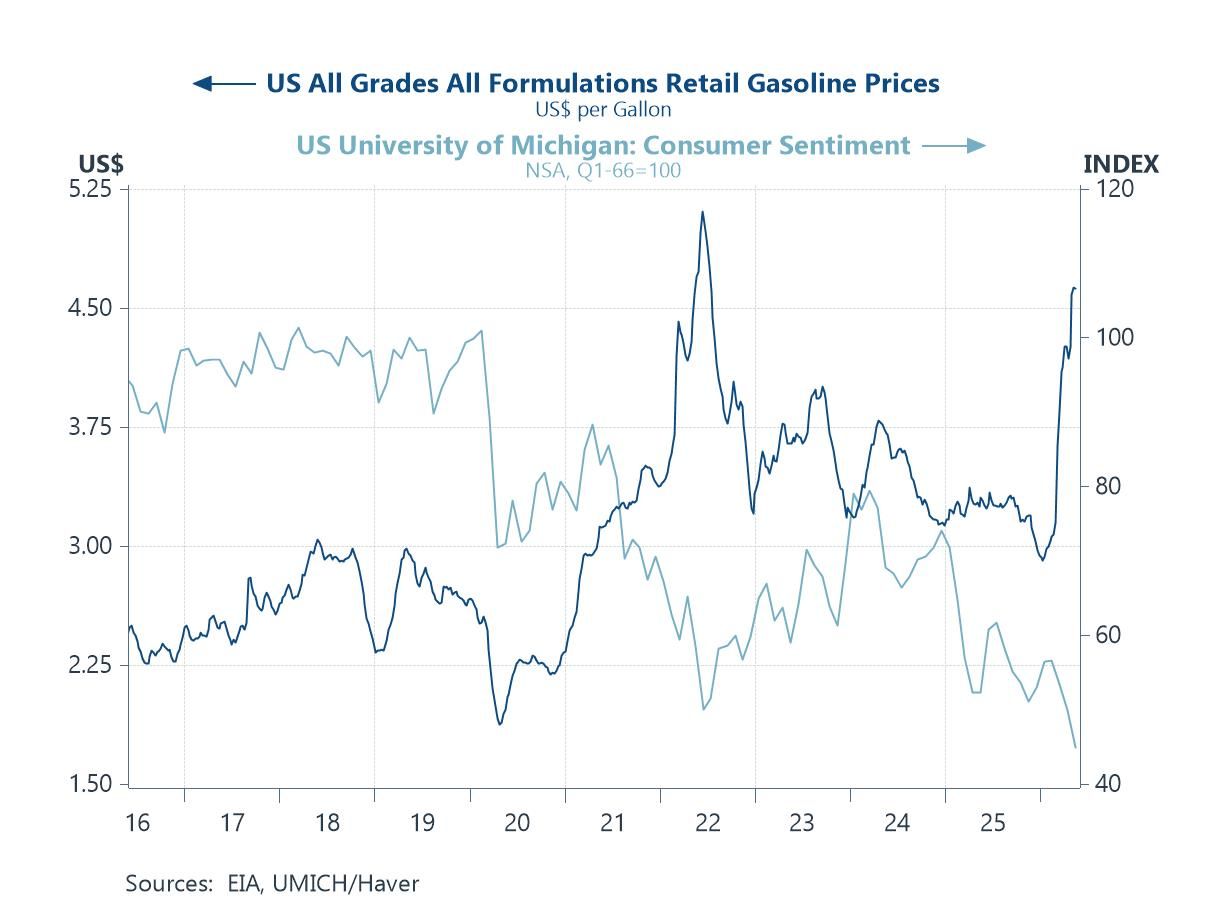

Higher energy prices continue to squeeze US consumers That said, rising gasoline prices in the US are clearly weighing on household sentiment. Consumer confidence, as measured by the University of Michigan survey, has fallen sharply even as labour markets remain relatively resilient, underscoring how sensitive households might be to renewed energy-related inflation fears. Yet this also reinforces an important counterpoint to the current inflation narrative. Unlike during the immediate post-pandemic period — when households were benefiting from extraordinary fiscal transfers, ultra-loose monetary policy and strong nominal income growth — consumers today appear more cautious and demand conditions far less exuberant.

Chart 2: US All Grades Retail Gasoline Prices & (Michigan) Consumer Sentiment

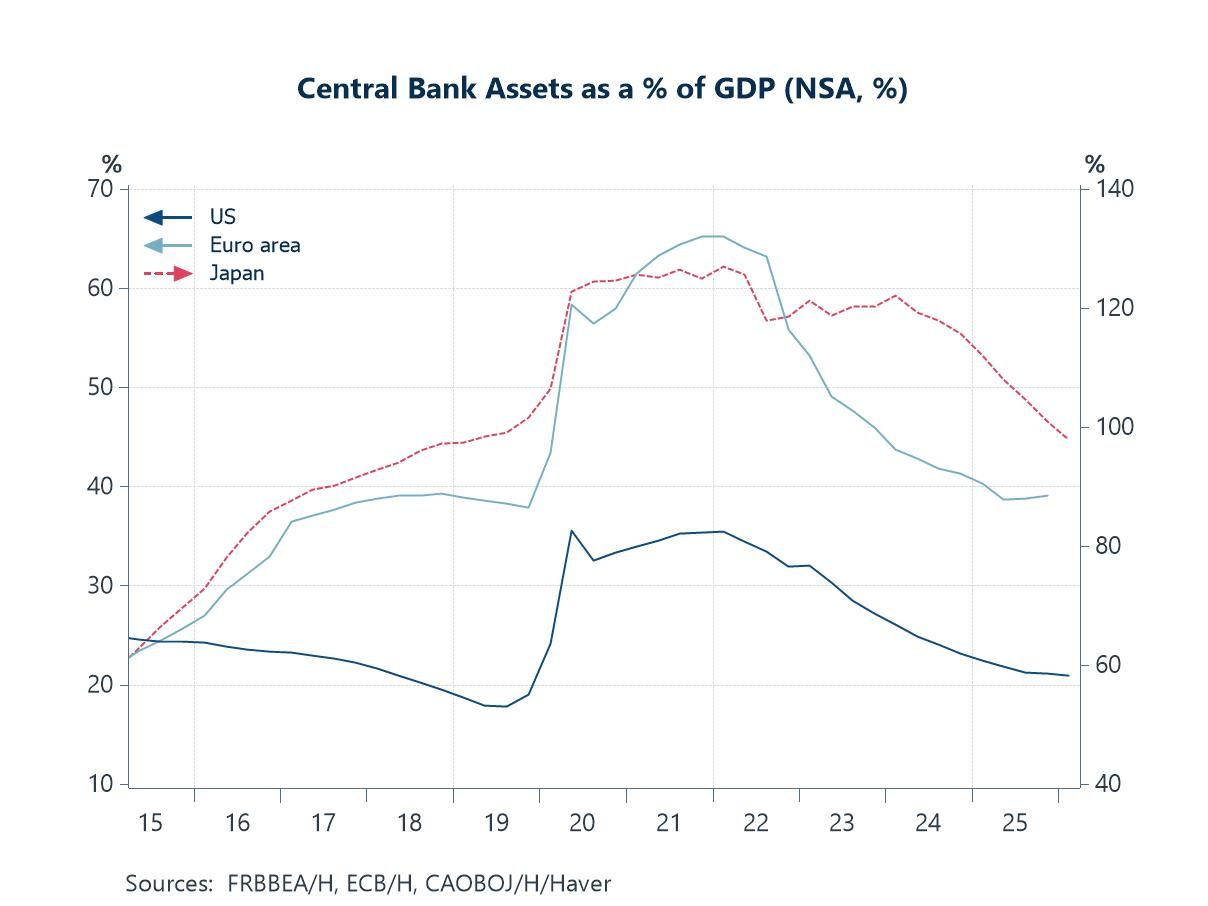

Not yet another pandemic-era liquidity shock Indeed, and as noted above, one of the most important differences between today’s inflation fears and the post-pandemic inflation surge concerns the underlying monetary backdrop. During the Covid pandemic, central banks massively expanded their balance sheets while governments simultaneously delivered extraordinary fiscal stimulus. That combination arguably helped fuel excess liquidity, surging demand and ultimately broad-based inflationary pressures. Today, however, the picture looks fundamentally different. Central bank balance sheets across the US, euro area and Japan are no longer expanding at anything like the pace seen during the pandemic period, with reduced asset purchases contributing to a much less supportive global liquidity backdrop.The global economy is therefore entering this latest energy shock against a backdrop of greater monetary restraint, or, at the least, far less extreme monetary accommodation.

Chart 3: Central Bank Assets as a % of GDP

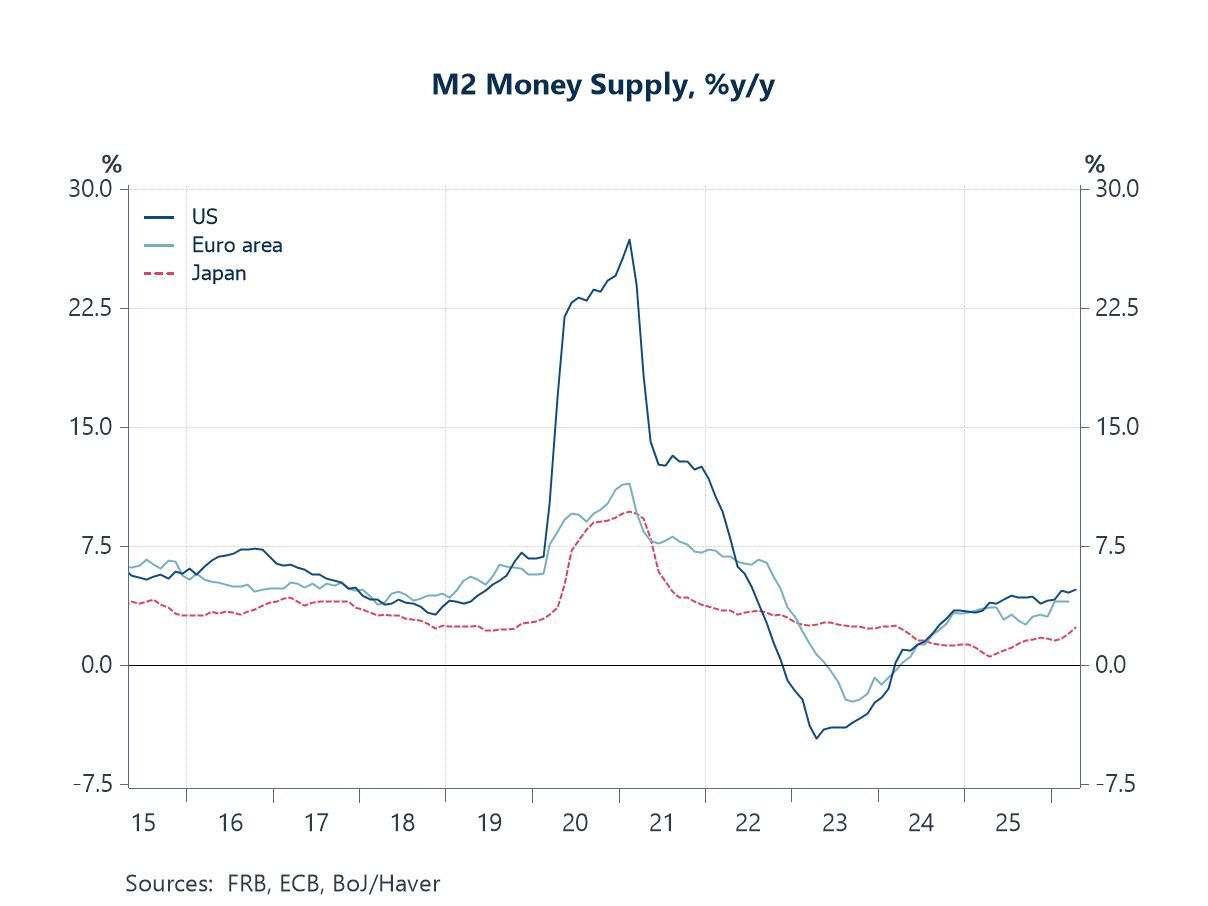

Broad money supply growth is not (yet) amplifying inflation concerns The contrast becomes even more striking when looking at broad money growth. Broad money growth across the major economies has slowed dramatically from the extraordinary rates seen during the pandemic period. In both the US and euro area, monetary growth remains subdued, reflecting tighter financial conditions and a much less supportive liquidity backdrop. This matters because periods of sustained inflation persistence have historically been associated not simply with commodity price spikes, but with strong underlying money and credit growth supporting broader demand conditions. Today’s monetary backdrop looks – for the time being - far less consistent with the kind of prolonged inflation spiral feared by many investors.

Chart 4: M2 Money Supply Growth

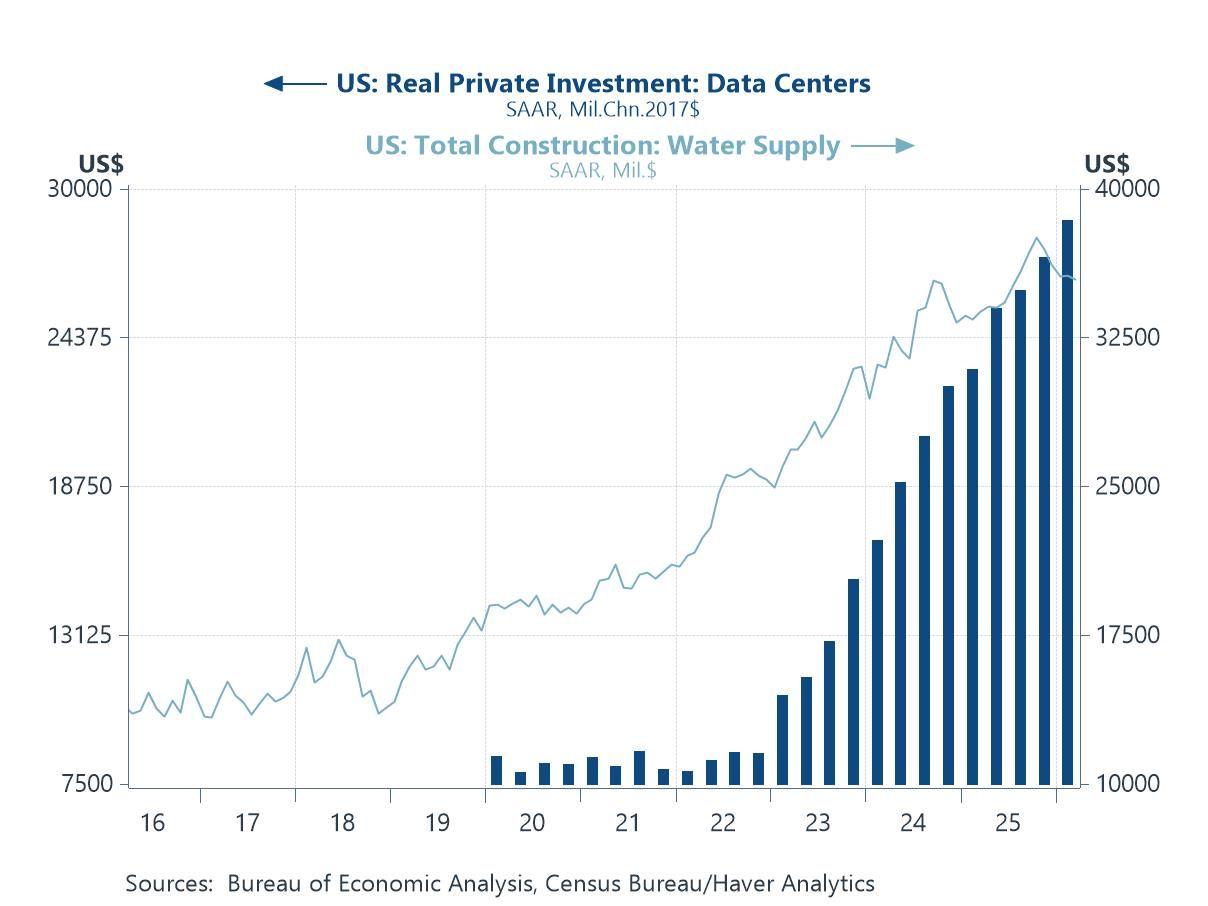

AI investment is becoming a full-scale infrastructure cycle At the same time, however, the global growth outlook is not being shaped solely by cyclical weakness and tighter monetary conditions. There remains one extraordinarily important countervailing force: the ongoing AI infrastructure boom. The scale of investment associated with artificial intelligence increasingly resembles a modern industrial boom rather than a conventional software cycle. Real US private investment in data centres has surged dramatically as hyperscalers race to build computational capacity, cloud infrastructure and AI training systems. Yet perhaps equally striking is the parallel surge in water supply construction spending. One of the great misconceptions surrounding AI is that it somehow belongs to a virtual economy detached from physical resource constraints. In reality, AI infrastructure is extraordinarily resource intensive, requiring vast quantities of electricity, cooling systems, water infrastructure and industrial-scale construction. Increasingly, the AI boom is colliding directly with broader questions surrounding energy systems, utility capacity and physical infrastructure constraints.

Chart 5: US Real Private Investment: Data Centers & Water Supply Construction

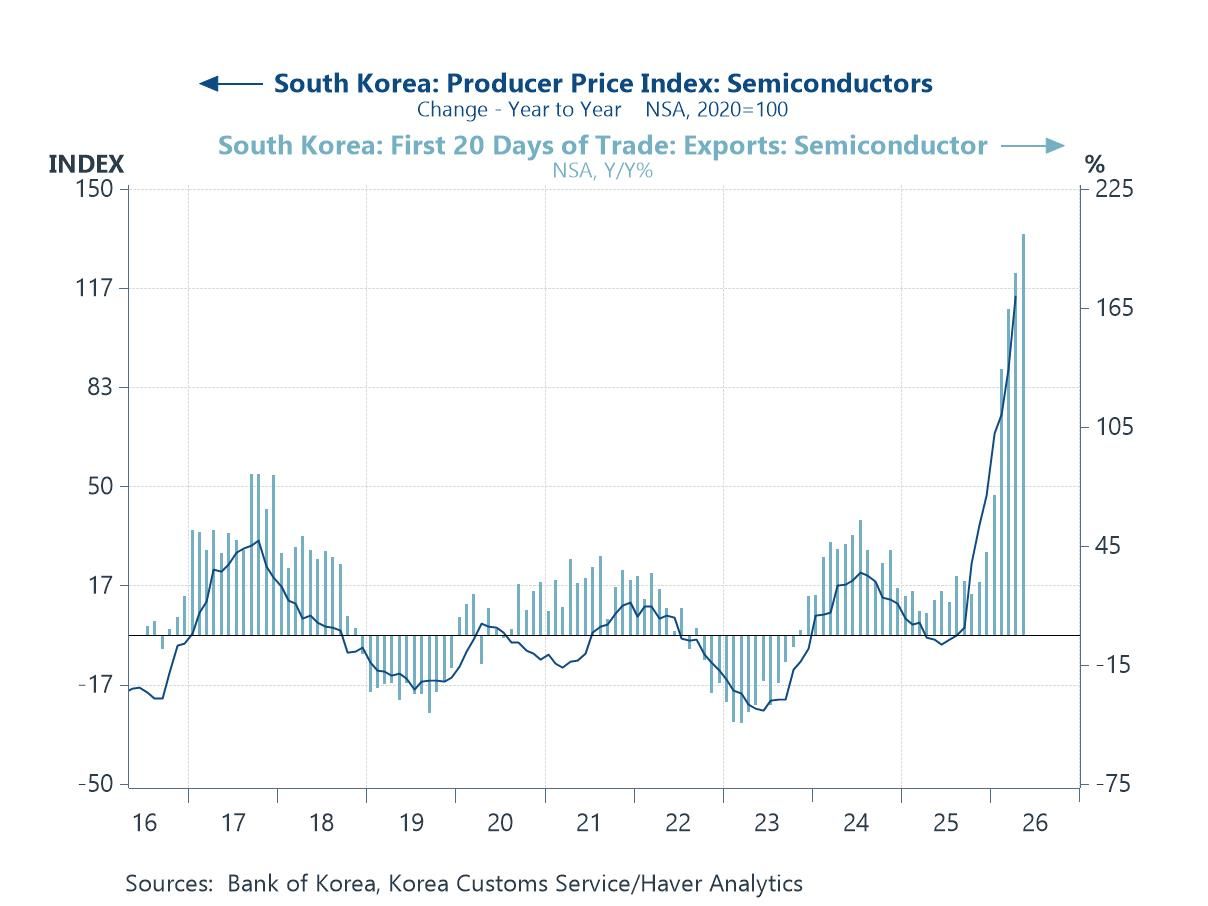

The AI cycle continues to drive global trade and investment Finally, the implications of this infrastructure boom are increasingly becoming visible globally through the semiconductor supply chain. South Korea’s semiconductor sector continues to provide one of the clearest real-time indicators of the scale and intensity of AI-related investment demand. Semiconductor export growth has accelerated sharply, while producer prices for semiconductors have also surged, reflecting exceptionally strong global demand for advanced chips, memory systems and computational infrastructure. In many respects, this remains the key counterweight supporting global equity markets and broader investor optimism despite ongoing geopolitical and inflation concerns. Even as parts of the global economy slow under the weight of higher energy prices, the AI-driven capex cycle continues to fuel trade, infrastructure spending and corporate earnings. Increasingly, markets appear willing to tolerate elevated bond yields, geopolitical tensions and energy volatility because investors remain convinced that AI-related productivity gains and infrastructure investment could ultimately transform the medium-term growth outlook. The result is a global economy increasingly caught between two competing forces: old-world supply-side inflation risks and one of the largest technology-driven investment booms in modern history.

Chart 6: South Korea Semiconductor Prices & Export Growth

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief